Securities Based Lending Rates: How Lenders Price Uncertainty

Most borrowers approaching a securities based lending transaction focus on the interest rate. It is the number that appears in the term sheet summary, it is what gets compared across lenders, and it is what gets reported back to advisers and trustees when a transaction is being evaluated. What it does not tell you is what the transaction actually costs.

The rate is one component of a cost structure that includes several other items, some of which are deducted before the borrower receives a penny. Understanding how lenders price securities based lending rates, and what that means for net proceeds and total cost of capital, is the difference between evaluating a transaction properly and being surprised at closing. For a grounding in how these transactions are structured from the outset, see how securities-backed loans work.

How Securities Based Lending Rates are Set

The interest rate on a term stock loan is not derived from a benchmark rate in the way a Lombard facility at a private bank typically is. Private bank lending against diversified portfolios is usually priced as a floating margin over a reference rate, adjusted periodically with market conditions. A term stock loan against a single listed equity position is priced on a fixed simple interest basis for the duration of the loan term, and the economics are different enough that direct rate comparison between the two structures is not meaningful. For a full breakdown of how Lombard facilities work and where they differ, see how a Lombard facility works.

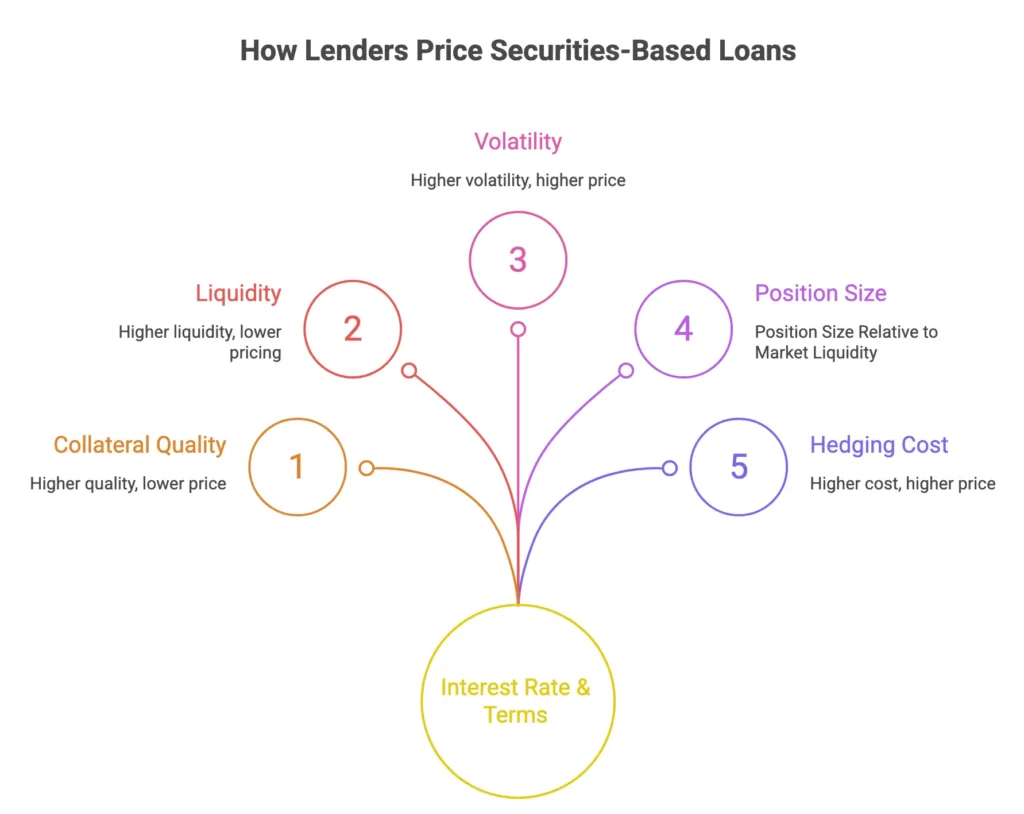

Lenders in this market set securities based lending rates based on several variables assessed at the point of underwriting: the quality and liquidity of the collateral, the size of the position relative to average daily trading volume, the volatility profile of the underlying stock, and the lender’s cost of hedging against the position once it is taken on. A borrower pledging a large-cap stock with deep liquidity and low historical volatility will receive a more competitive rate than a borrower pledging a mid-cap with thinner trading and higher price swings.

For context, securities based lending rates for well-structured transactions against quality collateral are typically more competitive than unsecured personal or corporate credit, and broadly comparable to or below asset-backed recourse lending, though above the floating margins available to a private bank client borrowing against a diversified managed portfolio. The relevant comparison is not consumer lending or margin lending: it is the cost of accessing liquidity against a concentrated single-stock position, where the available alternatives are limited.

Interest is calculated on a 360-day year basis and is generally payable quarterly in advance. That last point matters: the first interest payment is typically deducted from proceeds at closing. For a detailed look at the criteria lenders apply when assessing collateral quality and setting terms, see what lenders assess before approving a stock loan.

The Arranger or Origination Fee

The arranger fee is a one-time charge assessed on the principal amount being funded and deducted from loan proceeds at disbursement. It is typically agreed before documentation is drafted and confirmed in the loan documents, so the borrower knows the exact figure before committing to the transaction.

In our experience structuring these transactions, arranger fees typically sit in the range of 3% to 5% of the principal amount, though like most things, the figure can be negotiable, and on larger transactions some arrangers may accept a lower percentage.

The arranger fee exists because structuring and placing a term stock loan requires substantive work: lender placement, collateral assessment, documentation preparation, and coordination through to closing.

Lender Fees and Expenses

Separate from the arranger fee, lenders typically charge their own fees and expenses at closing. These cover internal costs: legal review, compliance checks, account setup, and the administrative costs of the custodial arrangements required to hold the collateral during the loan term. On a mid-sized transaction these are typically modest in absolute terms, but they are deducted from proceeds at closing alongside the arranger fee and the first interest payment.

Custodian Costs

The collateral in a pledged stock loan structure is deposited into a professional client brokerage account at a custodial firm designated by the lender. The cost of opening and maintaining that account, including any maintenance fees, transaction fees, or cross-trade costs on shares not pledged to the lender, is the borrower’s responsibility.

These costs are transaction-specific and depend on the custodian, the size of the position, and the duration of the loan. They are not large in absolute terms but represent a real ongoing cost that sits outside the headline rate and the closing deductions, and they are frequently overlooked in initial cost modelling. The structure of how collateral moves through a pledged transaction is covered in detail in the comparison of pledge and repo structures.

What the Securities Based Lending Rates and Numbers Actually Look Like

The cumulative effect of these deductions is best understood through a worked example showing what securities based lending rates and costs look like in practice.

Consider a borrower with a $10,000,000 loan amount agreed against a pledged single listed equity position:

Gross loan amount: $10,000,000 Arranger fee at 4%: ($400,000) First quarterly interest payment at 4% per annum: ($100,000) Lender fees and expenses: ($5,000) Net proceeds to borrower at closing: $9,495,000

The borrower has access to $9,495,000 on day one, with their shares retained, their position intact, and no personal liability attached to the facility.

Over a 36-month term at 4% per annum simple interest, the all-in cost of the transaction including the arranger fee and closing expenses is approximately $1,605,000. That is the price of accessing liquidity against a position the borrower has chosen not to sell, on a fixed rate that cannot be repriced, from a lender who cannot call the loan unless a documented event of default occurs.

Compare that to the alternative: selling a $10,000,000 position, crystallising a tax event, losing future upside, and exiting a holding that may have taken years to build. Or borrowing from a bank on a recourse basis at a floating rate that can be increased, restructured, or recalled at the institution’s discretion.

The all-in cost of approximately 5.3% per annum on a simple basis is not a discount. It is the market rate for certainty, protection, and retained ownership. For borrowers who understand what they are buying, it is frequently the most efficient decision available to them.

Lender Insight: Why Structure Determines Cost

The full cost of a term stock loan reflects the lender’s economics, and understanding how securities based lending rates are structured, is essential before comparing offers.

According to the Bank for International Settlements, securities financing transactions involve specific collateral management and risk transfer mechanisms that distinguish them structurally from conventional credit facilities. Those mechanisms have a cost, and that cost flows through to the borrower in the rate and fee structure.

A private bank Lombard facility against a diversified investment portfolio can carry no arranger fee and can operate as a revolving line with ongoing collateral visibility within an existing relationship. A term stock loan carries an arranger fee, fixed-term commitment, and hedging costs that the lender must recover. These are not equivalent structures priced at different levels: they are different instruments serving different collateral profiles.

For borrowers with a concentrated single-stock position, the term stock loan market offers something the private bank channel typically cannot: committed liquidity against a single listed equity holding, on a fixed rate, non-recourse basis, for a defined term. Private banks have appetite limits on concentrated positions, and where they do lend, the facility is rarely fixed rate or non-recourse. The term stock loan is not a fallback. It is a structurally distinct product serving a borrower profile that conventional lending does not address well.

The relevant question is not which structure is cheaper on rate. It is which structure delivers certainty, protection, and access for the collateral the borrower actually holds. For borrowers also evaluating a loan against an investment portfolio, the two approaches are complementary rather than competing.

The Cost of Early Exit

This is the component most frequently underestimated, and in some transactions it is the most significant cost of all.

Term stock loan agreements are structured for a fixed term and priced accordingly. Lenders price and commit to a transaction on the basis that it runs to maturity. If the borrower exits early, the lender incurs costs in unwinding their position. Those costs depend on market conditions at the time and can be substantial.

Most term stock loan agreements prohibit prepayment entirely during an initial period. After that period, prepayment is generally permitted only on specific anniversary dates and with substantial advance notice. A penalty applies, calculated as a function of outstanding principal and accrued interest to the term date.

Borrowers who enter a term stock loan expecting to exit at will, or who are planning to deploy the liquidity for a purpose that may resolve sooner than the loan term, need to understand this constraint before execution. The non-recourse nature of the loan does not translate to optionality on exit: the lender’s costs in unwinding their position are real and contractually recoverable.

What to Look for When Comparing Lenders

Not all lenders in this market set securities based lending rates the same way.

The interest rate is the most visible variable. It matters, but it is only one input into total cost of capital. The arranger fee percentage, the lender’s own closing costs, and the specific terms governing early exit are where the real differences between lenders emerge.

A lender offering a marginally lower interest rate but a higher arranger fee or more punitive exit provisions may be more expensive in total than one whose headline rate looks less competitive. This is particularly true where a borrower’s circumstances may change during the loan term and exit flexibility has real option value.

Working with an intermediary who places transactions across multiple lenders provides the ability to surface full-term comparisons rather than headline rates, and to identify which lenders’ risk appetite best matches the collateral profile. That changes the quality of the decision the borrower is making.

FAQ

What is a typical interest rate on a securities-based loan?

Securities based lending rates vary by collateral quality, position size, and lender. For well-structured transactions against liquid, large-cap collateral, rates in the private term stock loan market are typically more competitive than unsecured corporate credit and broadly comparable to asset-backed recourse lending. The headline rate is only one component of the total cost.

What fees are charged on a stock loan at closing?

The arranger fee is agreed before documentation is drafted and confirmed in the loan documents. At closing, it is deducted from loan proceeds alongside the first quarterly interest payment and the lender’s own fees and expenses. Together these deductions mean net proceeds to the borrower are below the agreed loan amount from day one.

Can I repay a stock loan early?

Most term stock loan agreements prohibit prepayment during an initial period. After that, prepayment is typically permitted only on anniversary dates with substantial advance notice and a penalty covering the lender’s costs in unwinding their position.

How does a stock loan rate compare to a Lombard loan?

A Lombard facility at a private bank is typically priced as a floating margin over a benchmark rate with no arranger fee, against a diversified managed portfolio. A term stock loan carries a fixed rate and reflects the concentrated single-stock collateral profile. The structures serve different borrower profiles and are not directly comparable on rate.

Conclusion

Securities based lending rates are one input into a cost structure that includes arranger fees, lender expenses, custodian costs, and early exit provisions, each of which affects the net economics of the transaction. Borrowers who evaluate rate in isolation will consistently underestimate total cost of capital and may enter transactions without understanding the constraints they are accepting.

The worked example above illustrates the point: a 4% interest rate on a $10 million loan translates to an effective all-in cost of approximately 5.3% per annum over the term when all closing deductions and fees are included. That is the number that deserves attention, not the headline rate alone.

If you are structuring a securities-based loan and want to ensure you are comparing lenders on a full-cost basis rather than headline rate, we welcome a discreet conversation. Get in touch.

For a structured overview of how securities-based lending works across different structures and collateral types, see the Securities-Based Lending Playbook.