Non Recourse Loan: Structural Differences That Matter in Securities Based Lending

A non recourse loan limits the lender’s recovery to the pledged collateral. If that collateral falls short on liquidation, the shortfall stays with the lender. The borrower walks away. In a recourse structure, the lender can pursue the borrower’s remaining assets to cover any gap.

For a borrower structuring a loan against a concentrated equity position, that distinction changes the risk profile of the entire transaction: the LTV, the margin call mechanics, the interest rate, and the legal exposure if the position moves against them. Most commentary on non-recourse financing focuses on commercial real estate and project finance. In securities lending, the structural dynamics are different and the borrower protections, where they exist, are more conditional.

This post covers how a non recourse loan works in a securities-based lending context, where lenders draw the line, and what borrowers need to examine before they commit to either structure. For broader context on securities-backed loan structures, see Securities Based Lending 2026: Structure and Risk.

Non Recourse Loan vs Recourse: How They Differ in Practice

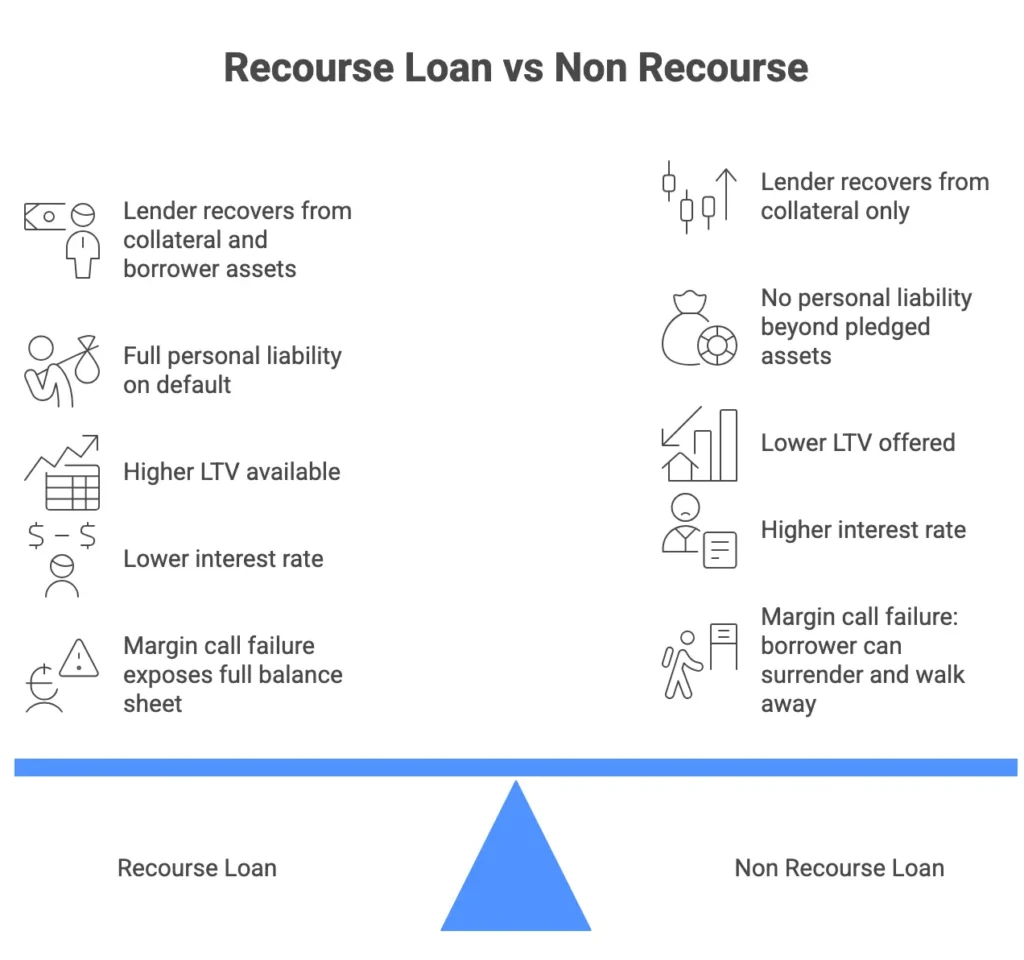

In a recourse loan secured against a share portfolio, the lender holds two lines of recovery: the collateral itself, and the borrower’s broader asset base if the collateral proves insufficient on liquidation. Personal liability survives the default.

In a non recourse loan, the lender is limited to the collateral. If the portfolio is liquidated and the proceeds fall short of the outstanding balance, the lender absorbs the loss. The borrower has no further obligation.

The commercial consequence is direct. Non-recourse financing transfers credit risk from the borrower to the lender. Lenders price that transfer into the terms: lower LTV ratios, higher interest rates, and more stringent approval criteria. A borrower seeking non-recourse terms is asking the lender to carry the tail risk. The lender will be compensated for doing so.

For a borrower holding a large or concentrated position, that pricing premium may be the right trade. The alternative is a recourse structure where a severe market dislocation exposes personal assets well beyond the pledged portfolio.

Non Recourse Loan LTV: What Borrowers Should Expect

Loan-to-value ratios in non-recourse stock lending are materially lower than in comparable recourse arrangements. Where a recourse lender might extend 60 to 70 percent LTV against a liquid blue-chip portfolio, a non recourse loan against the same collateral is more likely to come in at 50 to 60 percent, depending on the stock, the concentration, and the liquidity profile.

The logic is straightforward. In a recourse structure, residual lender exposure is backstopped by the borrower’s personal balance sheet. In a non-recourse structure, the collateral is the only protection. The LTV must embed enough buffer to absorb a significant market move without leaving the lender in deficit.

For borrowers, this has a direct impact on available proceeds. A lower LTV against the same portfolio means less capital released. Where the objective is maximum liquidity, recourse structures deliver more. Where the objective is to cap personal legal exposure, the lower proceeds of a non recourse loan facility are the price of that protection.For context on how LTV is assessed across different collateral types, see Loan to Value Ratio in 2026.

Non Recourse Loan: Margin Call Mechanics

Margin call mechanics differ significantly between recourse and non-recourse stock loans. This is where borrowers most commonly misread their exposure.

In a recourse arrangement, a lender facing a collateral shortfall during a market decline can issue a margin call requiring the borrower to top up the collateral or repay a portion of the loan. Failure to comply triggers a default. The lender can then pursue both the collateral and the borrower’s other assets.

In a non recourse loan, the lender still includes margin call provisions in most agreements. The critical difference is the consequence of non-compliance. A borrower who cannot meet a margin call can elect to surrender the collateral and walk away. No further liability attaches.

That walk-away right is the defining feature of non-recourse financing from a borrower’s perspective. It functions as an embedded put option: the borrower retains the upside if the portfolio recovers and can exit the liability by surrendering collateral if it does not. That optionality carries real value, particularly where the collateral is a concentrated position with meaningful downside risk in adverse conditions.

For more on how stock loans are structured around concentrated equity positions, see Stock Loans for Concentrated Shareholders.

The following summarises the key structural differences between a recourse and non recourse loan.

Bad Boy Carve-Outs: When a Non Recourse Loan Converts to Full Recourse

Non-recourse protection is not unconditional. Most non recourse loan agreements include what practitioners refer to as bad boy carve-outs: defined circumstances in which the loan converts from non-recourse to full personal recourse.

Standard carve-outs typically include:

- Fraud or material misrepresentation in the loan application or ongoing financial reporting

- Intentional or negligent damage to or disposal of pledged assets

- Unauthorised transfer of collateral without lender consent

- Voluntary bankruptcy filings where prohibited under the agreement

- Breach of restrictive covenants that materially impair the lender’s security position

The carve-outs exist to protect the lender against deliberate or negligent borrower conduct that undermines the collateral. A borrower acting in good faith, maintaining accurate disclosures and preserving the pledged assets throughout the loan term is unlikely to trigger them.

What borrowers must do is read the carve-out schedule carefully before signing. Poorly drafted clauses can extend recourse liability to scenarios that are neither fraudulent nor intentional. Broad language around “material misrepresentation” can, in some agreements, encompass a forward-looking projection that proves inaccurate, even where no deliberate misstatement occurred. Legal review of the carve-out schedule is not optional. It defines precisely where non-recourse protection ends.

Lender Insight: Why Non Recourse Loan Terms Are Selective

True non recourse loan facilities against equities, or a portfolio are available, but the market is narrow and lender appetite is specific. Understanding how lenders approach the category helps borrowers assess what is genuinely on offer versus what is marketed as non-recourse but structured otherwise.

Lenders reserve non recourse loan terms for highly marketable, listed securities with deep liquidity and an established trading history. Single-stock positions in less liquid names, shares subject to lock-up restrictions, or portfolios with significant sector concentration will either attract punitive LTV haircuts or be declined. The lender’s recovery in a default scenario depends entirely on their ability to liquidate the collateral cleanly. Anything that complicates that process transfers risk the lender is unwilling to carry on non-recourse terms.

Many facilities described as non-recourse in the market include covenant structures that function as quasi-recourse in practice. Aggressive cure periods on margin calls, personal guarantee requirements for bad boy events, or cross-default provisions linked to the borrower’s other borrowing can collectively recreate the economic effect of a recourse loan while preserving the non-recourse label. Borrowers should examine the full agreement, not the product description.

Lender appetite also varies considerably by jurisdiction. Securities lending regulations, enforcement mechanisms, and collateral realisation timelines differ across the UK, Europe and Asia-Pacific. A lender operating in multiple jurisdictions will price non-recourse risk differently depending on how quickly and reliably they can enforce in each market.

Finally, because the non recourse loan market for equity-backed lending is less commoditised than the recourse market, terms vary materially between providers. Comparing what is genuinely on offer requires understanding how these facilities are structured and priced from the outset. See How Do Securities-Backed Loans Work?

Scenario: Structuring a Non Recourse Loan Against a Concentrated Position

A founder holds a listed technology stock worth approximately GBP 18 million. The position represents the majority of their liquid net worth. They want to release capital for a property acquisition without triggering a taxable disposal.

Under a recourse structure, a lender might offer 65 percent LTV, releasing approximately GBP 11.7 million. The founder retains upside in the shares but carries full personal liability if the position falls sharply and margin calls cannot be met from other assets.

Under a non recourse loan at 45 percent LTV, the facility releases approximately GBP 8.1 million. The founder releases less capital but carries no personal liability beyond the pledged shares. If the technology stock falls 60 percent, the founder surrenders the position and exits the loan with no further obligation.

The decision turns on three things: the founder’s assessment of downside risk in that specific stock, their personal balance sheet strength outside the position, and whether GBP 8.1 million is sufficient to meet the acquisition requirement. Where the equity position is already highly correlated to the founder’s broader personal wealth, recourse exposure becomes disproportionately risky: a sharp fall in the stock damages both the collateral and the wider balance sheet simultaneously, which is precisely when a recourse lender will call. Neither structure is inherently superior. Both have a defined place depending on the risk profile of the borrower and the collateral.

What to Consider When Choosing Between Recourse and Non Recourse Loan

Personal Liability Tolerance

If the pledged collateral represents a significant proportion of net worth, non-recourse terms set a hard boundary on downside exposure. Borrowers with substantial assets beyond the collateral may find recourse terms commercially acceptable and will typically access better LTV.

Collateral Concentration and Volatility

Single stock or sector concentrated positions carry higher tail risk than diversified portfolios. A non recourse loan is better suited to concentrated collateral where a severe drawdown is a credible scenario.

Proceeds Requirement

If the transaction requires maximum LTV, recourse structures will typically deliver more. If the capital requirement can be met at a lower LTV, the non recourse loan premium may be commercially justified.

All-In Cost Over Term

Non recourse facilities over longer periods carry more lender risk and attract a wider rate premium. Assess the total cost of the facility over the intended loan period, not just the headline rate.

Bad Boy Carve-Out Scope

Review every carve out in the loan agreement with legal counsel before signing. The breadth of the carve-out schedule determines the real scope of non recourse loan protection.

Lender Selection

The non recourse loan market for equity backed lending is thinner than the recourse market. Terms vary significantly between providers. Independent advice on lender selection is valuable here.

Conclusion

In securities-based lending, structure determines outcome. In a non recourse loan, the real negotiation is where liability ends when markets move against the collateral. Getting that right is more consequential than the rate.

If you are evaluating a non recourse loan structure and want to ensure the terms reflect your interests, contact us for a discreet conversation.

For a more structured breakdown of how these strategies are applied in practice, see the Securities-Based Lending Playbook.