Securities Based Lending 2026: A Lender’s Guide to Structure and Risk

In 2026, securities-based lending is no longer a convenience product. It is a capital structuring tool used when liquidity, timing, and control matter more than cost alone.

Higher rates, tighter bank balance sheets, and increased disclosure sensitivity have shifted demand toward private, asset-backed solutions. Borrowers are no longer asking if they can raise liquidity against portfolios. They are asking how to do it without triggering risk, signalling, or forced decisions. The difference now is not access. It is structure. Loan-to-value discipline, lender recourse, and margin mechanics determine whether a facility provides flexibility or creates pressure at the wrong time.

What Is Securities Based Lending?

Securities based lending allows investors, corporations, and high-net-worth individuals to raise liquidity against an investment portfolio without selling underlying assets.

Collateral typically consists of marketable securities such as listed equities, bonds, or funds. Advance rates are determined by liquidity, concentration, and volatility, not just headline value.

Proceeds are flexible in use. Common applications include real estate acquisition, business investment, debt refinancing, and funding of illiquid or non-bankable assets.

The trade-off is structural. Exposure to market movement introduces margin sensitivity. As collateral values decline, borrowers may be required to provide additional assets or reduce the facility. Understanding this dynamic is central to using securities based lending effectively.

How Securities Based Lending Works

Securities based lending allows borrowers to raise liquidity against marketable securities, with facility size determined by collateral quality and structure rather than headline portfolio value.

The key variables are loan-to-value, asset liquidity, concentration, and lender risk tolerance.

Loan-to-Value Ratio

The amount that can be borrowed is defined by the loan-to-value ratio applied to eligible securities.

Collateral typically includes listed equities, bonds, or funds. Advance rates are not fixed. They vary based on liquidity, volatility, and concentration risk.

For example, a $10 million portfolio at 70% LTV supports a $7 million facility. In practice, concentrated or less liquid positions are discounted more heavily, reducing effective borrowing capacity.

LTV is not a borrower benefit. It is the primary control mechanism used by lenders to manage downside exposure.

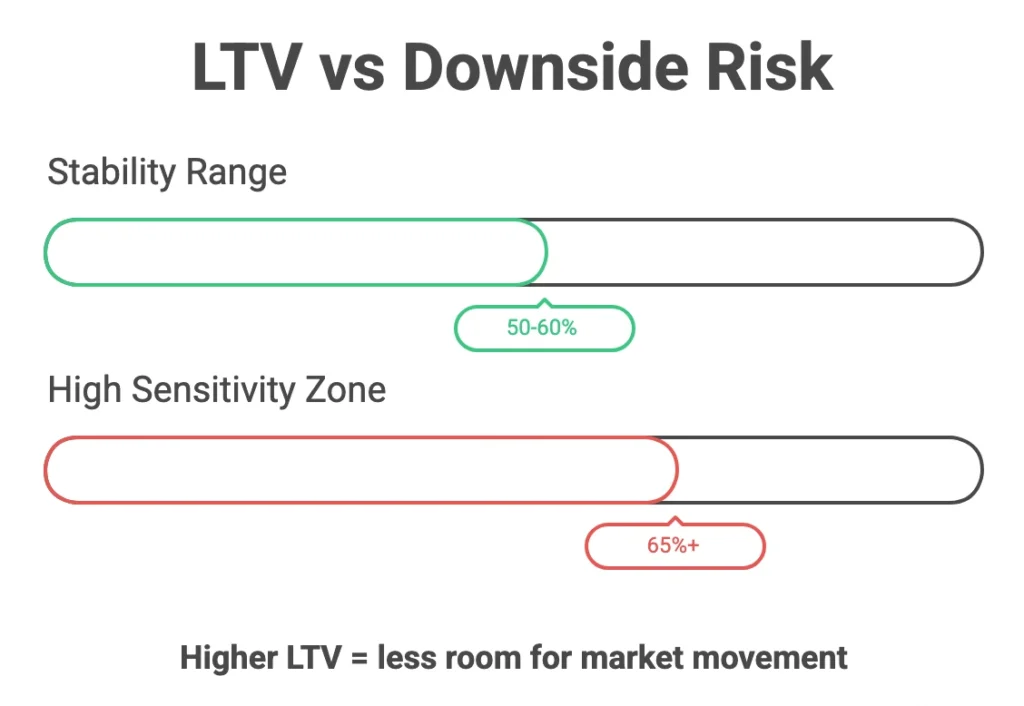

Low LTV vs. High LTV: Balancing Liquidity and Risk

Higher LTV increases available liquidity but reduces tolerance to market movement.

As LTV rises, the distance between current valuation and margin call thresholds compresses. This increases the probability of intervention if prices decline.

Lower LTV reduces initial proceeds but provides greater stability. It allows the facility to absorb normal market volatility without triggering collateral calls or forced repayment.

The decision is not how much can be borrowed. It is how much movement the structure can withstand without requiring action.

Interest Rate Structure

Pricing reflects both market benchmarks and structural risk.

Private lenders typically offer fixed rates, providing cost certainty over the term. Banks and larger institutions tend to use floating rates linked to benchmarks such as SOFR, EURIBOR, or BBSW, with an added margin.

Floating rates introduce variability in cost. Fixed rates shift that risk into pricing but remove exposure to rate increases.

Rate selection is secondary to structure. Stability of the facility under stress is the primary consideration.

Recourse vs. Non-Recourse Lending

The distinction between recourse and non-recourse is fundamental.

Banks generally operate on a recourse basis. If collateral value declines, they can liquidate securities and pursue the borrower’s broader balance sheet.

Private lenders often structure facilities on a non-recourse basis. Enforcement is limited to the pledged assets. If thresholds are breached and not cured, the lender can liquidate the position but has no claim beyond the collateral.

This directly affects risk containment. Non-recourse limits exposure to the asset. Recourse extends it to the borrower.

Repayment Terms

Repayment structures are typically flexible and aligned to liquidity objectives.

Common formats include interest-only periods with a bullet repayment at maturity. This allows borrowers to retain ownership of the underlying portfolio while accessing capital.

Flexibility does not remove obligation. Terms, triggers, and repayment mechanics must be understood in full, particularly under stressed scenarios.

Lender Insight: LTV is a Control Tool, Not a Borrower Benefit

Lenders do not set LTV to maximise borrower proceeds. They set it to control downside.

In practice, LTV determines three things:

- how quickly risk escalates if markets move

- when the lender can intervene

- how much optionality exists in a stressed scenario

Higher LTV increases utilisation but reduces tolerance. Lower LTV reduces deployment but increases stability.

From a structuring perspective:

- concentrated positions are sized for exit risk, not mark-to-market

- volatile names are haircut beyond standard models

- liquidity matters more than headline valuation

Private lenders price this explicitly. Banks manage it through margin systems and recourse.

The borrower decision is not how much can be borrowed. It is how much volatility the structure can absorb without forcing action.

Pros of Securities Based Lending

No Forced Liquidation

Liquidity is raised without selling core positions, avoiding market signalling and potential tax realisation

Flexible Use of Proceeds

Capital can be deployed across investments, to increase a concentrated position, real estate, or refinancing without structural restrictions.

Competitive Cost of Capital

Pricing is driven by liquid collateral. Facilities are structured in the low single digits.

Fixed Term Structure

Facilities are fixed term with fixed pricing. Return is driven by holding the position to maturity.

Cons of Securities Based Lending

Exposure to Market Movement

Collateral is marked to market. Price declines reduce coverage and bring the facility closer to trigger levels.

Margin Call Risk

If thresholds are breached, borrowers must provide additional collateral or reduce the loan, often within tight timeframes.

Asset Eligibility Constraints

Structure is driven by exitability. Liquidity and position size determine how the collateral is sized and managed.

Structural Constraints

Pledged securities are controlled by the lender. They cannot be sold or reduced during the term. Additional collateral can be added.

Borrowing vs Liquidating Holdings

The decision is not theoretical. It is driven by timing, control, and constraints.

Impact on Position

Selling reduces exposure and may move the market, particularly in concentrated or less liquid names. Borrowing preserves the position and avoids signalling.

Liquidity Timing

Borrowing provides immediate liquidity without execution risk. Selling depends on market conditions and may require staged exits.

Tax Considerations

Selling may trigger capital gains. Borrowing avoids realisation, preserving the existing position.

Using Securities Based Lending for Portfolio Rebalancing

Rebalancing often requires liquidity without disrupting core positions. Selling can create market impact, execution risk, and tax realisation.

Securities based lending allows capital to be raised against existing holdings, enabling reallocation without reducing exposure.

This is typically used where:

- positions are concentrated

- liquidity is limited

- timing matters

For example, a borrower can raise capital against listed equities and deploy it into alternative assets or new opportunities, while maintaining the original position.

The benefit is continuity. Exposure is preserved, and capital is deployed where required without forcing a sale.

Conclusion

Securities based lending is not simply a way to access liquidity. It is a structured solution where outcome is determined by LTV, asset quality, and control.

Used correctly, it allows capital to be raised without forcing a sale. Used poorly, it introduces pressure at the wrong time.

The difference is structure.

Next Steps

If you are managing a concentrated position and liquidity is required without reducing exposure, there are ways to structure this properly.

Each situation is driven by the underlying asset, liquidity profile, and required flexibility. If relevant, you can discuss your position here: contact us

Securities Based Lending Playbook

For a structured view of how these facilities are assessed and executed in practice, see Securities Based Lending Playbook