Covenant Breach in 2026: What Happens When Terms Are Broken

In the intricate world of high finance, a covenant breach is not an isolated incident. It is, more often, the culmination of underlying pressures, be it tightening liquidity, impending refinancing challenges, or the relentless squeeze of earnings compression. For high-level decision-makers, investors, and HNWI’s, the critical error is treating the breach as a legal technicality instead of a negotiation event. In the dynamic credit markets of 2026, lenders are not passive observers; they leverage a covenant breach to reprice risk, assert greater control, and fundamentally reshape the terms of engagement. The real challenge is managing the immediate aftermath, where control shifts quickly if handled poorly.

What is a Covenant Breach (In Credit Terms)?

At its core, a covenant breach signifies a borrower’s failure to adhere to specific financial or operational stipulations outlined in a loan agreement. These stipulations, or financial covenants, typically include metrics such as leverage ratios, interest cover ratios, and liquidity thresholds. The moment a breach occurs, lender discretion takes over and the negotiation begins

What Happens Immediately After a Breach

The period immediately after a breach matters more than the breach itself. It is a time of heightened scrutiny and rapid internal assessment by lenders.

Firstly, expect an immediate and significant increase in information requests. Lenders will seek granular detail on your financial position, operational performance, and any mitigating actions. This is not about the numbers, it is about whether the issue is temporary or structural. Is this a temporary blip, or a symptom of deeper, systemic issues?

Internal credit discussions start before any engagement with the borrower. Risk committees will convene, scenarios will be modelled, and potential strategies will be formulated. This internal alignment means that by the time lenders approach the borrower, they already have a position.

Time becomes the key negotiating variable. The first 72 hours post-breach can dictate the trajectory of the entire resolution process. Delays in providing requested information, or a perceived lack of transparency, will invariably weaken the borrower’s position, ceding control to the creditor.

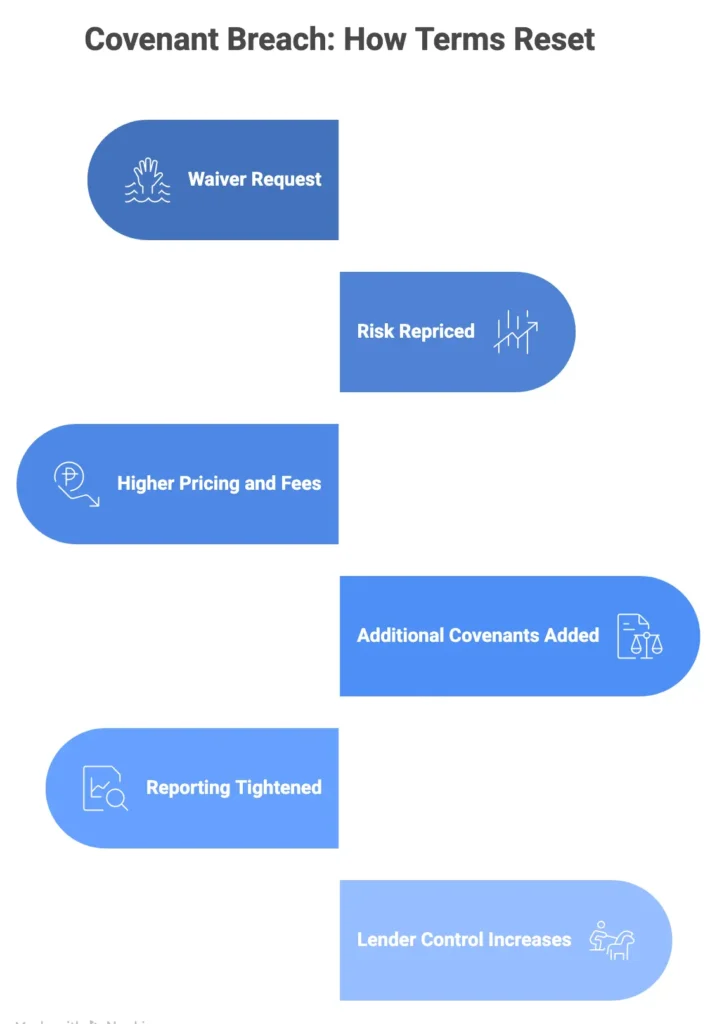

Waivers, Amendments, and Repricing Risk

When a covenant breach occurs, a covenant breach waiver is often the immediate objective for a borrower. However, a waiver is not forgiveness, it is a reset of terms. Lenders will almost certainly use this opportunity to reprice the risk associated with the loan. This shows up in:

- Increased Pricing: Higher interest rates, facility fees, or commitment fees are common covenant breach consequences.

- New Fees: Introduction of waiver fees, amendment fees, or restructuring fees.

- Additional Covenants: Lenders may layer in more stringent financial covenants or operational undertakings to enhance their control and monitoring capabilities.

- Tightened Reporting: More frequent and detailed financial reporting requirements will be imposed, providing lenders with a clearer, real-time view of the borrower’s performance.

This repricing reflects higher risk and gives lenders tighter control.

Cure Rights and Timing Pressure

Many loan agreements include provisions for covenant breach cure periods. These periods allow a borrower a limited timeframe to rectify the breach. Cure rights are conditional and limited.

Common cure mechanisms include:

- Equity Cures: The injection of new equity into the business to improve financial ratios, such as reducing leverage or boosting liquidity. This is often a preferred option for lenders as it strengthens the capital base.

- Operational Fixes: Implementing operational changes to improve profitability (e.g., cost-cutting, revenue enhancement) or asset sales to reduce debt.

Timing pressure is severe. Delays in executing a credible cure plan significantly weaken the borrower’s negotiating position. A delayed or failed cure pushes the situation toward default.

When a Breach Becomes an Event of Default

A covenant breach is not the same as an event of default. Not all breaches automatically trigger an immediate event of default. Often, the loan agreement will specify a grace period or a cure period before a breach formally becomes an event of default. Lenders control when escalation happens.

Once a covenant breach event of default is declared, the implications are immediate:

- Cross-Default Risk: Many loan agreements contain cross-default clauses, meaning a default under one facility can trigger defaults across other debt instruments, creating a domino effect.

- Acceleration Rights: Lenders gain the right to accelerate the repayment of the entire outstanding debt, demanding immediate settlement.

- Enforcement Rights: The creditor can exercise their security rights, potentially seizing assets or appointing receivers to recover their funds.

Understanding the nuances of when a covenant breach transitions into an event of default is paramount for any borrower or investor.

Control Shift: Where Borrowers Lose Leverage

This is where control is lost. A covenant breach fundamentally shifts control from the borrower to the lender. Lenders move from passive capital to active control.

- Tightened Consent Rights: Strategic decisions that previously required minimal lender input, such as significant capital expenditures, acquisitions, or divestitures, will now likely require explicit lender approval.

- Reduced Optionality: The borrower’s flexibility to pursue new opportunities, raise additional debt, or even manage their cash flow freely diminishes rapidly.

- Strategic Decisions Under Scrutiny: Lenders will scrutinise every major business decision, ensuring it aligns with their objective of debt recovery and risk mitigation.

This removes the borrower’s ability to operate independently, often leading to outcomes that may not align with their long-term strategic vision.

Key Takeaways – Managing a Breach Properly

Navigating a covenant breach requires a proactive and strategic approach.

- Early Engagement vs. Delayed Reaction: Delaying engagement is a common and costly mistake. Early, transparent communication, coupled with a credible plan, can significantly improve outcomes.

- Understand Lender Incentives: Do not just focus on the legal position. Understand what motivates your lender, their internal risk appetite, regulatory pressures, and their desire to protect their capital. This drives negotiation outcomes.

- Prepare for Repricing: Assume that a repricing of the loan is inevitable. Model the impact of higher pricing before negotiations start.

- Control the Narrative: Present a clear, concise, and compelling narrative about the cause of the breach, the steps being taken to rectify it, and the long-term viability of the business. Present a clear forward plan, not just numbers.

Conclusion – Breach as a Strategic Inflection Point

In the sophisticated credit landscape of 2026, a covenant breach is not merely a failure; it is a strategic inflection point. The outcome depends on speed and preparation. Lenders today act faster and with less flexibility, making proactive management essential. Mishandling a breach can lead to a significant loss of control and value, whereas a well-managed response can reset terms and even strengthen the long-term relationship with your creditor.

Discreet Discussion on Credit Pressure and Covenant Risk

If a covenant breach is becoming a possibility, or existing financial covenants are already under pressure, the situation can still be managed, but timing and positioning matter. Understanding how lenders assess risk and respond internally often determines whether terms are reset or control is lost. If relevant, you can discuss your situation here

For a more structured breakdown of how these strategies are applied in practice, see the Borrower Trust & Due Diligence Playbooks section.