Borrow Pledge vs Repo: Legal Structure and Risk in Securities-Based Lending

Most borrowers approach securities-based lending as a collateral question: what can be pledged, at what LTV, on what terms. The legal structure governing how that collateral is held is treated as administrative detail. In a stress event, that assumption can be expensive.

The borrow pledge vs repo distinction determines whether a lender can liquidate your securities without court approval, whether your collateral can be sold to a third party during the loan term, and what your recovery position is if the lender itself fails. Two structurally identical loan facilities can produce materially different outcomes depending on which legal architecture sits underneath them. How securities-backed loans work operationally is covered upstream.

This post addresses the legal structure that governs what actually happens when conditions change, across two axes: ownership and enforcement on default, and settlement mechanics and operational exposure during the term.

The Legal Difference Between Borrow Pledge vs Repo

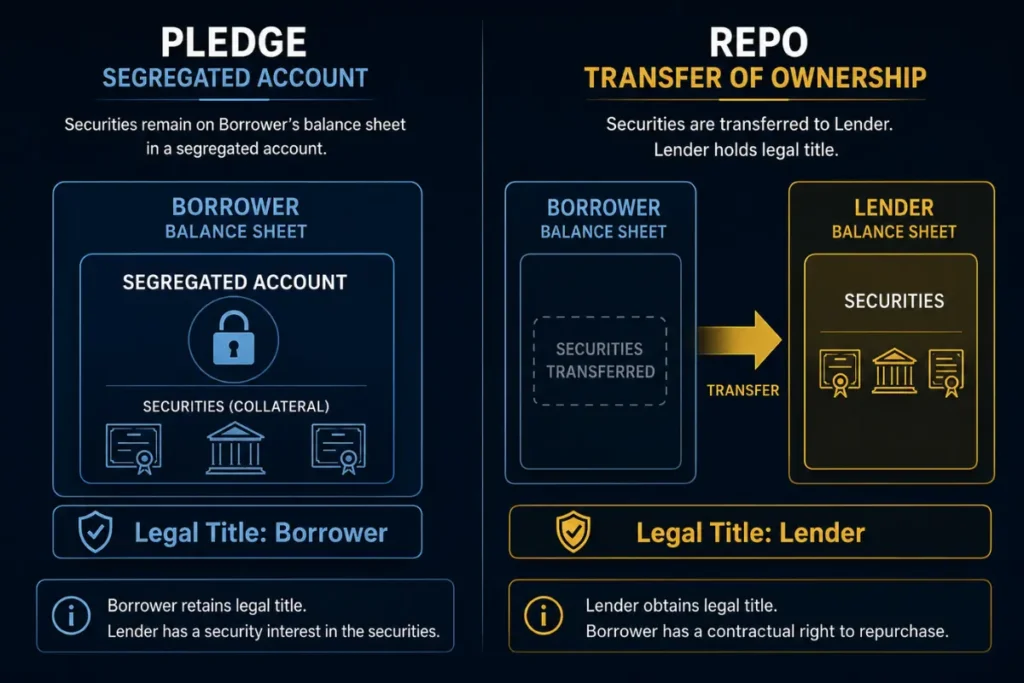

In a pledge arrangement, the borrower retains legal ownership of the securities throughout the loan term. The lender receives a security interest: a conditional right to enforce against the collateral on default. Legal title does not move. The lender holds a charge or lien, not ownership.

In a repo (repurchase agreement), the borrower sells the securities outright to the lender at an agreed price, with a simultaneous contractual commitment to repurchase equivalent securities on a future date. The difference in the prices is the implied repo rate. Legal title transfers at outset. The cash lender becomes the legal owner from the moment the transaction settles. The borrower holds a contractual right to buy back equivalent securities, not a proprietary claim over the original ones.

This single distinction drives every material difference in enforcement, counterparty exposure, and operational mechanics that follows in any borrow pledge vs repo structure.

Collateral Reuse, Rehypothecation and GMRA in Borrow Pledge vs Repo

Once title transfers in a repo, the cash lender can deal freely with the securities during the term: sell them, pledge them to a third party, or use them as collateral in another repo transaction. This is rehypothecation. It is a structural feature of institutional repo markets, not an edge case. A dealer receiving securities under a repo will typically reuse them immediately to fund the cash it has passed to the original borrower. The securities move through a chain of counterparties before the end date arrives.

Under a pledge in a borrow pledge vs repo arrangement, the lender holds a security interest, not ownership. On execution, the shares are transferred into a custodian account held by or on behalf of the lender. What the lender does with that position during the term varies by structure and institution and is not typically disclosed. Lenders hedge in some capacity, which is what makes competitive fixed rates commercially viable. The borrower retains legal title, voting rights, and dividend entitlements, with dividends typically applied against the outstanding loan.

The GMRA: Three Features Borrowers Need to Understand

The GMRA (Global Master Repurchase Agreement) governs most international repo transactions and is the document where these mechanics are formalised.

Close-Out Netting

On a default event, the GMRA allows all outstanding repo transactions between the same counterparties to be terminated and netted simultaneously into a single net cash obligation. This eliminates the need for the non-defaulting party to obtain court approval before acting.

Bankruptcy-Remote Design

Because legal title has already transferred, the cash lender owns the securities on default. The GMRA’s close-out provisions are structured to survive insolvency of either party without requiring stay relief.

Rehypothecation Chain Exposure

The GMRA does not eliminate chain exposure. Close-out netting protects the bilateral position between the two named parties only. If the cash lender has reused the securities and a third-party counterparty in that chain fails to deliver, the borrower’s right to receive equivalent securities on the repurchase date may be delayed or constrained. For a full technical treatment, the ICMA FAQ on Repo is the authoritative reference.

Under a pledge, the specific securities posted remain identifiable as the borrower’s property throughout the term. No chain exposure, no reuse risk, no question of receiving back equivalent rather than original securities.

Insolvency Risk: Two Failure Scenarios

If the borrower defaults

Under a pledge, the lender enforces its security interest through the applicable insolvency process. In most jurisdictions, an automatic stay applies: the lender must follow defined legal procedures before liquidating the collateral. The process takes time and is subject to court supervision.

Under a repo, the cash lender already holds legal title. On a default event as defined in the GMRA, it exercises its right to sell securities it owns. There is no stay, no court approval required, and no procedural delay. Enforcement is immediate.

If the lender fails

This is the scenario most UHNW borrowers do not model at execution. Under a pledge, the borrower’s securities are not part of the lender’s estate. They were never owned by the lender. The borrower retains legal title and can recover the specific securities on repayment, even through the lender’s administration. The claim is proprietary, not contractual.

Under a repo, the securities are the lender’s property at the point of failure. The borrower holds a contractual right to receive equivalent securities on the repurchase date. That right ranks as an unsecured creditor claim against the insolvent estate. In a disorderly failure, equivalent securities may not be immediately available, recovery through administration takes time, and full value is not guaranteed.

This asymmetry was made visible during the 2008 counterparty failures, where repo borrowers found themselves as unsecured creditors rather than recovering collateral directly. The GMRA’s close-out netting provisions help, but they operate on the bilateral netted position, not on the recovery of original securities that may have been reused into a chain now disrupted by the failure. The interaction between collateral structure and enforcement mechanics in events of default provisions is addressed in more detail in this post.

Settlement Mechanics, Substitution Rights and Operational Exposure in Borrow Pledge vs Repo

Ownership and insolvency are the first axis. Settlement mechanics and operational exposure during the term are the second, and they are rarely discussed with borrowers before execution.

Margining and variation

Both borrow pledge vs repo structures involve ongoing mark-to-market of the collateral position. In a pledge, additional collateral or partial repayment is required when LTV thresholds are breached: a margin call on the existing loan structure. In a repo, the equivalent mechanism is a margin call against the repo agreement, typically requiring the delivery of additional securities or cash to restore the haircut position. The practical effect is similar, but the legal basis differs. In a pledge, the margin call is a demand under the loan facility. In a repo, it is a contractual variation under the GMRA, with defined timeframes and failure-to-margin provisions that can themselves trigger close-out.

Substitution rights

In a repo, the borrower may negotiate a right of substitution: the ability to replace the originally delivered securities with equivalent eligible collateral during the term. This is operationally useful where the borrower needs to sell or reposition the original securities during the repo period. Whether this right is available and on what terms depends on the specific agreement. In a pledge structure, substitution of collateral is also possible but requires lender consent and a variation of the security documentation. Neither is automatic. Both require negotiation at term sheet stage.

Custody and segregation

Under a pledge, securities typically sit in a segregated custody account, identifiable as the borrower’s property and protected from the lender’s own creditors. Under a repo, the securities are on the buyer’s balance sheet. They may sit in the lender’s own custody account, commingled with its proprietary holdings. The operational risk during the term, including errors, settlement failures, or systems issues at the custodian level, is the lender’s to manage but the borrower’s exposure if it affects delivery on the repurchase date.

Lender Incentives: Why Structure Choice Reflects Book, Not Preference

Lenders do not choose between borrow pledge vs repo on borrower convenience grounds. The choice reflects their capital treatment, balance sheet infrastructure, and the nature of their lending operation.

Dealers and prime brokers

Large institutional dealers and prime brokers operate repo as the default structure for securities financing. Title transfer reduces their regulatory capital requirements under Basel III treatment of secured exposures. The reuse right is commercially active: securities received under repo are immediately deployed into the dealer’s collateral book to generate further revenue. The GMRA’s close-out efficiency reduces the dealer’s operational cost in a default scenario. For a collateral desk running hundreds of positions across general collateral and specials, the pledge structure is operationally incompatible with the trading book. Repo is not a product choice; it is how the infrastructure works.

Private banks and specialist SBL lenders

Private banks and specialist securities-based lenders serving UHNW borrowers typically operate on a pledge basis. The bilateral nature of the transaction, the size of individual facilities, and the custody relationship with the client all point toward a structure where securities remain in a segregated account, the borrower retains legal title, and enforcement follows a defined process. This is the architecture underlying most Lombard loan facilities in the private banking context. The lender does not have a reuse infrastructure to activate. The security interest is sufficient to manage its risk.

Scenario: Family Office, Listed Equity Position, Two Structures

A family office holds a concentrated FTSE 100 position and requires liquidity for a co-investment commitment. Two term structures are on the table.

Under the first, the shares are pledged to a specialist private lender. The family office retains legal title throughout the term. The shares sit in a segregated custody account. The lender holds a security interest and follows defined enforcement procedures on default. If the lender encounters difficulty during the term, the shares are not part of its estate. The family office has a proprietary recovery claim.

Under the second, a large institutional counterparty proposes a repo under a GMRA. The shares are sold at a price representing 70% of current market value, with a contractual obligation to repurchase equivalent shares at the end of the term at a higher price. Title transfers immediately. The institution is free to reuse the shares during the term. The family office holds a repurchase right, contractual in nature, against a counterparty it has not previously transacted with.

The risk profile across the two structures differs materially: unsecured creditor status in a lender failure against a proprietary recovery claim from a segregated account. The family office takes the pledge structure.

The correct decision varies by counterparty credit quality, duration, facility size, and the borrower’s actual failure tolerance. The analysis has to be run on the specific transaction. The point is that it must be run, and for corporate borrowers holding shares above a regulatory disclosure threshold, repo is frequently not an option at all.

Key Structuring Questions Before Accepting a Repo vs Pledge Structure

Does legal title transfer at any point during the term? If yes, the transaction is a repo regardless of commercial labelling.

Does the lender have a contractual right to reuse, rehypothecate, or re-pledge the collateral during the term? Rights vary by agreement. If such rights exist, the borrower’s exposure extends to the lender’s counterparty chain.

What is the margin call mechanism and what triggers close-out? Under a GMRA, failure to meet a margin call can itself constitute a default event triggering immediate close-out netting.

What substitution rights exist, if any, and on what terms are they exercisable?

What is the custody and segregation arrangement for the securities during the term?

What is the borrower’s recovery position if the lender becomes insolvent? Proprietary claim over specific securities, or unsecured contractual creditor of the estate?

Conclusion

The borrow pledge vs repo decision is two decisions, not one. The first is the ownership and insolvency axis: who holds legal title, what enforcement rights exist on default, and what the recovery position is if the lender fails. The second is the operational axis: whether collateral can be reused, how margining and substitution work during the term, and what chain exposure is introduced by title transfer.

For most UHNW borrowers transacting with specialist private lenders, the pledge structure is the operational default and the insolvency risk profile is manageable. For borrowers accessing institutional repo markets, the structure reflects real advantages for the lender that come directly at the borrower’s expense in a stress scenario.

The decision is made correctly at term sheet stage, with both axes fully mapped, not retrospectively when enforcement mechanics are the immediate question.

If you are evaluating a securities-based lending structure and want to ensure the terms reflect your interests rather than your lender’s default template, we welcome a discreet conversation. Contact us

For a more structured breakdown of how these strategies are applied in practice, see the Securities-Based Lending Playbook.