Intercreditor Agreement 2026: Control, Priority and Lender Priority

In the intricate world of modern finance, where capital structures are increasingly layered and sophisticated, the true locus of control often lies not just in the amount of capital provided, but in the precise wording of a seemingly technical document: the intercreditor agreement.

For high-level decision-makers, investors, and HNWIs navigating multi-lender financing, understanding this agreement is paramount. It’s the blueprint that dictates who holds the reins when challenges arise, determining priority of payment, enforcement rights, and ultimately, the real power dynamics within a financing transaction.

Many modern financing transactions now involve multiple lenders with different priorities, ranging from senior secured banks to mezzanine funds and private credit providers. In these situations, the intercreditor agreement determines repayment priority, enforcement rights and control during financial distress.

What Is an Intercreditor Agreement?

At its core, an intercreditor agreement is a contractual arrangement between two or more lenders to the same borrower that meticulously defines the rights, obligations, and priority of claims among those creditors. Think of it as a pre-nuptial agreement for lenders, meticulously outlining how they will interact, particularly when the borrower faces financial stress or an event of default.

The purpose of an intercreditor agreement is multifaceted. It establishes a clear framework governing the relationship between different creditors, ensuring that their respective rights and priorities are understood and agreed upon upfront. This proactive approach helps to avoid costly and protracted disputes during challenging times.Key elements typically addressed within an intercreditor agreement include:

- Priority of Payment – the order in which creditors are repaid if the borrower defaults or enters insolvency.

- Security Interests and Lien Ranking – which lender holds the first claim over collateral and which claims are subordinate.

- Rights of Senior and Junior Lenders – defining what actions each creditor can take during default or restructuring.

- Procedures During Default or Insolvency – agreed protocols governing enforcement, asset sales and negotiations.

In essence, an intercreditor agreement protects lender interests while ensuring that potential disputes are managed through pre-agreed contractual arrangements rather than through contentious and unpredictable litigation. It is a vital component of any sophisticated financing transaction involving multiple creditors, providing clarity and certainty to all parties involved.

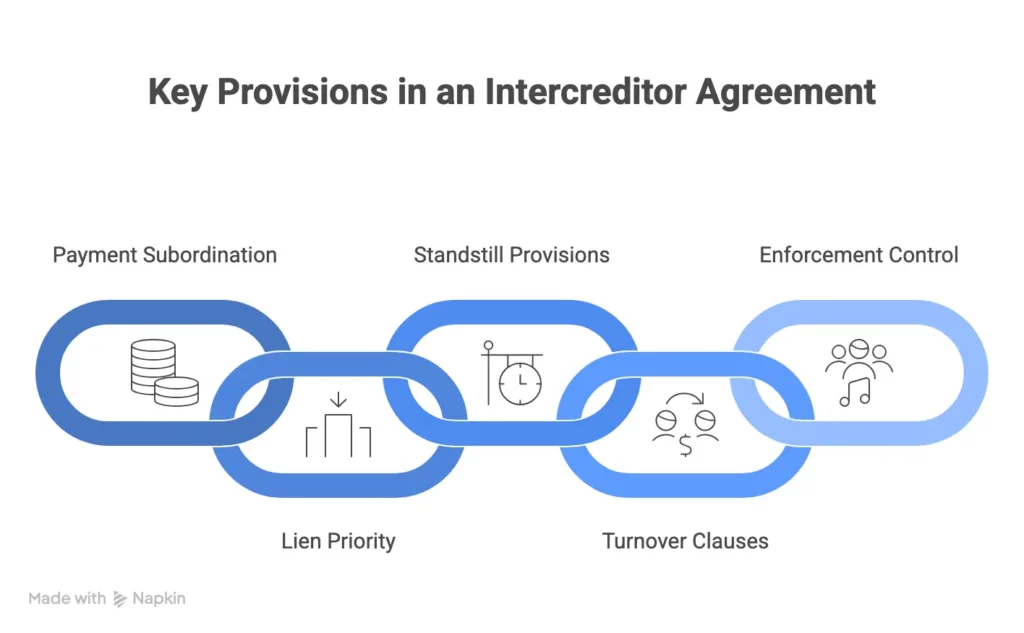

Key Provisions in an Intercreditor Agreement

Understanding the specific contractual provisions within an intercreditor agreement is crucial for both borrowers and lenders. These clauses dictate the practical implications of the agreement, particularly during periods of financial stress.

Payment Subordination

One of the most fundamental provisions is payment subordination. This clause dictates that junior debt repayment will only occur after the senior debt is fully satisfied. Payments to the junior creditor may be severely restricted or even entirely prohibited during an event of default or if the senior lenders have not been fully discharged. This ensures that senior creditors receive their due before any junior debt holders.

Lien Priority and Security Interests

The intercreditor agreement meticulously defines lien priority and security interests. It specifies which lender holds the first claim over the borrower’s assets (first lien) and which claims are subordinate (second lien). This ranking is paramount, as it often determines the order in which creditors can enforce security and recover their investments during insolvency or bankruptcy court proceedings. For instance, a senior secured lender with a first lien will have priority over a junior creditor with a second lien on the same collateral.

Standstill Provisions

Standstill provisions are designed to give senior lenders control over the enforcement process. These clauses typically prevent junior lenders from commencing enforcement proceedings against the borrower for a defined standstill period after an event of default. This allows senior lenders to control restructuring negotiations, asset sales, or other enforcement actions without interference from junior creditors, who might otherwise trigger a premature or uncoordinated liquidation.

Turnover Clauses

Turnover clauses are a critical protective measure for senior lenders. If a junior lender inadvertently or improperly receives a payment from the borrower that is contrary to the agreed-upon payment priority in the intercreditor agreement, the turnover clause mandates that the junior lender must immediately transfer those funds to the senior lender. This reinforces the agreed-upon order of priority and prevents circumvention.

Enforcement Control

Typically, senior secured lenders are granted significant enforcement control within an intercreditor agreement. This means they usually have the primary right to initiate and direct enforcement actions, such as asset sales, restructuring negotiations, or legal proceedings against the borrower.

This centralisation of control aims to ensure a coordinated and efficient recovery process, preventing multiple creditors from pursuing disparate and potentially conflicting enforcement strategies. Many intercreditor agreements also define voting rights and amendment thresholds, determining which creditors must approve restructurings, waivers or changes to the capital structure.

Intercreditor Agreement vs. Subordination Agreement

While both an intercreditor agreement and a subordination agreement deal with the ranking of debt, their scope and complexity differ significantly.

A subordination agreement is generally a more focused document. It primarily involves a junior creditor agreeing to subordinate its right to repayment to a senior creditor. Its main function is to establish a clear hierarchy for payment, ensuring that the senior lender is paid first.

An intercreditor agreement, by contrast, is far broader and more comprehensive. It governs the full relationship between different creditors, extending beyond mere payment priority to include:

- Enforcement Rights: Who can take action against the borrower and when.

- Collateral Sharing: How shared collateral is managed and realised.

- Voting and Restructuring Decisions: How lenders will vote on critical matters affecting the borrower’s capital structure and during insolvency.

Essentially, while a subordination agreement is a component of establishing a senior and junior capital structure, an intercreditor agreement provides the overarching framework for how all these different creditors will interact, particularly when the borrower is in distress. It’s the difference between a single rule and an entire rulebook.

Intercreditor Agreement vs. Agreement Among Lenders

Another important distinction exists between an intercreditor agreement and an Agreement Among Lenders (AAL). While both involve multiple lenders, they typically apply to different financing structures.

An Agreement Among Lenders (AAL) is often used in unitranche facilities. In a unitranche structure, lenders provide a single loan facility to the borrower, but internally, they allocate senior and junior risk among themselves. The AAL then governs this internal allocation, defining how the single loan is shared and how different tranches within that loan are treated.

An intercreditor agreement, conversely, typically governs separate lending facilities with distinct security positions. For example, it would be used between a first-lien lender providing senior secured debt and a second-lien lender or a mezzanine debt provider. Here, the lenders have separate debt and security documents, and the intercreditor agreement bridges these distinct contractual arrangements, establishing the order of priority and respective rights.

This distinction is crucial when considering structures involving pari passu arrangements (where creditors have equal standing), first and second lien lenders, or complex mezzanine debt financing. Each structure necessitates a specific type of agreement to manage creditor rights and priorities effectively.

Real-World Scenarios Where Intercreditor Agreements Matter

The theoretical aspects of an intercreditor agreement gain significant clarity when viewed through practical, real-world scenarios. These examples demonstrate why these agreements are central to managing creditor rights and ensuring capital structure stability.

Example 1: Leveraged Acquisition Financing

Consider a private equity firm undertaking a leveraged acquisition. The borrower group raises senior secured debt from a syndicate of banks and simultaneously secures mezzanine debt from a private credit fund.

The intercreditor agreement in place between the senior secured lenders and the mezzanine provider will meticulously define the order of priority for repayment, the allocation of security interests, and crucial standstill rights if an event of default occurs. This agreement dictates, for instance, that the mezzanine fund cannot commence enforcement proceedings until the senior debt is fully discharged or a specified standstill period has elapsed, giving the senior lenders control over the initial response to distress.

Example 2: First Lien / Second Lien Structures

In many financing transactions, particularly in leveraged finance, a borrower might have two secured lenders sharing the same collateral but holding different priority rights. A first-lien lender will have the primary claim, while a second-lien lender will have a subordinate claim.

The intercreditor agreement in this scenario is vital. It will detail how the shared collateral is managed, who controls the sale or liquidation of assets, and the payment priority from the proceeds. Often, enforcement decisions may be exclusively controlled by the first-lien lender, even if the second-lien lender is also secured.

Example 3: Restructuring or Insolvency

Perhaps the most critical juncture where an intercreditor agreement comes into play is during bankruptcy proceedings or a broader restructuring. When a debtor faces insolvency, the agreement determines which creditors can enforce security, negotiate restructuring terms, or receive repayment first from the limited assets available.

The subordination provisions, standstill provisions, and enforcement control clauses become legally binding directives for the bankruptcy court, guiding the distribution of assets and the resolution of creditor claims. Without a robust intercreditor agreement, such situations can quickly devolve into costly and protracted legal battles among different creditors. These examples underscore why intercreditor agreements are not merely legal boilerplate but fundamental instruments for managing risk, allocating control, and preserving the integrity of complex capital structures.

Why Intercreditor Agreements Are More Important in 2026

The financial landscape of 2026 is characterised by an increasing reliance on sophisticated, layered capital structures. This trend has significantly elevated the importance of intercreditor agreements as the essential contractual framework governing multiple creditors.

Several key drivers contribute to this heightened significance:

- Expansion of Private Credit Funds: The rapid growth of private credit funds has introduced a wider range of non-bank lenders into the market, often providing junior debt, unitranche facilities or bespoke financing solutions alongside traditional bank lenders.

- Complex Leveraged Finance Structures: Leveraged buyouts and acquisition financings frequently involve multiple tranches of debt, including senior secured, second-lien and mezzanine debt, with junior lenders contractually subordinated to senior creditors through the intercreditor agreement.

- Growth in First-Lien / Second-Lien Lending: The increasing use of first and second lien structures has made intercreditor agreements essential for defining lien priority, enforcement rights and repayment hierarchy.

- Mezzanine Debt Financing: Mezzanine debt sits between senior debt and equity in the capital structure, requiring carefully structured intercreditor provisions to prevent conflicts with senior secured lenders.

As more financing transactions involve different creditors with varying risk appetites and repayment expectations, intercreditor agreements provide the crucial legal framework that protects creditors’ interests, preserves the agreed-upon repayment order, and ensures an orderly process during financial distress. They are the bedrock upon which the stability of these complex capital structures rests.

What Borrowers Should Understand Before Signing

While intercreditor agreements are primarily designed to protect the interests of lenders, borrowers must possess a thorough understanding of their provisions before signing. These agreements can significantly influence a borrower’s operational flexibility, strategic options, and ability to navigate financial stress or restructuring scenarios.

Borrowers, particularly high-level decision-makers and corporate treasurers, should carefully review and seek expert advice on:

- Priority of Payment Provisions: Understand when and how different classes of creditors are repaid, as this directly affects cash flow management during financial stress.

- Standstill Periods Affecting Junior Lenders: Be aware of clauses preventing junior creditors from enforcing security for a defined period, leaving senior lenders in control of enforcement decisions.

- Enforcement Rights of Senior Secured Lenders: Senior lenders often control enforcement actions, asset sales and restructuring negotiations, which can limit the borrower’s strategic options.

- Restrictions on Refinancing or Restructuring: Some agreements restrict refinancing or restructuring without lender consent, potentially limiting future flexibility.

Understanding these provisions early in the financing transaction helps borrowers structure capital more effectively, negotiate more intelligently, and avoid unintended constraints down the line. It’s about proactively managing potential risks and ensuring that the financing aligns with the borrower’s long-term strategic objectives.

Conclusion: Control Often Lies in the Documentation

In the increasingly complex world of multi-lender financing, the intercreditor agreement stands as a pivotal document. While often perceived as a technical legal instrument, it is, in reality, one of the most influential agreements within a layered capital structure. It meticulously determines who controls enforcement actions, establishes the critical priority of payment, and defines the precise scope of creditor rights when a borrower faces financial distress.

For high-level decision-makers, investors, and HNWIs navigating sophisticated financing structures in 2026, understanding how these agreements allocate power is not merely a legal nicety; it is essential to managing risk, preserving strategic flexibility, and ultimately, safeguarding investments. The true measure of control and real power in these arrangements often lies not just in the capital provided, but in the detailed, often overlooked, clauses of the intercreditor agreement.

Discreet Enquiries

If you are evaluating a multi-lender financing structure or reviewing intercreditor arrangements within an existing capital stack, a discreet discussion may provide useful clarity.

Discuss your options here.