Blue Chip Shares as Collateral: What Lenders Actually Assess Before Lending

Two investors present portfolios of similar nominal value. Both hold blue chip shares on approved exchanges. Both secure facilities. The difference is not eligibility. It is position size relative to trading volume, and that difference determines LTV, structure, and terms.

Blue chip is a borrower’s label. Lenders do not use it. What they assess is liquidity, position size relative to trading volume, custody structure, and enforceability. These four factors determine whether a position is financeable, at what LTV, and on what terms. Understanding this distinction changes how UHNW investors and family offices approach collateral selection and facility structuring.

This post covers what lenders actually assess when blue chip shares are offered as collateral, why the same stock can produce very different outcomes depending on position size, and which structuring decisions affect the quality of the facility.

For the mechanics of how a securities-backed lending facility is structured from the borrower’s side, see Securities Based Lending 2026: Structure and Risk.

Why Position Size, Not Quality, Determines Terms on Blue Chip Shares

Blue chip shares are the strongest collateral in securities-based lending. They are liquid, globally recognised, and accepted by lenders on approved exchanges without question. Eligibility is not the issue.

The only variable is position size relative to average daily trading volume. A large concentrated position in even the most liquid blue chip stock will attract different terms from a smaller holding in the same name. The lender is not assessing the quality of the asset. They are assessing how efficiently they can exit it if required.

This is the distinction that matters. Two investors holding the same stock can receive materially different LTV offers based entirely on the size of their position relative to the market. Understanding that dynamic is what allows borrowers to structure facilities that reflect the true value of their collateral.

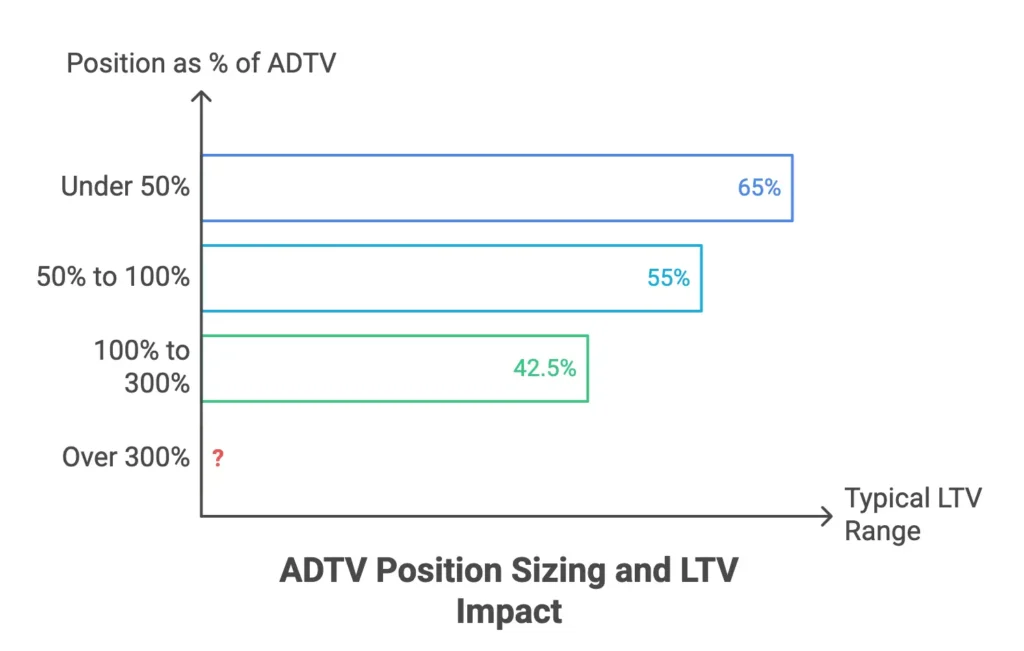

Average Daily Trading Volume: A Primary Underwriting Factor

Average daily trading volume, ADTV, is the single most important number in a blue chip shares assessment. It determines how large a position is relative to the market’s ability to absorb it, and therefore how quickly a lender could exit in a default scenario.

A £50M position in a stock trading £500M per day presents minimal execution risk. The same £50M in a stock trading £20M per day means the lender holds approximately 2.5 days of volume. Any attempt to exit quickly moves the price. The lender prices that execution risk directly into the LTV they offer.

Positions representing more than one day’s ADTV typically attract lower LTVs. Positions exceeding five days of volume will see terms tighten significantly, with lenders structuring facilities in tranches or stepping down LTV as position size increases. The holding remains financeable. The structure adapts to manage the execution risk.

For how LTV is determined across secured lending structures, see Loan to Value Ratio in 2026.

Position Concentration and the Haircut Methodology

Lenders assess concentration risk separately from liquidity. A borrower holding single blue chip shares representing the majority of their pledged assets presents a different risk profile from one holding ten positions across sectors and geographies.

Single-stock concentration affects terms in two ways. First, the lender’s exit risk is concentrated in one name. If that stock is under pressure at the time of a default, there is no diversification effect to absorb losses. Second, a large position in a single name may attract disclosure requirements or regulatory scrutiny depending on the borrower’s status and jurisdiction.

Haircuts on blue chip shares typically range from 20% to 40% of current market value, depending on ADTV, position size, stock volatility, and lender appetite. Borrowers expecting to borrow at 70 to 75% LTV against a concentrated position in a mid-liquidity stock will encounter friction. The facility may be structured in tranches, with LTV stepping down as position size increases relative to volume.For how concentrated equity positions are handled at the transaction level, see Stock Loans for Concentrated Shareholders.

Lender Insight: How Blue Chip Shares as Collateral Are Actually Assessed

Eligible exchanges and settlement infrastructure

Not all listed blue chip shares are eligible collateral. Lenders maintain approved exchange lists, and eligibility is driven by settlement reliability, enforceability of custody arrangements, and jurisdictional exposure. Shares listed on the LSE, Euronext, SGX or ASX will generally find lender appetite. Shares listed on thinner or emerging market exchanges may not, regardless of headline market capitalisation.

Settlement infrastructure also affects speed and cost. A lender assessing CREST-eligible UK equities is working within a known, efficient framework. Cross-border positions involving multiple depositories introduce complexity that affects both feasibility and pricing. Borrowers who assume that a major international listing guarantees acceptance should confirm eligibility before progressing a mandate.

Volatility assessment and margin call architecture

Lenders build margin call thresholds into every blue chip shares facility. The mechanics vary, but the principle is the same: if the collateral value drops below a defined floor, the borrower must either top up collateral or reduce the outstanding loan balance.

For shares with low historical volatility, these thresholds may sit at 10 to 15% below the initial collateral value. For more volatile names, lenders set wider buffers. The borrower’s ability to meet a margin call without liquidating other assets is factored into facility design. A blue chip stock that falls 25 to 30% in a market correction, which is not unusual, can breach margin thresholds quickly if the facility was structured at full LTV from the outset. This is where the assumption that blue chip shares means low-risk collateral breaks down in practice.

Corporate actions and dividend treatment

Lenders specify how corporate actions are handled during the loan term. Rights issues, special dividends, share splits, and merger events all affect collateral value and require clear contractual treatment. For borrowers who depend on dividend income from pledged positions, the treatment of distributions during the pledge period is a material term.

Well-structured facilities retain beneficial ownership and pass dividends through to the borrower. Poorly structured ones may not. This is an area where documentation quality separates sound transactions from problematic ones, and where borrowers working through an experienced intermediary consistently achieve better outcomes than those approaching lenders directly.

Insider status and regulatory constraints

A borrower who is a director, significant shareholder, or insider in the company whose shares are being pledged faces additional constraints. Pledging shares during a closed period, or without appropriate disclosure where required, creates regulatory exposure for both the borrower and the lender.

Lenders with institutional infrastructure screen for this at origination. They will not proceed if the transaction creates compliance risk for themselves or the counterparty. This is not a barrier to execution in most cases, but it is a structuring consideration that needs to be addressed early. Timing, disclosure planning, and documentation are as important as collateral quality when insider status is a factor.

What Structuring Decisions Affect Facility Quality

Three decisions have the most material effect on the quality of a blue chip shares lending facility.

LTV versus tranche structure: a single facility at maximum LTV creates higher margin call exposure than a tranched structure where borrowing steps up over time. For large concentrated positions, tranching reduces the risk of a single price movement triggering a default or forced reduction.

Recourse structure: non-recourse facilities limit the lender’s claim to the collateral itself. Full recourse extends liability beyond the pledged shares. The recourse structure affects pricing, and borrowers should understand precisely which structure they are being offered before proceeding to documentation.

Custody arrangement: the shares must sit in a custody account acceptable to the lender that clearly preserves the borrower’s beneficial ownership and rights over dividends and corporate actions. Custody is not an administrative detail. It is the foundation of the transaction, and weak custody arrangements create execution risk at default, which lenders price into terms or decline to accept.

For more on how custody and control interact with more complex collateral structures, see Cross Collateralisation in Private Credit 2026.

Lender Appetite Across Jurisdictions

Lender appetite is determined by the exchange the stock is listed on, not where the borrower is domiciled. Shares listed on recognised exchanges, including the LSE, Euronext, ASX, SGX and Hong Kong Stock Exchange, will find lender appetite. Shares listed on some emerging market exchanges will not, regardless of trading volume or market capitalisation.

The two criteria lenders apply are simple: is the exchange on their approved list, and does the position size work relative to ADTV. Borrower domicile is irrelevant.

The Bank for International Settlements has published detailed research on securities financing transactions and collateral markets, which provides useful context on how cross-border collateral arrangements are assessed globally.

For how lenders assess risk exposure across different market conditions and counterparty profiles, see Liquidity Risk in Lending 2026.

Conclusion

Blue chip shares are accepted collateral. The variables are LTV, position size, trading volume, custody structure, and margin architecture. These determine the terms on offer, not the quality of the underlying name.

Investors who understand how position size affects structure enter negotiations from a stronger position. Those who approach lenders without that understanding consistently encounter friction that could have been anticipated at the outset.

If you are evaluating a blue chip share lending facility and want to ensure the structure reflects the collateral’s actual market position, we welcome a discreet conversation. Lets talk

For a more structured breakdown of how these strategies are applied in practice, see the Securities-Based Lending Playbook.