Structured Finance: Unlocking Value in Commercial Real Estate

Structured finance has become a critical tool in commercial real estate, offering investors, lenders, and developers flexible ways to manage risk, access liquidity, and unlock capital. As markets evolve, innovative financing structures are helping to close gaps that traditional debt or equity cannot.

Why Structured Finance Matters in Today’s Market

The commercial real estate (CRE) landscape has changed dramatically. Rising interest rates, stricter regulatory oversight, and more conservative credit committees have limited the availability of traditional bank lending.

For developers, investors, and family offices, this creates a major challenge. Many high-value projects remain stalled, not for lack of vision or viability, but because conventional financing no longer fits their complex capital requirements or risk profiles.

Structured finance fills this gap. It provides a dynamic, flexible source of capital that adapts to project needs, manages risk with precision, and connects borrowers to deep, diversified pools of global capital. Increasingly, structured finance is not simply an alternative but a strategic imperative for ambitious commercial real estate players.

What Is Structured Finance?

At its core, structured finance refers to highly customised, non-standard financing solutions designed for complex projects or portfolios.

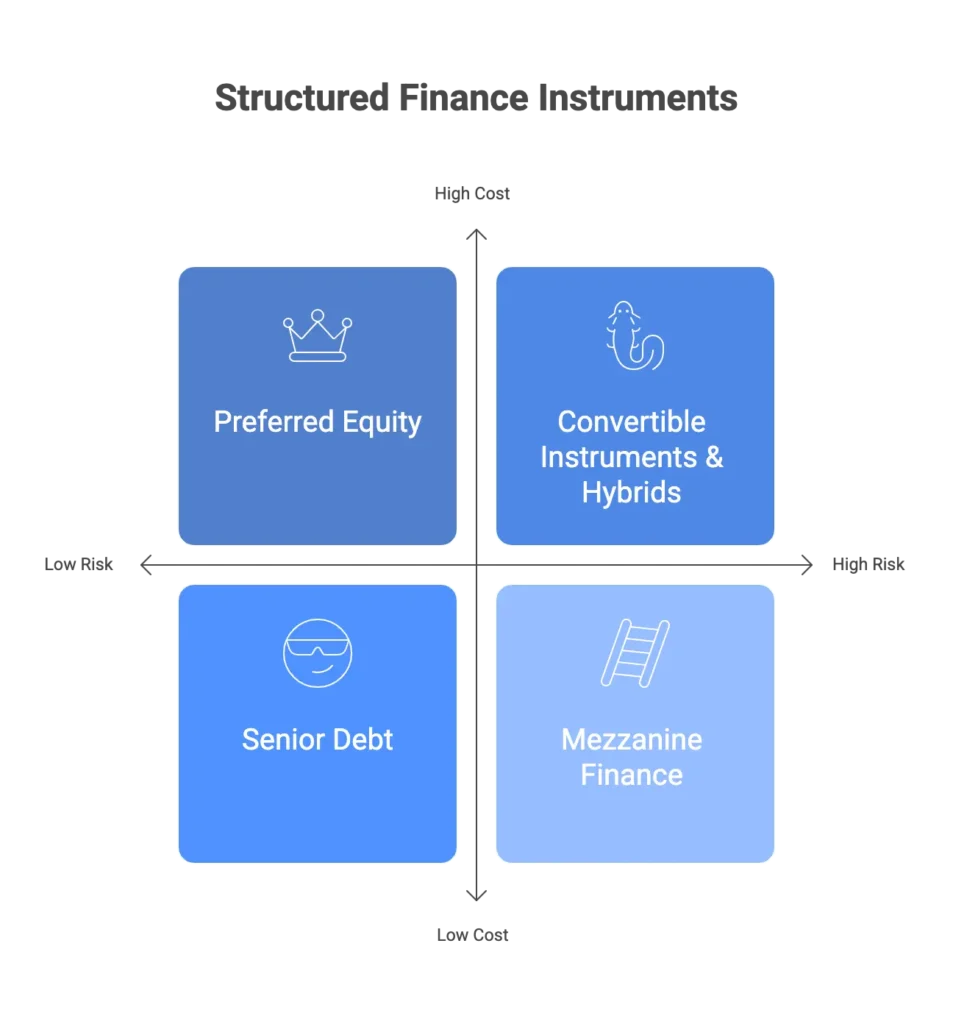

Unlike a standard mortgage, which offers a uniform structure, structured finance involves layering multiple instruments into a bespoke capital stack. This might include:

- Senior Debt – Lowest cost, lowest risk, priority in repayment.

- Mezzanine Finance – Subordinated debt that fills the gap between senior loans and equity.

- Preferred Equity – Equity-like capital that sits above common equity but below debt.

- Convertible Instruments & Hybrids – Capital that can shift between debt and equity depending on conditions.

This combination creates a funding solution designed to match the cash flow profile, risk appetite, and strategic goals of the borrower.

A useful analogy: structured finance is the Savile Row bespoke suit of financing, meticulously tailored to fit the unique contours of a project, rather than the “off-the-peg” one-size-fits-all model of traditional bank lending.

The Strategic Benefits of Structured Finance

1. Flexibility and Customisation

Structured finance adapts to the project lifecycle and borrower’s objectives. For example:

- Repayments can be deferred until stabilisation or sale.

- Covenantscan be negotiated to reflect the operational realities of development or repositioning.

- Hybrid solutions allow instruments to behave like debt in some circumstances and equity in others, optimising risk–return alignment.

This flexibility can be the difference between a stalled project and one that delivers outsized returns.

2. Advanced Risk Allocation

Perhaps the most powerful advantage of structured finance is its ability to allocate risk surgically. Through tranching, capital is structured into layers:

- Senior tranches: Lowest risk, lower yields, suited to insurers and pension funds.

- Mezzanine tranches: Medium risk and return, attracting specialist credit funds.

- Equity/first-loss positions: Highest risk, highest potential return, appealing to hedge funds and opportunistic private equity.

Each tranche is matched with an investor that actively chooses that risk level, ensuring alignment between borrower needs and investor appetite.

3. Access to Diverse Capital Pools

Structured finance opens the door to capital sources beyond banks. The global private credit market has expanded to over $1.6 trillion (Preqin, 2024) and continues to grow as institutional investors seek yield outside of public markets.

Typical providers include:

- Asset managers with dedicated credit strategies

- Pension funds and insurers searching for long-duration, stable returns

- Specialist credit funds focused on mezzanine or distressed opportunities

- Family offices and UHNWIs seeking direct exposure to real assets

This diversification not only improves execution certainty but often results in faster decision-making than bank credit committees.

How Structured Finance Works: Securitisation in Practice

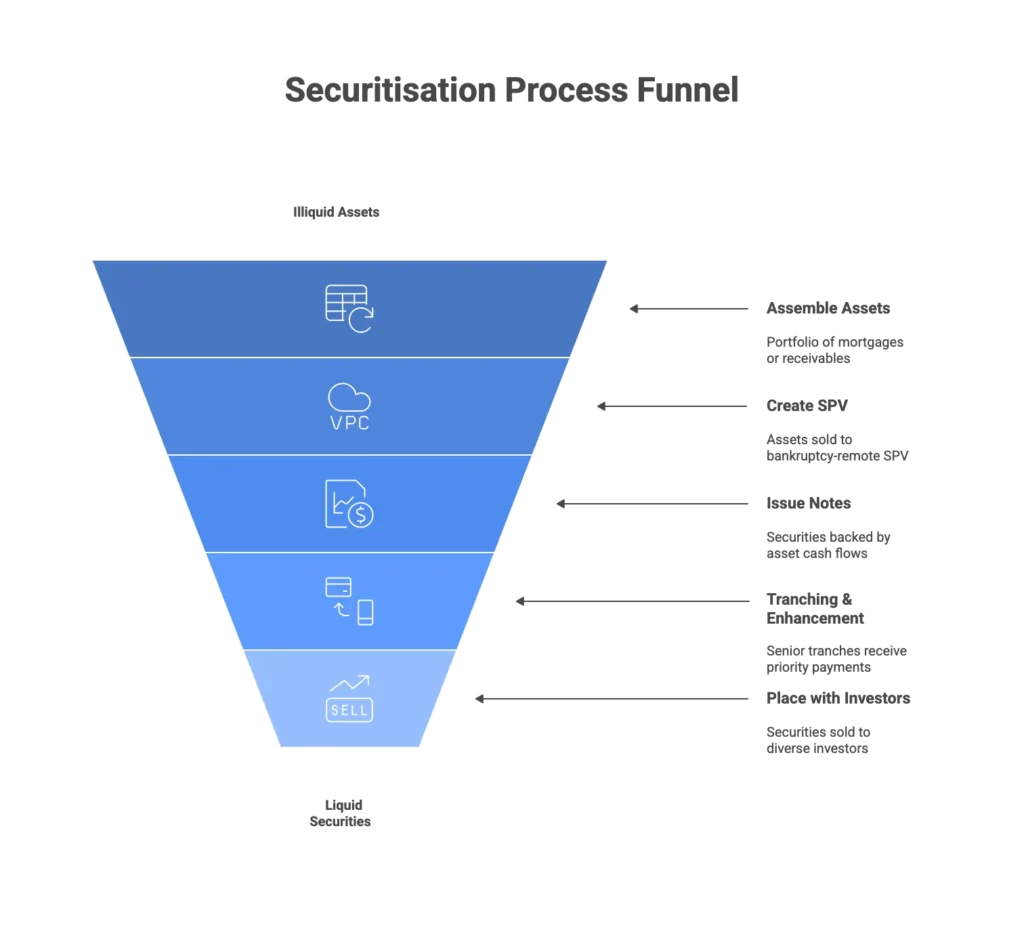

A key mechanism underpinning structured finance is securitisation, the process of transforming illiquid assets (such as loans or receivables) into tradable securities.

The Process:

- Originator Assembles Assets – e.g., a portfolio of commercial mortgages or rental receivables.

- Creation of an SPV – Assets are sold to a bankruptcy-remote Special Purpose Vehicle (SPV), ring fencing them from the originator’s balance sheet.

- Issuance of Notes – The SPV issues securities backed by asset cash flows.

- Tranching & Credit Enhancement – Senior tranches receive priority payments, with junior tranches absorbing losses. Credit ratings, overcollateralisation, or reserve accounts further support investor confidence.

- Placement with Investors – Securities are sold to investors across the risk spectrum, from conservative insurers to opportunistic funds.

This structure provides liquidity, redistributes risk, and connects real estate projects to global institutional capital.

Structured Finance in Action: Three Scenarios

1. Urban Regeneration

A developer secures bank funding for Phase 1 of a mixed-use scheme. The lender refuses to extend financing for Phase 2 until stabilisation. A mezzanine tranche fills the gap, enabling work to continue immediately, shortening the development timeline and improving project IR

2. Family Office Refinancing

A family office with a diversified CRE portfolio seeks liquidity without selling core holdings. By placing assets into a private securitisation, it issues senior bonds to insurers and retains junior tranches. This raises cost-effective capital while preserving ownership and future upside.

3. Opportunistic Acquisition

An investor acquires an underperforming retail park requiring refurbishment. Banks decline to lend due to weak current cash flows. A structured deal combines a low-leverage senior loan with preferred equity, funding repositioning. Preferred equity investors are rewarded with a larger share of profits post-stabilisation.

Key Considerations and Risks

While the benefits are compelling, structured finance is complex and must be approached prudently.

- Complexity – Documentation, modelling, and structuring are far more involved than plain vanilla loans.

- Transaction Costs – Legal, advisory, and rating fees can be significant.

- Cost of Capital – Junior tranches and preferred equity are expensive. Borrowers must calculate blended cost of capital carefully.

- Liquidity Risk – In volatile markets, certain structured products may be less liquid, making refinancing more difficult.

- Investor Alignment – Misalignment between senior and junior investors can create friction in distressed scenarios.

- Market Timing – Rising rates or shifting investor sentiment can quickly alter pricing and appetite.

- Advisory Requirement – Engaging an experienced structured finance team or intermediary is critical to protect borrower interests while meeting investor demands.

Future Outlook: The Evolution of Structured Finance

Structured finance in CRE is evolving rapidly, shaped by new market forces:

- Growth of Private Credit – As banks retreat, private lenders continue to expand their dominance in bespoke capital solutions.

- ESG-Linked Structures – Green securitisation and sustainability-linked tranches are emerging as investors demand alignment with environmental goals.

- Digitalisation and Tokenisation– Blockchain technology may transform securitisation, improving transparency and secondary market liquidity.

- Cross-Border Capital Flows– Global investors are increasingly using structured products to access real estate in new markets, especially Asia-Pacific and Europe.

These trends suggest structured finance will become even more integral to commercial real estate finance strategy.

Conclusion

In today’s market, reliance on traditional financing is no longer sufficient. Structured finance is essential, offering flexible, tailored capital solutions, precise risk allocation, and access to vast pools of private credit.

For developers, UHNWIs, and family offices, structured finance turns capital from a transactional necessity into a strategic tool for growth, resilience, and value creation.

Call to Action

Forbes Le Brock works with property developers, UHNWIs and family office to arrange discreet, tailored structured finance solutions across global markets. Contact us in confidence for a strategic consultation