Events of Default in 2026: When Control Moves to the Lender

Defaults are rarely sudden. Pressure builds through missed payments, covenant stress, and refinancing pressure long before anything is formally declared. An event of default is not boilerplate. It is the point at which lender discretion turns into lender control. In 2026, tighter credit conditions and more active lender oversight make that shift more important to understand. The real issue is not the default itself, but the moment control transitions from the borrower to the lender.

What Are Events of Default? More Than Just a Breach

An event of default clause is a contractual trigger that gives the lender specific rights when borrower risk increases, but it does not trigger automatic enforcement. It is crucial to understand that these are not automatic enforcement mechanisms. It protects the lender’s position and creates a framework for intervention. In practice, it gives the lender options before the position deteriorates further.

That matters because default is rarely just about non-payment. It can arise from covenant breaches, cross-defaults, misrepresentation, or insolvency events. Once triggered, the borrower loses room to manoeuvre and the lender gains leverage over what happens next.

What Events Actually Trigger Default: Control in the Crosshairs

The drafting varies, but the main triggers are consistent. Each gives the lender a contractual basis to intervene. Each of these represents a critical point where the lender gains the right to intervene, effectively moving control away from the borrower.

Non-Payment: The Most Obvious Trigger

Non-payment is the obvious trigger. Missing interest, principal, or fees will usually become an event of default once any grace period expires. It is the clearest sign that the borrower is failing to meet core obligations.

Covenant Breach: The Early Warning System

Covenant breaches are often more important than non-payment because they give lenders an earlier trigger.

Financial covenants test the borrower’s numbers, including leverage, liquidity, and interest cover. A breach signals that financial performance is deteriorating before payments are missed.

Operational covenants test behaviour. These include reporting obligations, insurance requirements, restrictions on asset sales, and adherence to agreed business practices. A breach may not immediately affect cash flow, but it indicates that the borrower is moving outside the agreed framework.

In securities-based lending, a fall in collateral value can quickly trigger a loan-to-value breach, forcing the lender to reassess risk and tighten control.

A covenant breach does not necessarily lead to immediate enforcement. It tells the lender that risk is rising and that intervention may be required.

Cross-Default: The Domino Effect

A cross default clause means a default under one facility can trigger default under another. That matters because lenders are not underwriting a single payment in isolation. They are underwriting the borrower’s wider credit position. In practice, cross-default can turn one breach into a broader loss of control across the capital structure.

Insolvency: The Ultimate Control Shift

Insolvency events are the clearest formal shift in control. Administration, liquidation, or inability to pay debts typically gives the lender a direct route to enforcement and recovery.

Misrepresentation: Trust Undermined

A material misrepresentation can also trigger default. If key information was false or withheld, the lender can argue that the credit decision was made on a flawed basis.

Material Adverse Change (MAC): The Subjective Trigger

A material adverse change clause is more subjective. It gives the lender scope to act if the borrower’s business, financial condition, or prospects deteriorate materially. These clauses are heavily negotiated because they expand lender discretion, especially in volatile markets.

The Timing Problem: When Lenders Choose to Act

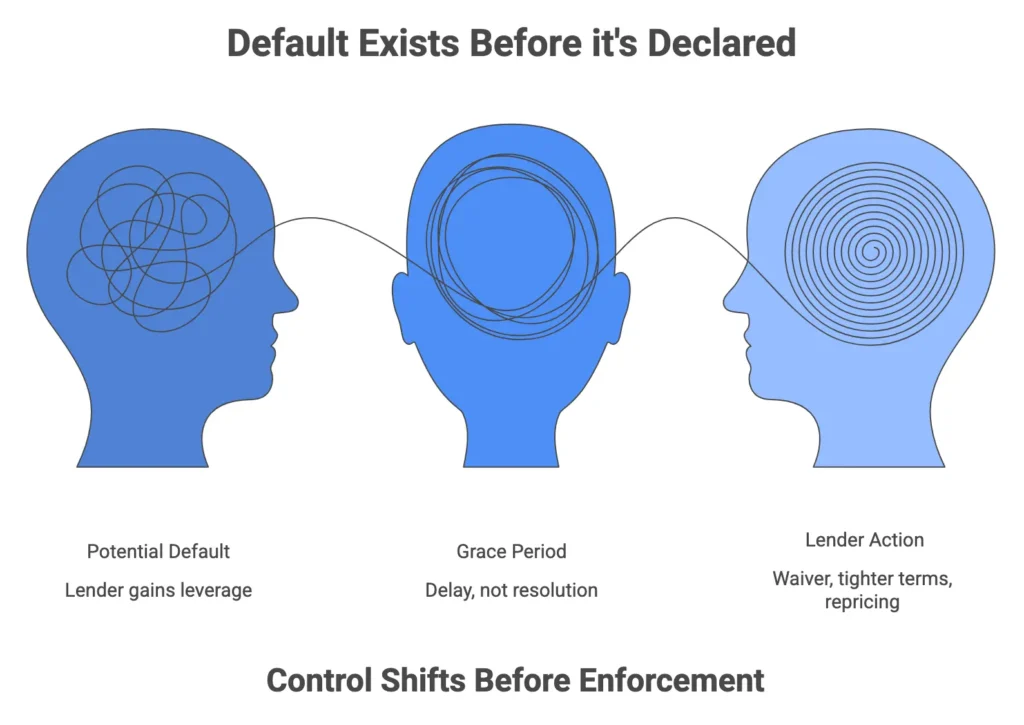

A default can exist before it is formally declared. That is where many borrowers get caught out.

Lenders rarely act on the first sign of a breach. They choose when to act, and the existence of a potential default becomes leverage.

Grace periods can create false comfort. They delay consequences, but they do not remove the underlying problem. The loan agreement determines how much flexibility the lender has and how much room the borrower has to respond. A lender may waive a breach in exchange for tighter reporting, additional security, or revised pricing. That is the point. Default does not always lead to immediate enforcement, but it almost always changes the bargaining position.

What Happens After Default: Real-World Behaviour

Once default occurs, the lender gains remedies, but their use is discretionary.

- Acceleration is optional. A lender can demand immediate repayment, but often prefers to preserve value first, especially where assets or cash flow remain viable.

- Waivers are strategic. They are rarely generous. They are negotiated, priced, and usually tied to tighter controls such as additional security, revised terms, or increased reporting.

- Restructuring often comes first. Amend-and-extend, revised covenants, staged deleveraging, or controlled asset sales can produce better outcomes than immediate enforcement.

The key point is simple. Enforcement may come later, but control shifts first.

Why Events of Default Matter More in 2026

Events of default matter more in 2026 because lender tolerance is lower and intervention happens earlier.

- Credit is tighter. Lenders are more risk-aware and less willing to overlook breaches.

- Oversight is more active. Performance is monitored closely, and issues are picked up faster.

- Documentation is more aggressive. More covenants and triggers give lenders earlier points of intervention.

- Waivers are less automatic. What was once overlooked is now used to renegotiate terms or tighten control.

For borrowers and intermediaries, this changes the dynamic. Defaults are more likely to become negotiation triggers rather than being quietly waived.

What to Consider / Key Takeaways

For borrowers and intermediaries, events of default need to be assessed strategically, not just legally.

- Defaults are negotiation tools. They often create leverage before they lead to enforcement.

- Structure matters as much as drafting. The outcome depends on the facility, the collateral, and the lender’s objectives, not just the clause itself.

- Early-stage breaches matter. A minor covenant issue can become a bigger problem if it is ignored.

- Cross-default can widen the problem quickly. One breach in one facility can trigger pressure elsewhere.

- Trigger points should be understood before signing. Borrowers need clarity on what can trip default and what rights that gives the lender.

Conclusion

Events of default are not technicalities. They determine who controls the outcome.

In 2026, understanding how these triggers are used is essential for managing credit risk properly.

The issue is not simply whether default exists. It is what rights it activates, and who controls the next move.

Discreet Discussion on Credit Structure

If you are reviewing existing financing or structuring new credit exposure, understanding how control shifts under different scenarios is critical.

If that is relevant, you can discuss your situation hereFor a more structured breakdown of how these strategies are applied in practice, see the Borrowers Trust& Due Diligence Playbook