Lombard Loan Case Studies: Structure Determines the Outcome

Three Lombard loan case studies, that were facilitated in the past year were structured after a standard private bank proposal failed to meet the execution requirement. In each case, the client had been with the bank for years. The portfolios were well-managed. The issue was the bank’s underwriting framework, not the quality of the assets.

These Lombard loan case studies examine three execution scenarios: a time-sensitive PE co-investment, a competitive property bridge, and a tax-constrained family liquidity requirement. They are not presented as templates. They are decision-making accounts that show where standard bank lending reaches its limits and how specialist structuring closes the gap. For a full breakdown of how Lombard facilities are structured, see the Lombard Loan Guide 2025

How Lender Frameworks Shape Execution Outcomes

Standard private bank Lombard facilities are built around a defined eligible collateral list and standardised advance rates. For straightforward, diversified portfolios, this works. For portfolios with concentration, cross-border custody, managed fund exposure, or time-sensitive drawdown requirements, it frequently does not.

The structural principles that govern Lombard lending are covered in the Securities-Based Lending 2026 guide. What these case studies add is the execution layer: how individual variables within a specific portfolio determine whether a facility is deliverable, and at what terms.

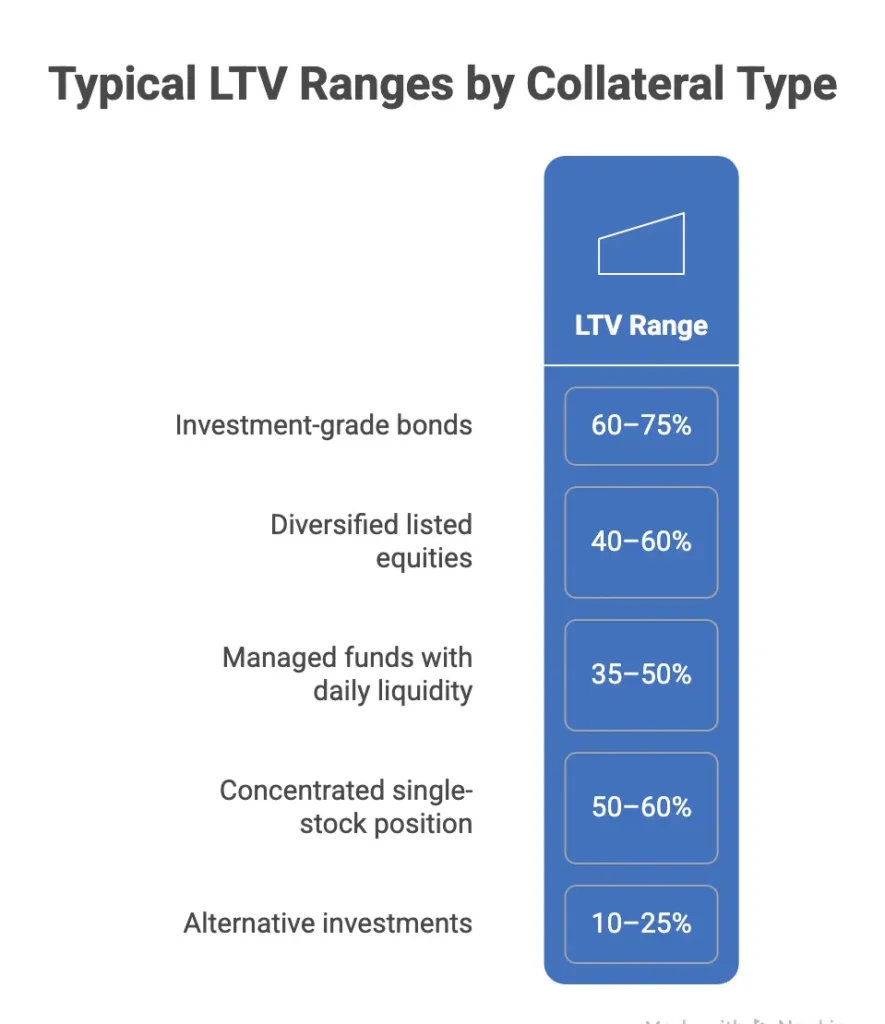

LTV is not a fixed number handed down by a lender. It is a function of negotiation informed by collateral analysis. Borrowers who arrive at that conversation with a prepared position consistently achieve better outcomes than those who accept the first offer without question.

Lombard Loan Case Studies: Three Real Execution Scenarios

Case Studies 1: PE Co-Investment Under Time Pressure

An entrepreneur with a £15M portfolio at a private bank needed to raise £5M to participate in a time-sensitive PE co-investment. The window was 18 days.

The bank’s proposal was limited to listed equities at 25-30% LTV. Under those criteria, eligible collateral left a shortfall of over £1.5M. Selling assets to bridge the gap would have triggered a capital gains liability on positions held for four years. The client was not willing to disrupt the portfolio for a short-term funding requirement.

A full portfolio analysis identified additional eligible collateral beyond the bank’s standard list, including managed funds that the bank had excluded despite established liquidity terms. A specialist lender underwrote at a 40% blended LTV across the full eligible portfolio. Fixed pricing was agreed at the outset to remove repricing risk during the drawdown period.

The full £5M was drawn in 17 days. No assets were sold. The PE position was funded and the original portfolio remained intact. The facility was repaid 14 months later on distribution from the investment.

For borrowers with concentrated equity positions or portfolios that fall outside standard bank eligible collateral lists, the question is rarely whether a Lombard loan is possible. It is which lender’s underwriting framework matches the portfolio.

Case Study 2: Lombard Bridge for a Competitive Property Acquisition

An international executive with a £10M investment portfolio needed to act as a cash buyer on a £3.5M London property. The vendor would not extend the timeline.

Conventional mortgage routes were eliminated at the outset. Cross-border income, currency complexity, and an 8 to 12 week completion timeline were incompatible with the requirement. A short-term Lombard bridge was the only viable structure.

The facility was arranged at approximately 35% LTV against the most liquid portion of the portfolio, with a 12-month term and a defined exit via conventional mortgage refinance. The approach was deliberate: not every eligible asset was pledged. The objective was approval speed, not maximum facility size.

Funds were released in under three weeks. The property was secured ahead of competing buyers. Within six months, a mortgage was in place, the Lombard facility was repaid in full, and the cost of the bridge had been absorbed within the acquisition budget.

This is how Lombard lending functions most effectively as a bridge: not as a permanent financing solution, but as a precision instrument that buys time for a conventional structure to follow. The portfolio was not disrupted. The opportunity was not missed.

Case Study 3: Liquidity Without Triggering Tax Exposure

A high-net-worth individual needed to raise £1M for a family gifting programme. The portfolio comprised an £8M pension structure and a separate £4M personal investment portfolio.

Borrowing against the pension structure was not viable under existing regulatory constraints. Liquidating the personal portfolio would have crystallised a capital gains liability at an unfavourable point in the tax year. The structural problem was not illiquidity. It was sequencing.

A facility was arranged at 25% LTV against the personal portfolio, with interest-only repayments to preserve cash flow. The structure was developed alongside the o confirm compliance with the gifting framework and to ensure no unintended tax consequences arose from the borrowing itself.

The £1M was raised without triggering a taxable event, without touching the pension structure, and without requiring any change to the investment strategy. The facility was serviced from existing income.

This type of scenario is more frequent than it appears. The constraint is rarely the capital itself. It is the interaction between liquidity, regulatory structure, and tax timing that standard lending frameworks are not designed to navigate. For context refer to: liquidity risk intersects with lending structures.

What Lenders Are Actually Assessing in Lombard Loan Scenarios

Lenders evaluating a Lombard facility do not begin with headline portfolio value. They begin with enforceability. A portfolio valued at £10M is assessed by how quickly each line can be liquidated without material market impact. A concentrated position representing 40% of the portfolio attracts a steep haircut not because the company is a poor investment, but because the lender’s ability to enforce against it without moving the price is limited. The BIS framework on collateral haircuts in securities financing reflects this directly: haircut methodology is driven by liquidity and volatility, not nominal value.

Custody structure carries equal weight. Assets held at a well-rated custodian under a clean pledge agreement give a lender enforceable rights from day one. Assets spread across multiple custodians, or held in structures that complicate pledge execution, introduce legal risk that lenders will either price in or decline. Borrowers who consolidate custody and prepare pledge documentation before approaching lenders consistently achieve faster approvals and better terms.

LTV is a negotiating point, not a fixed output. The composition of the collateral, the borrower’s willingness to accept monitoring triggers, the term of the facility, and the clarity of the exit route all affect the advance rate a lender will extend. In each of the three cases above, the final LTV achieved was not the first number discussed. It was the result of a conversation grounded in a prepared collateral analysis, a defined use of funds, and a clear exit. Borrowers who present that package from the outset are in a materially different position from those who present a portfolio statement and wait. For a detailed view of how loan-to-value ratios function across different lending structures and how lenders stress-test collateral.

Every Lombard lender is simultaneously underwriting the exit. For a bridge, that exit is a refinance or sale. For an ongoing facility, it is income servicing or portfolio performance. A facility without a credible exit is either declined or priced at a risk premium that makes it commercially unattractive. The three cases above share one characteristic: each had a defined exit from the first conversation. That is not a coincidence. It is what made each of them executable.

Lender Insight: What Actually Drives Lombard Loan Approval

From a lender’s perspective, Lombard lending is not about portfolio size. It is about control and liquidity.

- Liquidity of underlying securities determines usable collateral

- Concentration directly reduces achievable LTV

- Volatility impacts both pricing and monitoring requirements

- Custody structure determines enforceability

- Ability to take control of assets is non-negotiable

Two portfolios with the same value can produce completely different loan outcomes depending on these factors.

This is where standard private bank solutions often fall short, and where specialist structuring becomes necessary.

For broader context, see the securities-based lending playbook

Execution Is Not Incidental to Lombard Lending

Lombard lending is a structuring decision. Whether a facility is deliverable, and at what terms, is determined before the first conversation with a lender.

The common factor across these Lombard loan case studies is not portfolio size or asset quality. It is the gap between what a standard private bank will underwrite and what a specialist lender, approached with a prepared position, can deliver. In each case the constraint was structural. The solution was structural. The outcome followed directly from the quality of the preparation.

If you are evaluating a Lombard loan facility and want to ensure the terms reflect your portfolio and your objectives, we welcome a discreet conversation, contact us today.

For a more structured breakdown of how these strategies are applied in practice, see the Securities-Based Lending Playbook.