NAV Lending: Unlocking Liquidity in Private Equity in 2025 and Beyond

The landscape of private equity is constantly evolving. For years, the focus has been on deploying capital, nurturing portfolio companies, and orchestrating successful exits. However, in recent times, a significant challenge has emerged: liquidity. Exit timelines have stretched, initial public offerings (IPOs) have become less predictable, and distributions to investors have slowed. Simultaneously, traditional credit facilities have tightened, making capital less readily available through conventional means.

In this environment, both private equity fund managers and their investors, including sophisticated limited partners (LPs), family offices, and HNWIs, are seeking innovative ways to access capital without disrupting their core investment strategies.

They need liquidity without being forced into premature or suboptimal portfolio company sales. This is where NAV lending has emerged as a powerful, strategic solution.

But NAV lending isn’t just a short-term liquidity fix, it’s becoming a critical enabler of asset reallocation. By unlocking capital from within portfolio companies, private equity holders can tactically adjust exposures, shift capital across strategies, and respond to changing market conditions without being forced to exit core positions. This opens the door to more agile, efficient portfolio rebalancing at both the GP and LP levels.

Often discussed in hushed tones within the upper echelons of private markets, NAV lending is quietly transforming how private equity holders can use portfolio rebalancing to manage their capital needs and rebalance their portfolios.

NAV Lending – What Exactly is it?

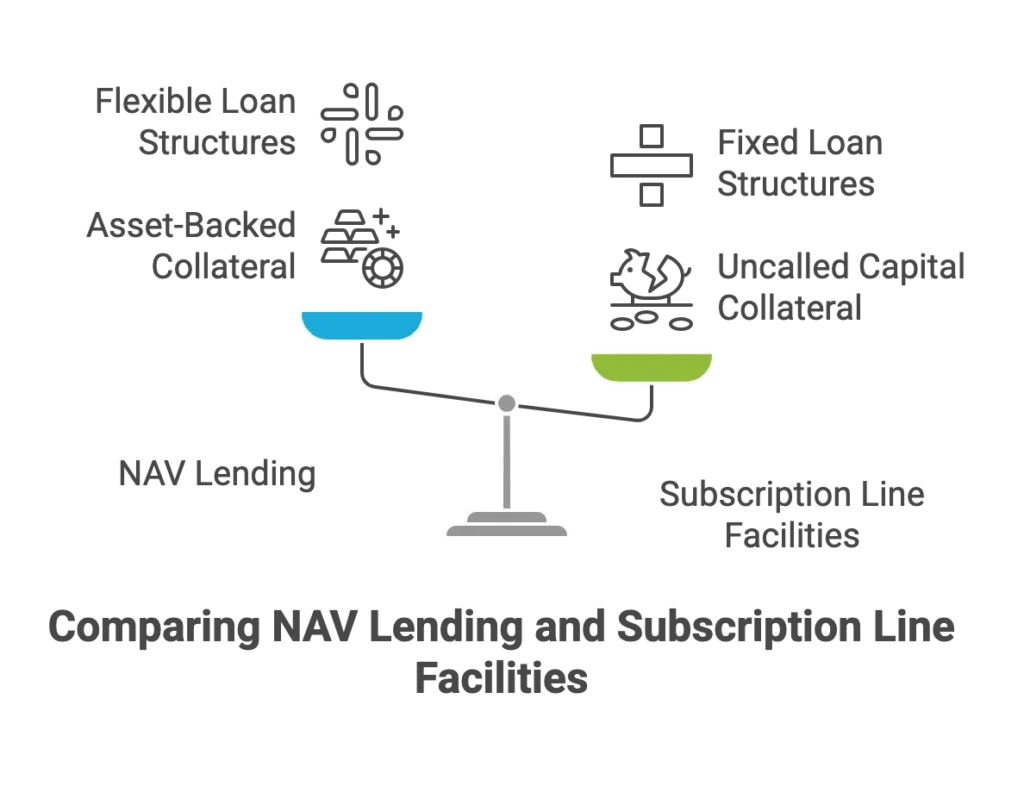

At its core, NAV lending is a form of financing where a lender provides a credit facility or loan secured by the Net Asset Value (NAV) of a private equity fund or a specific portfolio of private equity investment interests. Unlike traditional subscription line facilities, which are secured by the uncalled capital commitments of LPs, NAV financing uses the value of the underlying portfolio assets or funds as collateral.

Think of it as borrowing against the value that has already been created within the fund’s holdings – the value of the fund’s holdings in its portfolio companies. The borrower is typically the private equity fund itself, a holding vehicle, or sometimes a large investor or family office holding significant LP interests or GP stakes.

The structure of NAV-based financing can vary significantly. It can be:

- Recourse or Non-Recourse: Depending on the structure, the lender may have recourse only to the pledged assets or funds (secured NAV) or potentially to other assets of the borrower.

- Senior or Mezzanine: The NAV loan can sit senior in the capital structure or as a junior/mezzanine layer.

- Term or Revolving: It can be a single lump-sum loan for a fixed term or a flexible revolving credit facility that can be drawn and repaid as needed.

This flexibility means that NAV lenders can tailor solutions to the specific needs and risk management profile of the private equity fund or investor.

The Strategic Advantage: Why NAV Lending Matters Now

The appeal of NAV lending lies in its unique ability to provide liquidity without requiring the sale of underlying assets. In a market where exit windows are narrow and valuations may be depressed, avoiding a forced sale is paramount for preserving IRR and maximising returns for limited partners.

Here’s why NAV lending is gaining significant traction among sophisticated private equity managers and investors:

- Liquidity Without Liquidation: This is the primary benefit. Funds can access capital for various purposes – from funding follow-on investment in portfolio companies to making distributions to LPs or meeting capital commitments in other funds – all without selling assets prematurely. This is particularly valuable when portfolio companies are not yet ripe for exit or market conditions are unfavourable for sales.

- Preserving IRR: By avoiding early, potentially discounted asset sales, NAV lending allows funds to hold assets until optimal exit timing and valuation are achieved. This directly contributes to preserving and potentially enhancing the fund’s IRR.

- Flexibility and Optionality: NAV facilities provide greater flexibility in capital management. A fund manager can use the facility to bridge timing gaps between capital calls and distributions, manage working capital needs at the fund level, or seize new investment opportunities quickly.

- Tailored Solutions: Unlike more commoditised financing, NAV lending is highly structured and can be customised based on the specific characteristics of the underlying portfolio – its diversification, sector exposure, vintage, and expected cash flows. This bespoke nature appeals to sophisticated borrowers.

- Alternative to Equity: For a private equity fund or investor needing capital, NAV financing as an alternative to raising additional equity at the fund level or selling LP interests at a discount on the secondary market can be significantly more attractive, preserving ownership and future upside.

In essence, NAV lending serves as a powerful tool for private equity funds and investors to manage their balance sheet strategically, providing access to capital when and where it’s needed most.

Real-World Applications: Use Cases of NAV Lending

The versatility of NAV lending is best illustrated through practical examples of how different market participants are deploying these credit facilities:

- The Family Office Managing Diverse Commitments: A large family office has a significant, diversified portfolio of LP interests across various private equity funds. They need to meet a large, unexpected capital commitment in a new, highly attractive fund. Rather than selling a portion of their existing, illiquid LP interests on the secondary market at a potential discount to NAV, or liquidating public market holdings, they secure a NAV loan against a select portion of their well-performing private equity portfolio. This provides the necessary liquidity quickly, allowing them to meet the new commitment without disrupting their long-term private equity investing strategy or incurring transaction costs and potential value leakage from a secondary sale.

- The PE Fund Supporting Portfolio Company Growth: A private equity fund holds a successful portfolio company that requires additional capital for a strategic bolt-on acquisition. The fund has limited remaining uncalled capital commitments and doesn’t want to dilute its ownership by bringing in new equity investors at the portfolio company level. The fund manager secures a NAV-based financing facility against the Net Asset Value of a diversified pool of its other portfolio companies. This allows the fund to inject the necessary capital into the target company, facilitating growth and enhancing the value of the overall portfolio investment, all while preserving the fund’s equity stake.

- The Secondaries Fund Managing Liquidity: A secondaries fund acquires LP interests from investors seeking liquidity. These acquisitions require significant upfront capital. While waiting for distributions from the acquired interests, the fund needs working capital or wishes to make further acquisitions. A NAV facility, secured by the asset value of the fund’s holdings (the acquired LP interests), provides a flexible source of borrowing. This helps the fund manage its cash flow, bridge the gap between capital deployment and distributions, and potentially increase its deployment capacity.

These scenarios highlight how NAV lending allows sophisticated players to access capital efficiently, supporting strategic objectives across different levels of the private equity landscape.

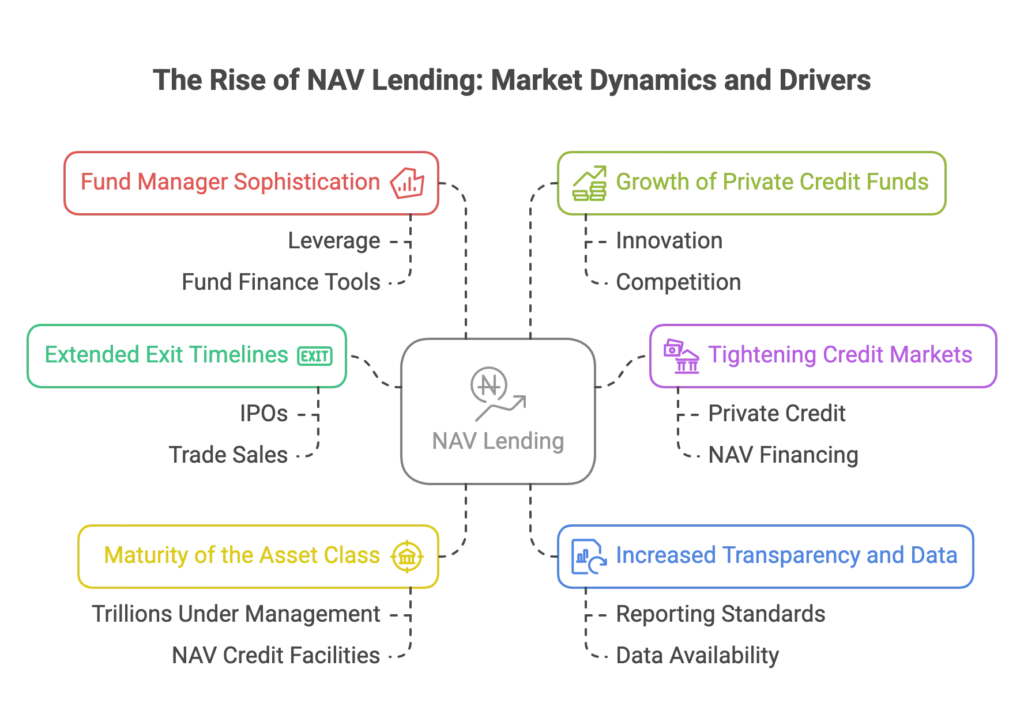

The Rise of NAV Lending: Why Now?

The growth of NAV lending is not accidental; it’s a direct response to prevailing market conditions and structural shifts in private markets.

- Extended Exit Timelines: As mentioned, the traditional path to liquidity via IPOs or trade sales has become less predictable and often takes longer. This creates a need for alternative liquidity sources at the fund level.

- Tightening Credit Markets: While private credit has grown significantly, the broader environment for traditional bank financing has become more cautious. NAV financing offers a specialised form of private credit tailored to the nuances of private equity assets.

- Maturity of the Asset Class: Private equity is no longer a niche asset class. With trillions under management, the need for sophisticated financial tools like NAV credit facilities is increasing. Lenders have also become more comfortable underwriting the risks associated with diversified private equity portfolios.

- Increased Transparency and Data: Improved reporting standards and data availability regarding private equity portfolio performance and Net Asset Value calculations have made it easier for lenders to underwrite NAV loans.

- Fund Manager Sophistication: Private equity managers are increasingly sophisticated in their use of leverage and fund finance tools. They view NAV facilities not just as a last resort but as a strategic component of their capital structure.

- Growth of Private Credit Funds: The proliferation of private credit funds actively seeking opportunities has increased the supply of capital available for NAV lending, driving innovation and competition in the market for NAV facilities.

This confluence of factors has propelled NAV lending from a niche product to a significant segment of the fund finance market, with estimates suggesting the market could exceed 100 billion USD in the coming years.

Key Considerations for Implementing a NAV Facility

While NAV lending offers compelling advantages, it is a complex form of financing that requires careful consideration by both borrowers and lenders.

Sophisticated investors and fund managers must evaluate several key factors:

- Valuation Discipline: The credibility and consistency of the Net Asset Value calculation are paramount. Lenders will scrutinise the valuation methodologies for the underlying portfolio companies. Independent third-party valuations may be required. Market volatility can impact the NAV, potentially affecting the facility’s terms or triggering covenants.

- Advance Rates (LTV Ratio): The amount a lender will provide relative to the NAV (the Loan-to-Value or LTV ratio) is typically conservative, ranging from 20% to 50%, depending heavily on the diversification, quality, and perceived liquidity of the underlying assets. Highly concentrated or early-stage portfolios will command lower advance rates.

- Covenants and Monitoring: NAV facilities come with covenants designed to protect the lender. These often include minimum NAV thresholds, maximum leverage ratios, reporting obligations, and restrictions on portfolio composition or distributions. Breaching a covenant can have significant consequences. Robust internal systems for monitoring portfolio performance and compliance are essential.

- Counterparty Strength and Expertise: Choosing the right NAV lender is critical. They must possess deep expertise in private equity, understand the nuances of valuing illiquid assets, and have the capacity and willingness to work through complex structures. Experience with cross-jurisdictional deals is often necessary.

- Legal Structuring and Collateral: The legal framework for a NAV loan can be intricate. It typically involves granting the lender a security interest in the pledged assets or funds. This might be a direct security interest in the LP interests themselves, an interest in a holding vehicle that owns the interests, or security over the fund’s rights to receive distributions from specific portfolio investments. This differs significantly from the simpler pledge of capital commitments in a traditional subscription line. Understanding the implications of pledging specific investments as collateral is vital.

- Cost of Capital: While potentially more attractive than a distressed asset sale, NAV financing is a form of structured private credit and may carry higher interest rates and fees compared to traditional bank financing, reflecting the complexity and illiquid nature of the collateral. The all-in cost must be weighed against the benefits of maintaining liquidity and preserving IRR.

- Risk Management: Both borrowers and lenders must have robust risk management frameworks. For the borrower, this includes stress-testing the facility against potential drops in NAV or changes in market conditions. For the lender, it involves sophisticated underwriting and ongoing monitoring of the underlying portfolio.

Navigating these considerations requires expert guidance and a thorough understanding of the specific private equity portfolio and the borrower’s strategic objectives.

NAV Lending vs. Other Fund Finance Tools

It’s important to position NAV lending within the broader context of fund finance. While subscription lines have been the staple for managing short-term liquidity and bridging capital calls, NAV facilities serve a different purpose. Subscription lines are based on the creditworthiness of the LPs and their remaining capital commitments. NAV lending is based on the value and quality of the assets already acquired by the fund.

They are often complementary. A fund might use a subscription line early in its life for efficient capital deployment and then transition to a NAV facility later to manage liquidity related to the existing portfolio or make distributions while waiting for optimal exit timing.

Selling LP interests at a discount on the private equity secondary market is another way to generate liquidity, but it typically involves giving up future upside on the sold assets. NAV lending allows the borrower to retain ownership of the underlying portfolio and benefit from future appreciation, albeit with the cost and obligations of the loan.

The Future of NAV Lending

The market for NAV lending is still maturing but is on a clear upward trajectory. As private equity continues its continued growth and becomes an even more central component of institutional and HNW investor portfolios, the need for sophisticated liquidity management tools will only increase.

NAV lending is expected to become a standard component of the private equity landscape, integrated into fund structuring and capital management strategies from inception. The market continues to innovate, with new lenders entering the space and existing players developing more complex and flexible products. This includes facilities secured by specific asset classes within a diversified portfolio, or structures designed for specific types of borrowers like family offices or sovereign wealth funds.

2026 Update: How NAV Lending Is Evolving in a Higher-Rate, Lower-Liquidity Market

The role of NAV facilities has expanded significantly heading into 2026. Several structural shifts are driving renewed demand:

• Slower realisations: Distributions remain muted across private equity as exit timelines extend and sponsors delay sales in the hope of improved pricing. This places pressure on GPs and LPs who still need liquidity for commitments, co-investments, and balance-sheet allocation.

• Higher refinancing costs: With traditional credit still priced tightly, more funds are using NAV lines to refinance legacy fund-level obligations or fund follow-on rounds without selling assets at compressed multiples.

• Increased lender comfort: Private credit funds have deepened their underwriting frameworks for diversified PE portfolios. Advance rates remain conservative, but lenders are now structuring more hybrid facilities that blend senior and mezzanine characteristics.

• LPs using NAV lines directly: Large LPs, including family offices and sovereign investors, are increasingly using NAV financing to rebalance exposures, meet commitment schedules, and manage liquidity across vintage years without selling on the secondary market.

These dynamics reinforce the reality:

NAV lending is no longer an emergency tool, it is becoming a standard component of long-term liquidity planning for sophisticated private equity participants.

Conclusion: The Next Evolution in PE Liquidity Strategy

In an era defined by extended hold periods and the strategic imperative to maximise value, NAV lending is far more than just a temporary bridge. It is a sophisticated financial instrument that empowers private equity funds and investors to proactively manage their liquidity, optimise capital structures, and enhance overall portfolio performance.

By providing access to capital against the inherent value of illiquid private equity holdings, NAV financing offers a powerful alternative to traditional methods of generating cash. It enables fund managers to make strategic decisions based on market opportunity and asset readiness, rather than being dictated by immediate liquidity needs.

For high-level decision-makers, investors, and HNWIs navigating the complexities of private markets, understanding and potentially leveraging NAV lending is becoming essential. It’s not just about securing financing; it’s about unlocking optionality, preserving control, and strategically positioning your private equity portfolio for long-term success. The rise of NAV lending signifies a fundamental shift in how liquidity is perceived and managed within the private equity landscape.

Interested in Exploring NAV-Based Finance for your Fund or Portfolio?

Forbes Le Brock provides discreet access to structured NAV lending facilities through a global network of credit partners.

→ Schedule a confidential consultation to discuss bespoke solutions aligned with your liquidity needs and investment strategy.

🔥 Got questions about NAV Lending? Listen to this Deep Dive for insights and key takeaways. 🎙️ Tune in now!