Margin Call vs Stock Loan Explained: 2026 Structural Differences

The most important question when evaluating a securities-backed lending facility is not the interest rate. It is whether your lender can demand additional funds or liquidate your holdings at any point during the term, without your approval, based on daily market movements. To understand that risk, you need the margin call vs stock loan explained at a structural level, not as a retail brokerage definition.

Both formats use listed securities as collateral. Beyond that, the structural logic diverges significantly: in how LTV is enforced, how risk is allocated between borrower and lender, and what happens when markets move against you.

Margin Call vs Stock Loan Explained: The Core Structural Difference

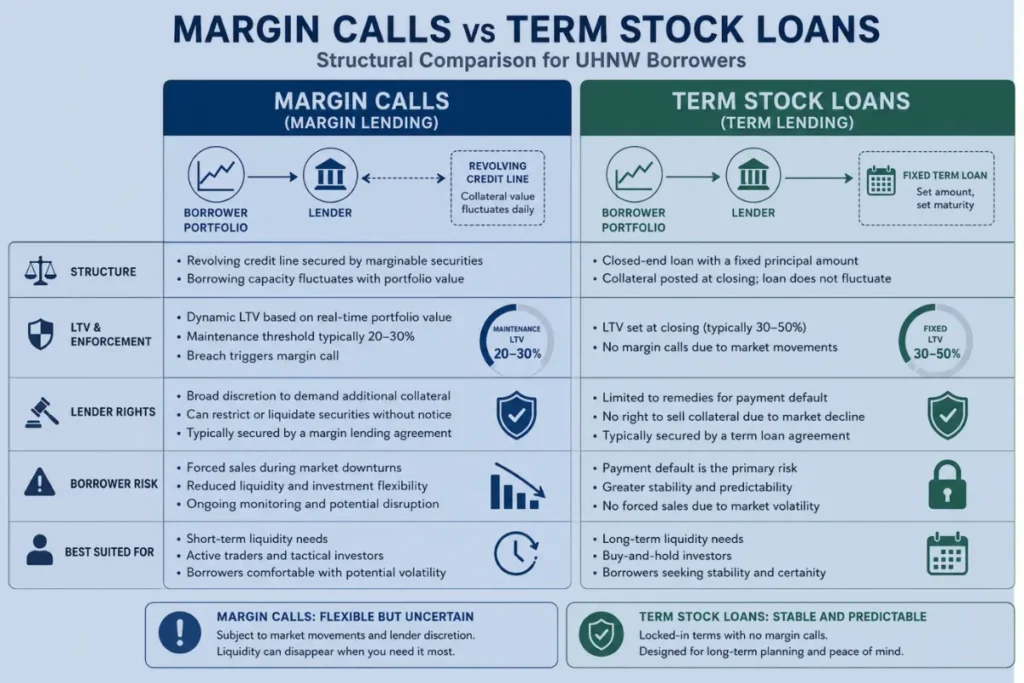

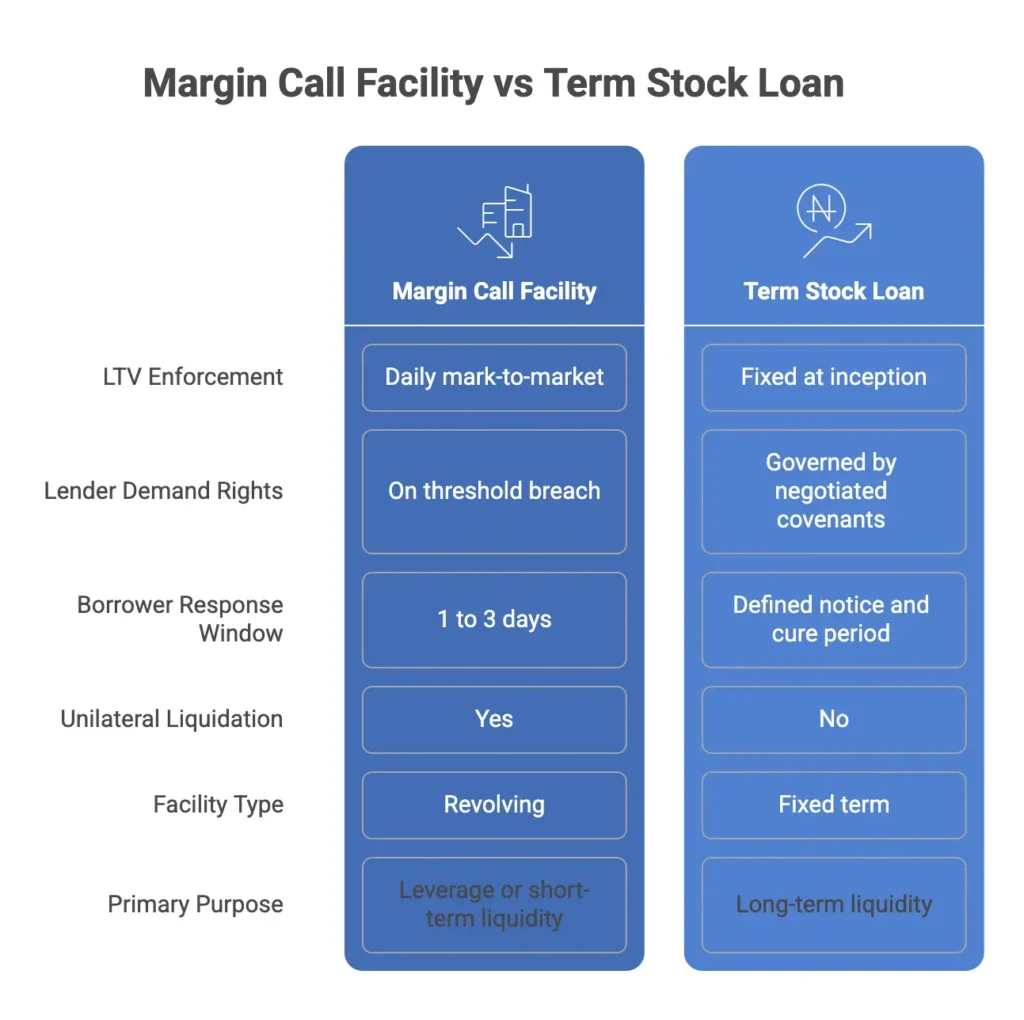

A margin lending facility is revolving and marked to market daily. The lender continuously monitors the ratio of the loan balance to the current market value of the pledged securities. If that ratio breaches a defined threshold, the borrower receives a margin call: a demand to restore the required equity level by depositing additional cash, pledging additional securities, or selling holdings to reduce the loan balance.

A term stock loan operates differently. The loan is issued for a fixed term, typically one to three years, against a single listed, free-trading stock at an agreed LTV set at inception. There is no daily mark-to-market mechanism. The borrower’s obligation is fixed at closing, and provided the agreed covenants are met, the lender cannot call for additional collateral or force a sale based on interim price movements.

The structural difference is not subtle. One format transfers meaningful market risk to the borrower in real time. The other isolates the borrower from that risk for the duration of the term, within the parameters of the agreed facility covenants. That is the margin call vs stock loan explained at a structural level.

How a Margin Call is Triggered

Margin calls occur when equity in a margin account falls below the maintenance margin requirement: the minimum threshold the lender requires the borrower to maintain. When the market value of the pledged securities declines, the loan-to-value ratio rises. Once it crosses the maintenance threshold, the margin call is issued.

The borrower typically has a short window, often one to three business days, to meet the margin call. Failure to do so allows the lender to liquidate securities in the account without the borrower’s consent, at whatever the current market price happens to be.

This mechanism is designed to protect the lender. In periods of market volatility, margin calls compound existing portfolio losses. A borrower who cannot meet a margin call is forced to crystallise losses at the worst possible time. The lender’s right to act unilaterally removes any ability to manage timing or execution.

The consequences extend beyond the immediate loss. Forced liquidation of a concentrated position, particularly in illiquid or thinly traded securities, can move the market against the borrower.

Understanding the margin call vs stock loan explained at this level of detail matters precisely because the consequences are not theoretical. For the background on why concentrated positions amplify this risk, see Stock Loans for Concentrated Shareholders.

A Stress Scenario: Margin Call vs Stock Loan Explained in Practice

Consider a founder holding a concentrated position in a single listed stock, pledged as collateral across two facilities: one a standard margin lending line, the other a three-year term stock loan. The stock drops 35% over six weeks following an earnings miss.

Under the margin facility, the maintenance margin threshold is breached in week two. The lender issues a margin call. The founder cannot meet it within the required window without liquidating other holdings at a loss. The lender executes a forced sale of pledged stock into a declining market, compounding the loss and reducing the position the founder had intended to retain long-term.

Under the term stock loan, the same 35% decline occurs. It is significant, but it does not automatically trigger enforcement action. The facility has defined covenant thresholds, negotiated at inception, with a notice and cure framework before the lender can act. The founder has time to respond, engage with the lender and consider options without facing unilateral liquidation.

The structural protection is not that losses are avoided. It is that the borrower retains enough time and agency to manage them. That is the margin call vs stock loan explained in practice, and it shapes how sophisticated borrowers approach facility selection before a decline happens, not after.

How a Term Stock Loan is Structured

A well-structured term stock loan addresses margin call risk through facility design. Several structural features distinguish it from a margin facility, and together they are what makes the margin call vs stock loan explained at a practical level.

LTV Set at Inception, Not Monitored Daily

The lender assesses the stocks at the outset and sets the advance rate based on that analysis. In most term facilities, this LTV is not continuously recalculated against daily market movements. Some facilities do include periodic review clauses or thresholds tied to significant collateral deterioration, and these should be confirmed at the term sheet stage. The LTV framework should be read in full before any facility is signed.

Defined Covenant Triggers, Not Open-Ended Demands

Term stock loans include covenant structures that specify the precise conditions under which the lender can act. These are negotiated at the outset and are not subject to unilateral adjustment during the facility term.

Liquidity, Not Leverage

Margin lending is frequently used to increase investment exposure, borrowing to buy more securities. A term stock loan is structured against a single listed stock for liquidity purposes. The borrower is not amplifying market risk through the borrowing itself.

Defined Enforcement Timelines

Even where a term stock loan includes provisions for accelerated repayment on covenant breach, the process is governed by the facility agreement and includes notice and cure periods. Immediate lender-executed liquidation is not a feature of a properly structured term facility.

How Private Credit Lenders Assess These Structures

Private credit providers assess term stock loan facilities differently from standard brokerage margin desks. The asset pledged is the primary criterion, and the baseline requirement is that the securities are free trading. Restricted stock, insider holdings subject to lock-up or shares with trading limitations attached will not be considered regardless of their market value.

Beyond that, a diversified basket of large-cap liquid securities is evaluated entirely differently from collateral that is concentrated or thinly traded. KYC at personal and corporate level satisfies the borrower requirement. The lender’s focus is on the quality, liquidity and enforceability of the pledged securities. See Private Credit Underwriting 2026 for a detailed breakdown.

Cross-collateralisation is worth raising where securities are held across multiple custodians. A broader security package can justify more favourable LTV terms and less restrictive covenants. That negotiation point does not exist in standard margin lending.

Covenant structure is a negotiated document, not a standardised schedule. A borrower who has the margin call vs stock loan explained at a structural level can approach that negotiation knowing precisely which protections matter and why. The BIS report on securities lending transactions and market structure provides useful institutional context on how these facilities are documented and enforced.

What Matters for Borrower Decision-Making

The choice between a margin lending facility and a term stock loan is a question of predictability and what happens when markets move against you. Having the margin call vs stock loan explained at a structural level is the starting point for making that decision correctly. Cost is secondary.

A margin facility offers flexibility and speed of access. It can be appropriate where the borrowing is short-term, the portfolio is highly diversified and liquid, and the borrower has the capacity to meet a margin call without disrupting their broader financial position. For borrowers using leverage as a tactical rather than strategic tool, this flexibility may outweigh the structural risk.

A term stock loan is the appropriate structure where certainty over the facility terms is required for a defined period, where the borrower holds a significant position in a single listed stock, where the purpose of the loan is long-term liquidity rather than short-term leverage, or where the borrower cannot absorb forced-sale risk.

For UHNW borrowers and family offices using securities-based lending as a liquidity tool rather than a leverage mechanism, the term stock loan structure is almost always the more appropriate format. The absence of a daily margin call mechanism is not a minor detail. It is the feature that preserves borrower agency throughout the facility term.

What to Confirm Before Choosing a Structure

Before committing to either structure, confirm the following with your lender or intermediary:

- Whether the facility includes a maintenance margin requirement and what specifically triggers a demand

- How quickly the lender can act following a threshold breach and whether a cure period is built in

- Whether the LTV is fixed at inception or subject to recalculation on a defined schedule or on demand

- What the lender’s rights are if a margin call is not met, including whether unilateral liquidation is permitted

- Whether the facility is documented as a term loan with fixed covenants or as a revolving facility subject to lender discretion

These questions belong at heads of terms, not at the point of signing. For the operational mechanics of how these facilities work before these questions arise, see How Do Securities-Backed Loans Work.

Conclusion

Having the margin call vs stock loan explained at a structural level is not an academic exercise. It determines how much of your position you retain if markets move against you, and whether the timing and execution of any enforcement action is yours to manage or the lender’s to execute unilaterally.

For borrowers who require certainty over the facility term and want to retain the ability to manage their portfolio through short-term price movements, the term stock loan structure is the relevant format to understand, negotiate and use. The structural features that eliminate the margin call mechanism are not a premium. They are the baseline for any serious liquidity facility built around a long-term portfolio.

If you are holding a significant listed position and considering borrowing against it, the terms of the facility will determine how much of that position you retain if markets move against you. We welcome a discreet conversation before you commit to a structure. Contact us today.

For a more structured breakdown of how these strategies are applied in practice, see the Securities-Based Lending Playbook.