Commercial Real Estate Financing: 9 Steps to Structure and Place Your Transaction

Most commercial real estate financing deals that fail to close do not fail on price. They fail because the debt structure was wrong from the start: the wrong lender type approached at the wrong stage, the wrong position in the capital stack, or a borrower presentation that invited credit questions it was not prepared to answer.

This post sets out the nine steps that govern how commercial real estate financing is structured and placed, from defining the transaction objective through to close. It is written for borrowers, family offices and advisors who want to approach the financing process with the same rigour lenders bring to their credit assessment.

The core metrics and loan fundamentals that underpin these steps are covered in Real Estate Finance Basics. This post assumes that grounding and focuses on process.

Why Commercial Real Estate Financing Demands a Structured Approach

Private credit lenders and institutional debt funds assess CRE transactions against criteria that reward preparation and penalise vagueness. A borrower who arrives with an unclear objective, an incomplete data pack, or a capital structure that has not been thought through does not receive credit: they receive questions, delays and unfavourable terms.

The nine steps below are sequential for a reason. Treating the financing process as a single conversation rather than a structured sequence is the most consistent cause of failed or mispriced transactions.

Step 1: Define the Transaction Type and Financing Objective

Before approaching any lender, define precisely what the financing must achieve. Acquisition, refinance, development, bridge to stabilisation and cash-out recapitalisation each carry different risk profiles, preferred lending channels and acceptable leverage levels.

The financing objective should define not only the purpose of the loan, but also the intended repayment source, target hold period and acceptable leverage range. These three parameters shape every subsequent decision: which lending channel is appropriate, how the capital stack should be constructed, and what exit thesis will be presented to credit.

A refinance on a stabilised, income-producing asset sits at a fundamentally different point in the credit risk spectrum than a speculative development loan. Presenting a bridge requirement to a lender whose book is weighted towards stabilised senior debt wastes time and signals a lack of preparation.

Step 2: Evaluate the Asset Income Profile and Debt Serviceability

Lenders underwrite cash flow first, asset value second. The Debt Service Coverage Ratio is the primary lens through which income-producing CRE is assessed. Most senior lenders require a minimum DSCR of 1.20x to 1.30x at underwriting, with some private credit lenders applying different thresholds on assets with strong sponsorship or clear near-term upside.

Before entering any lending conversation, scrutinise the rent roll, weighted average lease expiry, tenant credit quality and void rates. Lenders will stress-test vacancy and cap rate assumptions independently. If you do not have confident answers to those questions, the credit process will surface the gaps after heads of terms have been agreed.

Property type also shapes assessability. Logistics, multifamily and healthcare assets attract the broadest lender appetite across the UK, European and Asia-Pacific markets. Offices, retail and hospitality require stronger in-place fundamentals and more precise positioning to secure competitive terms.

Step 3: Establish the Capital Requirement and Target LTV

Define the gross capital requirement, the equity contribution available and the maximum LTV you are targeting before approaching lenders. These three figures determine which lending channels are viable and whether additional debt layers are needed to close the gap.

Senior secured CRE lending in the UK and European market typically ranges from 50% to 65% LTV on stabilised assets, depending on property type, geography and lender appetite. Development and transitional assets attract lower leverage. Any gap between senior debt proceeds and the required capital should be mapped to mezzanine, preferred equity or co-investment before the process begins, not identified mid-transaction when pressure to close is at its highest.

In practice, a family office acquiring a stabilised logistics asset might target senior debt at 60% LTV and reserve mezzanine capacity only if acquisition timing requires additional leverage to close. That decision is made at this step, not during lender negotiations.

For a detailed treatment of how LTV is calculated, tested and negotiated in practice, see Loan to Value Ratio in 2026.

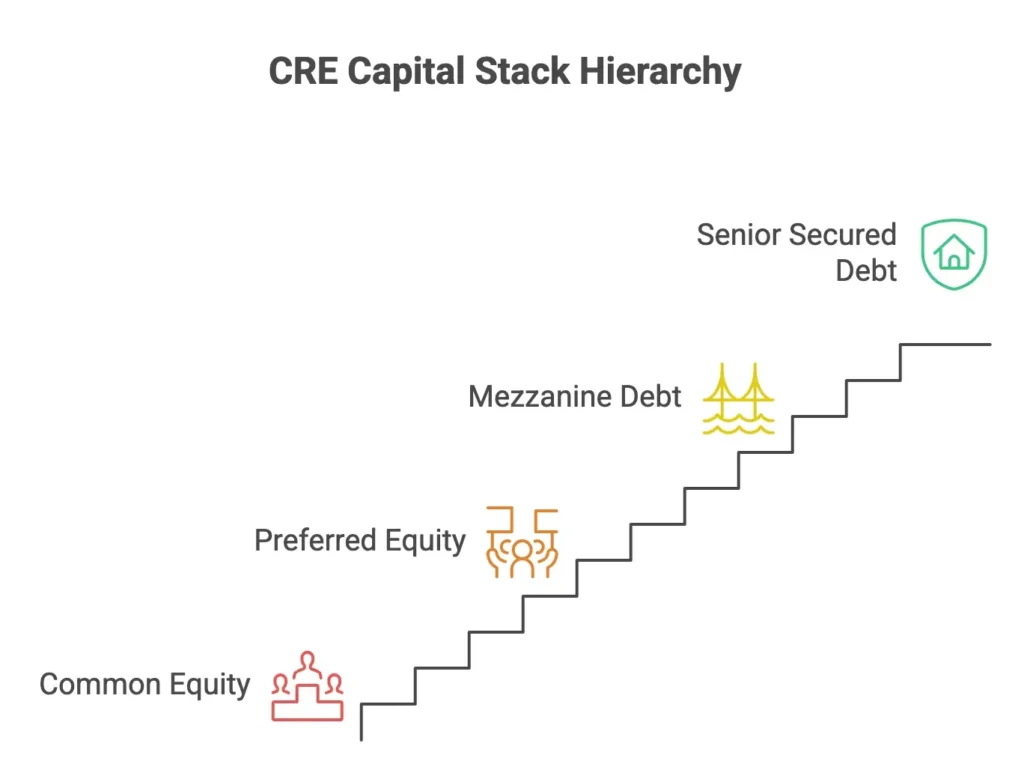

Step 4: Map the Capital Stack and Identify Commercial Real Estate Financing Channels

The capital stack in commercial real estate financing runs from senior secured debt at the base through to common equity at the top. Each layer carries distinct risk, return and security characteristics. Structuring it correctly before lender engagement is not optional: most institutional lenders ask immediately whether an intercreditor arrangement is in place and who holds the junior positions.

Senior lending channels include clearing banks, insurance companies, specialist debt funds and CMBS conduits. Each has different appetite by asset type, geography, loan size and complexity. Private credit and debt funds dominate the transitional, value-add and development space. Insurance companies and banks focus on stabilised income assets at conservative leverage. Mezzanine and preferred equity sit above senior debt and are deployed where senior LTV creates a funding shortfall.For a structured breakdown of how the CRE capital stack is assembled and layered, see Structured Finance in Commercial Real Estate and Mezzanine Financing in Real Estate.

Step 5: Prepare the Borrower Presentation and Data Pack

A lender’s initial assessment is formed by the quality of the presentation, not the asset alone. A poorly packaged borrower creates uncertainty, which lenders manage through higher pricing, tighter covenants or additional credit enhancements.

The borrower pack for a commercial real estate financing transaction should include: a property overview with financial performance history, a current rent roll with lease expiry schedule, a three-to-five year income projection with assumptions stated explicitly, a capital stack diagram, sponsor track record and credentials, and an exit analysis with supporting market evidence.If the asset carries material voids, planning risk or near-term lease expiries, address those directly in the pack rather than relying on lenders to overlook them. The full scope of what lenders expect in a borrower submission is covered in Borrower Due Diligence: The Power Move.

Step 6: Approach Lenders and Run a Structured Process

Running a structured lender process is not the same as sending the same information memorandum to ten lenders simultaneously. Identify lenders whose published appetite, deal size parameters and property type focus align with the specific transaction. A targeted process of four to six appropriately selected lenders, approached with a clear IM and a defined timetable for responses, will generate better terms and faster execution than a wide scatter approach.

In the UK and European market, private credit funds and specialist debt funds have materially expanded their appetite for CRE lending since 2022, particularly for assets where clearing bank appetite has been constrained by regulatory capital requirements. The Bank of England’s financial stability monitoring has consistently flagged commercial real estate as a systemic exposure, a signal that mainstream lender appetite will remain cycle-sensitive and selective. Borrowers who run a disciplined lender process capture the competition that still exists in the private credit market for quality assets at the right leverage point.

How Lenders Assess Commercial Real Estate Financing in 2026

Private credit lenders approach commercial real estate financing assessment differently from clearing banks, and understanding those differences before entering a lending conversation materially improves outcomes.

The first factor is exit clarity. Private credit lenders underwrite to the exit, not the entry. They want to understand precisely how the loan will be repaid: sale, refinance, portfolio recapitalisation or income sweep over a defined hold period. An unclear or over-optimistic exit thesis is the fastest route to lost lender confidence, regardless of how strong in-place income looks at entry.

The second is sponsor quality, assessed independently of the asset. In the UK and European private credit market, lenders run parallel tracks: one on the asset and one on the sponsor. A strong asset paired with an untested or financially stretched sponsor will attract defensive structuring, including tighter covenants, cash traps or guarantee provisions that a stronger sponsor would have avoided. Sponsor track record, co-investment and financial standing are underwriting inputs, not background information.

The third is asset liquidity and realisability under stress. Lenders assess not just current income, but how quickly the asset could be sold or refinanced at the loan value in an adverse scenario. Assets with thin secondary markets, structural obsolescence risk or concentrated tenant dependency attract conservative LTV and tighter cash management requirements, irrespective of current occupancy.

The fourth is debt yield. Calculated as net operating income divided by the loan amount, debt yield is independent of cap rate assumptions, which makes it a useful underwriting floor that does not fluctuate with valuation methodology. A debt yield below 7% on a transitional or higher-risk asset will create friction with most private credit lenders, regardless of stated LTV or in-place income.

Step 7: Review, Compare and Negotiate the Term Sheet

A term sheet is not a final offer. It is a negotiating document, and the terms accepted at this stage define the legal framework for the entire loan. The items that require particular scrutiny: margin and total cost of debt, extension options and the conditions attached to them, financial covenants (DSCR, LTV, interest cover), cash management and reserve requirements, prepayment penalties and change of control provisions.

Negotiating at term sheet stage is materially less costly than attempting to revise terms once the loan agreement is in solicitors’ hands. Engage specialist legal counsel before executing.

Step 8: Navigate Lender Due Diligence and Credit Approval

Once a term sheet is signed, the lender’s formal due diligence process begins. This covers: structural survey and building condition report, environmental assessment, independent property valuation by an approved valuer, title and legal structure review, corporate and financial due diligence on the borrowing entity, and in institutional processes, a formal credit committee presentation.Delays at this stage are almost always caused by incomplete data, valuation disputes or title issues surfaced late. A well-prepared data room, assembled before term sheets are issued, reduces the lender’s workload and compresses the timeline significantly. For a detailed breakdown of how private credit lenders assess borrower submissions through the credit process, see Private Credit Underwriting 2026.

Step 9: Execute, Close and Position for Ongoing Debt Management

Execution is not the end of the process. Loan covenants require ongoing compliance. Financial reporting obligations, cash management accounts, reserve top-up requirements and trigger events all require active management through the loan term.

Borrowers who treat debt management as an afterthought routinely encounter avoidable covenant breaches and forced conversations with lenders at the worst possible moment: when the asset is underperforming and the borrower’s negotiating position is weakest. Build the monitoring obligations into operational planning from the date of first drawdown.

Conclusion

The strongest commercial real estate financing structures are built backwards from the repayment event. Borrowers who understand how lenders assess exit risk, leverage and sponsor quality before the first lender conversation place themselves in a materially stronger position at every step that follows.

The nine steps above are a process framework, not a checklist. The outcome at each stage depends on the quality of preparation at the stage before it. Borrowers who follow that sequence consistently secure better terms, fewer conditions and faster execution, regardless of market conditions.

If you are structuring a commercial real estate financing and want to ensure the debt is correctly positioned before approaching lenders, we welcome a discreet conversation. Arrange a call. For a structured overview of how private credit is deployed across asset classes, see the Private Credit Playbooks.