Liability Management Exercises 2026: Control, Restructuring and Creditor Dynamics

Liability management exercises (LMEs) have moved from niche restructuring tools to a central feature of debt strategy in 2026. The financial landscape is materially different from the preceding decade, with cheap, readily available capital replaced by tighter liquidity and higher interest rates. For decision-makers, investors, and HNWIs, this shift fundamentally alters the calculus of debt management. Refinancing, once assumed, is now uncertain, pushing borrowers and sponsors towards more complex and proactive solutions to maintain control over capital structures.

The Shift from Refinancing to Restructuring

For years, approaching debt maturities was straightforward: refinance. Liquidity was abundant, lenders were active, and extending terms or raising new debt was relatively frictionless. In 2026, that dynamic has changed. Higher rates, persistent inflation, and tighter lending conditions have materially reduced refinancing options, leaving many leveraged and distressed borrowers facing punitive terms or limited access to capital.

This shift forces a re-evaluation of strategy. Rather than relying on refinancing alone, borrowers are increasingly required to restructure existing obligations. Liability management exercises (LMEs) provide a mechanism to do this out of court, using flexibility within credit documentation to reshape maturities, priority, and capital structure without entering formal insolvency. For C-suite executives and investors, understanding these tools is now critical to preserving value and maintaining control.

What Are Liability Management Exercises?

Liability management exercises (LMEs) are out-of-court transactions used by borrowers and sponsors to restructure existing debt. Rather than relying on formal insolvency processes, LMEs utilise flexibility within credit agreement documentation to alter terms, priority, or structure. The objective is to address maturity pressure, manage liquidity constraints, and reposition the capital structure in a controlled way.

These transactions do not eliminate obligations; they reshape them to remain sustainable for the borrower while securing support from a sufficient group of creditors. Their effectiveness depends on documentation, particularly covenants and amendment thresholds, which determine what can be changed and by whom. For lenders, the outcome of an LME can materially affect recovery and seniority.

Core LME Structures

Liability management exercises typically fall into a small number of core structures, each designed to adjust priority, extend maturities, or introduce new capital within the existing documentation framework.

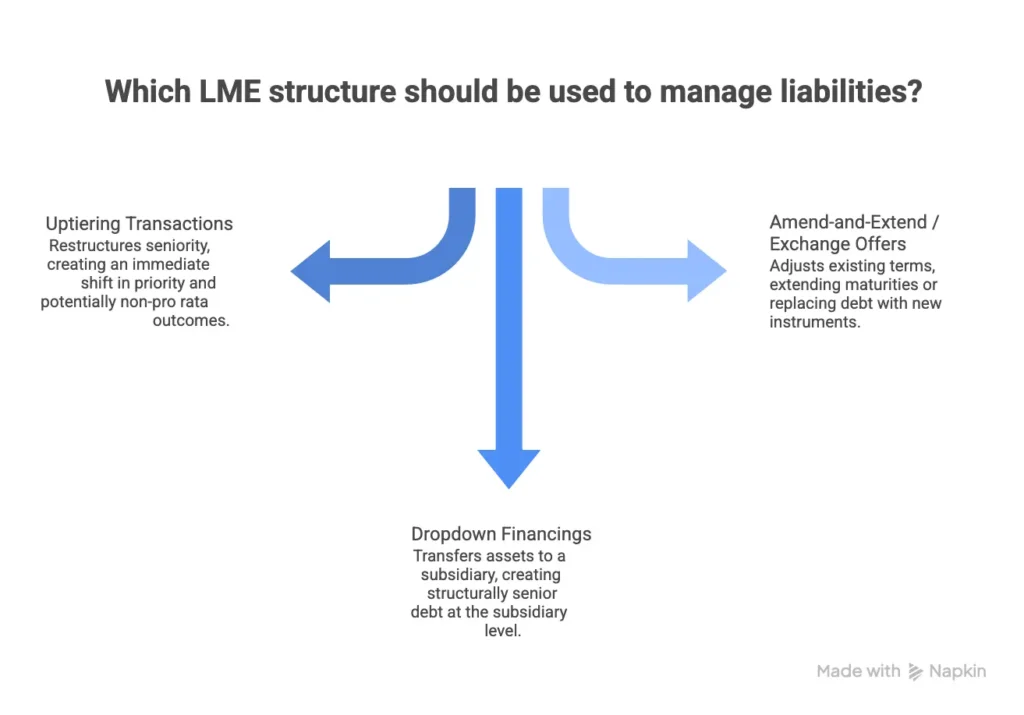

Uptiering Transactions

Uptiering transactions restructure seniority. A subset of lenders exchanges into, or provides, new debt that ranks ahead of existing non-participating creditors.

This creates an immediate shift in priority and often results in non-pro rata outcomes, leaving excluded lenders subordinated and increasing the risk of dispute.

Dropdown Financings

Dropdown financings transfer assets to an unrestricted subsidiary, which then raises new secured debt against those assets.

This effectively removes collateral from the original creditor group and creates structurally senior debt at the subsidiary level.

Amend-and-Extend / Exchange Offers

Amend-and-extend transactions adjust existing terms, typically extending maturities in exchange for improved economics for participating lenders.

Exchange offers replace existing debt with new instruments, often combined with consent provisions that weaken the position of non-participating creditors.

These structures are less aggressive but still shift outcomes through documentation rather than formal restructuring.

Control, Incentives and Creditor Dynamics

Liability management exercises are ultimately about control. They are not just restructurings, but strategic actions that shift power within a capital structure through incentives and selective participation.

Creditor-on-Creditor Conflict

LMEs create a divide between participating and non-participating lenders. Borrowers secure support by offering improved terms to a subset of creditors, such as enhanced priority or access to new money.

This leads to non-pro rata outcomes, where excluded lenders are diluted or subordinated. In private credit markets, where documentation and alignment vary, this often results in disputes and increased litigation risk.

How Control Shifts Within the Capital Structure

LMEs reallocate control rather than eliminate debt. In practice, they allow borrowers and sponsors to:

- Extend maturities and delay refinancing pressure

- Introduce new capital on a senior basis

- Weaken the position of non-participating creditors

Each of these shifts reduces the leverage of holdout lenders and strengthens participating creditors. Control is not static; it is defined by documentation and execution.

Why LMEs Are Increasing in 2026

Several factors are driving the increased use of liability management exercises in 2026:

- Refinancing Pressure: Traditional refinancing is less available, particularly for leveraged borrowers facing near-term maturities.

- Higher Rates / Tighter Liquidity: Rising funding costs and reduced liquidity limit access to new capital.

- Private Credit Growth: More flexible but often more aggressive structures are increasing the use of out-of-court solutions.

- Documentation Flexibility: Credit agreements now commonly include provisions that allow restructuring actions without unanimous consent.

Real-World Positioning (Use Cases)

LMEs are applied in practice across a range of scenarios:

- Sponsor-Led Restructuring Ahead of Maturity: A sponsor facing a maturity wall may use an uptiering transaction to extend maturities, inject new capital, and improve positioning for participating lenders, while subordinating holdouts.

- Borrower Avoiding Default Through Liability Reshaping: A company under short-term liquidity pressure may launch an exchange offer, extending maturities and adjusting terms to stabilise cash flow and avoid default.

- Lenders Protecting or Improving Position: A creditor group may support a dropdown financing, providing new money in exchange for structurally senior exposure to key assets.

What to Watch

For those exposed to leveraged capital structures, the key risks are structural:

- Documentation Loopholes: Credit agreements often contain provisions that allow asset transfers or new debt without unanimous consent.

- Consent Thresholds: Many amendments require only a majority, leaving minority creditors exposed.

- Risk of Exclusion: Not all lenders are invited to participate, increasing the risk of subordination.

- Litigation Exposure: Aggressive structures frequently lead to disputes from non-participating creditors.

Conclusion – Control is Structured, Not Assumed

In 2026, control is not assumed by hierarchy; it is defined by documentation. Outcomes are increasingly determined by credit agreements, sponsor strategy, and creditor alignment, not simply by seniority.

For market participants, understanding how liability management exercises shift priority and influence outcomes is essential. Those who act early, by assessing documentation, positioning within the capital structure, and exposure to non-pro rata outcomes, are better placed to preserve value. Those who react late risk dilution.

If you are reviewing refinancing options or assessing your position within a capital structure exposed to liability management exercises, a discreet discussion may help clarify available strategies and risks. You can discuss your situation here.

For a more structured breakdown of how these strategies are applied in practice, see our Borrower Trust & Due Diligence Playbook