How Lenders Use Loan-to-Value in Securities-Based Lending to Control Risk

Most borrowers negotiate a securities-based lending facility with one number in mind: the loan amount. Lenders structure the same transaction around a different number entirely, and unlike the loan amount, that number is not fixed at signing.

Loan-to-value in securities-based lending is the primary mechanism through which lenders manage collateral exposure across the life of an SBL facility. It determines how much can be borrowed, the conditions under which the lender can demand additional collateral, and the point at which enforcement becomes an option. Borrowers who treat LTV as a static ceiling, agreed once and then set aside, are routinely caught out when markets move.

If you are following the SBL Playbook sequence, the structural mechanics of how securities-backed loans are constructed are covered in How Securities-Backed Loans Work.

This post focuses specifically on how lenders use loan-to-value in securities-based lending as an active risk control tool, and what that means for borrowers structuring a facility. For a broader overview of how LTV operates across private credit and real estate structures, see Loan to Value Ratio in 2026.

How Lenders Set Loan-to-Value in Securities-Based Lending: Asset Class Comes First

Loan-to-value in securities-based lending is not calculated against a fixed valuation. The collateral is marked to market continuously, and the advance rate the lender applies reflects their assessment of how that collateral value might behave under stress.

The starting point is always the asset class. Before concentration, portfolio composition or borrower profile are considered, lenders assign an indicative advance rate based on the type of securities being pledged.

Current market ranges for 2026:

- Government bonds and investment-grade fixed income: 75% to 90%

- Blue-chip large-cap equities: 60% to 75%

- Diversified equity portfolios across multiple sectors: 55% to 70%

- Concentrated single-stock positions: 40% to 55%

- Volatile, illiquid or small-cap holdings: 30% to 45%

These figures are not uniform across all lenders. Private banks, private credit providers and specialist SBL lenders each apply their own underwriting criteria, and advance rates can vary meaningfully between institutions for the same collateral package. The ranges above represent the market as it currently operates across the UK, European and Asia-Pacific markets that Forbes Le Brock serves.

The underlying lender logic is consistent even where the specific numbers differ. Lenders are not lending against today’s portfolio value. They are lending against a stressed version of that value, one that accounts for the liquidity of the collateral, the speed at which they could enforce and realise it, and the market conditions they might face if they needed to do so.

Asset Concentration Risk vs Loan-to-Value in Securities-Based Lending

For UHNW borrowers and family offices, the most common friction point in LTV negotiations is concentration. A portfolio built around a single legacy shareholding, often the very asset generating the liquidity need in the first place, attracts the most conservative advance rates in the market.

The reason is execution risk at enforcement. A lender holding security over a diversified portfolio of liquid equities can realise collateral incrementally across multiple positions without moving the market. A lender holding security over a single large-cap position faces a different problem entirely. Liquidating a concentrated block creates price impact, and that price impact directly erodes the recovery value the lender is relying on.

Lenders manage this in two ways. First, they apply a haircut to the advance rate relative to what they would offer on a diversified portfolio of equivalent market value. A borrower who might attract a 65% advance rate on a mixed portfolio may find the same portfolio, reweighted toward a single stock, advances at 45% or below.

Second, lenders impose concentration limits within the collateral pool. Typically, no single security is permitted to represent more than 20% to 30% of the total collateral value at any point during the facility. If market movements push a single position above that threshold, the borrower may be required to introduce additional securities or accept a reduction in the available facility.

Borrowers who understand this dynamic before approaching lenders can structure their collateral package more effectively. Introducing additional securities alongside a concentrated position, even where those securities generate a lower return, can materially improve the opening advance rate and reduce concentration-related restrictions throughout the life of the facility. For broader context on how lenders approach facility structure and risk, see Securities-Based Lending 2026: Structure and Risk.

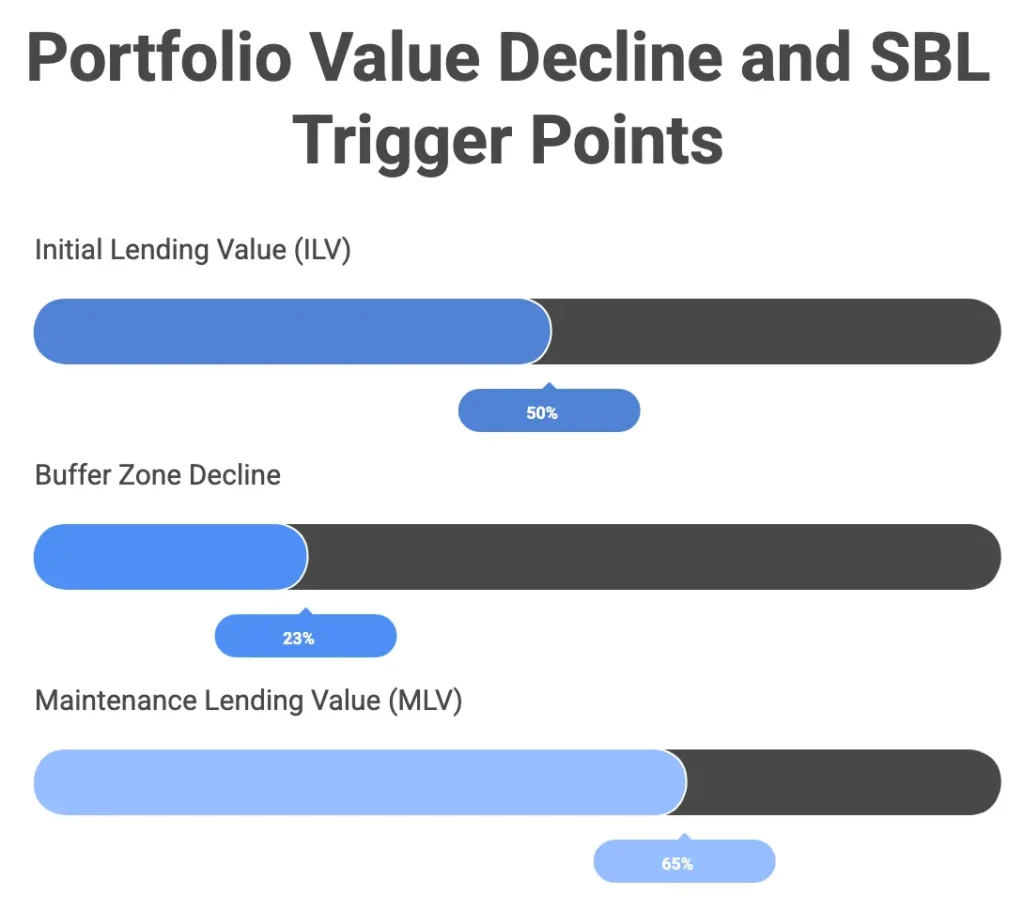

ILV and MLV: The Two Numbers That Actually Control the Facility

This is the structural detail that generates the most borrower problems in practice, and it is rarely explained with sufficient clarity at origination.

SBL lenders typically operate with two distinct loan-to-value in securities-based lending thresholds, not one.

Initial Lending Value

The Initial Lending Value is the advance rate applied at drawdown. It is the number borrowers negotiate, the figure that determines the opening loan amount, and the threshold that appears most prominently in term sheet discussions. Most borrowers treat this as the operative loan-to-value for the life of the facility. It is not.

Maintenance Lending Value

The Maintenance Lending Value is a lower threshold set below the ILV, which the borrower must maintain throughout the facility term. If the market value of the pledged securities falls and the outstanding loan as a proportion of collateral value rises above the MLV threshold, the lender is entitled to issue a collateral top-up notice.

The gap between ILV and MLV is the lender’s operational buffer. It gives them time to respond to market movements before their position becomes impaired. J.P. Morgan Private Bank describes this distinction explicitly in their SBL facility documentation, noting that maintenance lending values are set at the lender’s discretion up to regulatory thresholds and can be revised without prior notice to the borrower.

To illustrate the mechanics with concrete numbers:

- Portfolio value at origination: £10,000,000

- ILV: 50%, facility advanced: £5,000,000

- MLV: 65% of outstanding loan to collateral value

- MLV breach point: collateral falls below £7,692,308 (£5,000,000 ÷ 0.65)

The portfolio starts at £10,000,000. The MLV breach occurs when collateral declines to approximately £7.69 million, representing a 23% fall from origination value. That is the buffer the borrower is actually working with.

A 23% decline in a diversified equity portfolio is not a stress scenario. It is a normal market correction. In a concentrated single-stock position, that level of decline can occur within weeks.

When the portfolio crosses the £7.69 million threshold, the lender issues a top-up notice. The borrower has two to five business days to introduce additional collateral or reduce the outstanding balance. There is no grace period built into the mechanics. The trigger is contractual and automatic.

The gap between the ILV of 50% and the MLV of 65% is not generous headroom. It is a precisely calibrated buffer designed to give the lender an early enforcement trigger before their position becomes materially impaired.

How Lenders Adjust Loan-to-Value in Securities-Based Lending Facilities

The advance rate negotiated at origination is not necessarily the one that applies six months later. Lenders reserve the right to revise lending values in response to sustained market volatility, deterioration in the liquidity of specific pledged securities, or changes in their internal capital treatment of the facility.

This is not a theoretical risk. It happens, and it typically happens during periods of market stress, precisely when borrowers are least able to respond. Reviewing facility documentation for unilateral adjustment language before signing is not optional. It is a basic structuring discipline.

Lenders build these adjustment rights directly into facility documentation. They sit within standard collateral policy clauses and are reviewed by internal risk committees, not negotiated case by case. Borrowers who do not identify and challenge this language at term sheet stage will find it embedded in the executed agreement with no practical remedy.

A Real-World Scenario: Concentration Risk and the MLV Trap

A European family office holds a £15 million position in a single listed technology company, accumulated over more than a decade. They approach a private bank seeking £7 million in liquidity to fund a property acquisition, structuring the transaction as a securities-based loan against the shareholding to avoid triggering a capital gains event on a position with a very low cost base.

The lender assesses the collateral. The stock is large-cap and liquid in normal market conditions, but the proposed collateral pool is 100% concentrated in a single name. The lender applies a concentration haircut, setting the ILV at 48% rather than the 65% they would offer against a diversified portfolio. The facility is advanced at £7,200,000 against a collateral value of £15,000,000. The MLV is set at 38%.

Three months after completion, the technology sector sells off sharply in response to a shift in interest rate expectations. The stock declines 25%. Portfolio value falls to £11,250,000. The outstanding loan of £7,200,000 now represents 64% of collateral value, well above both the ILV and the MLV floor of 38%. The lender issues a formal collateral top-up notice requiring the family office to introduce additional unencumbered assets or repay £2,800,000 within five business days.

The property acquisition has already been completed. The loan proceeds have been deployed. The family office is now forced to liquidate part of the shareholding at a 25% discount to the price at which the facility was structured, crystallising exactly the capital gain they designed the transaction to defer.

The error was not the choice of instrument. Securities-based lending was the right structure for this situation. The error was the failure to model the MLV scenario at origination and either introduce diversifying collateral to reduce the concentration haircut, or size the facility more conservatively relative to the MLV floor to create adequate headroom.

For context on how lenders approach LTV in broader private credit structures, the Loan to Value Ratio in 2026 post in the Borrower Trust and Due Diligence Playbook covers the same concept across different asset classes and lending contexts.

What to Negotiate Before the Facility Agreement is Signed

Borrowers who understand how lenders use loan-to-value in securities-based lending as a control mechanism have a genuine basis for negotiation at origination. The following points warrant specific attention before any facility agreement is executed:

- MLV threshold and gap to ILV: Model what portfolio decline triggers a top-up notice and size the facility accordingly, not just against the opening advance rate.

- Top-up notice periods: Standard agreements require a response within two to five business days. For less liquid collateral, negotiate longer.

- Substitution rights: The right to swap securities within the pledged pool without lender consent gives flexibility to manage concentration risk during the facility.

- Concentration limits: If the facility is backed by a single-stock position, understand precisely how the lender treats that under stress before agreeing terms.

- Unilateral LTV adjustment: Identify any language permitting the lender to revise advance rates without consent and negotiate notice periods and cure rights at term sheet stage.

- Interest rate structure: Lower loan-to-value in securities-based lending attracts better pricing. Diversified, high-quality collateral and a conservative advance rate often deliver materially lower rates across the life of the facility.

Conclusion

Loan-to-value in securities-based lending is not a pricing mechanism. It is lender control architecture designed to protect the lender before a problem develops, not after one occurs.

The borrowers who receive top-up notices under pressure are not unlucky. They are under-prepared. Sophisticated structuring happens at origination, not during a market sell-off.

If you are assessing a securities-based lending facility and want to understand how loan-to-value thresholds will affect your borrowing capacity and downside exposure, we welcome a Discreet Conversation

For a more structured breakdown of how these strategies are applied in practice, see the Securities-Based Lending Playbook