Stock Loans in Australia & Europe: Unlock Liquidity in 2025

In today’s dynamic financial landscape, high net worth individuals (HNWIs), family offices, and institutional investors are continually seeking sophisticated strategies to optimise their capital. As traditional credit avenues tighten and market volatility persists, the ability to access liquidity without disrupting core investment portfolios has become paramount. For those holding significant positions in listed securities, these assets often represent substantial, yet “lazy,” capital.

Stock loans offer a compelling, discreet, and efficient lending solution to unlock this latent value, providing a crucial financial lever in both Australia, APAC and Europe. This article delves into the mechanics, advantages, and critical considerations of stock loans, a form of securities based lending tailored for strategic borrowing and investment.

Stock Loans: When Holding Shares Holds You Back

The current economic climate, characterised by rising interest rates and more cautious traditional lenders, has made accessing capital increasingly challenging. Banks, constrained by stricter regulatory frameworks, are often risk-averse, making conventional borrowing against shares or cryptocurrencies a complex, and sometimes restrictive, process. Yet, many sophisticated investors and family offices possess substantial portfolios of listed equity – valuable assets that, while performing, remain illiquid for immediate capital needs.

The dilemma is familiar: a compelling new investment opportunity arises, a strategic acquisition beckons, or unexpected personal liquidity needs emerge. The conventional response might be to sell a portion of the existing portfolio. However, this can trigger unwelcome capital gains tax (CGT) events, signal market movements, or disrupt long-term investment strategies. This is where the strategic use of stock loans, also known as equity lending or stock financing, comes to the fore. These instruments offer a timely and often misunderstood solution, allowing investors to borrow money against their shares without resorting to an outright sale, thereby preserving their core holdings and future upside potential.

What are Stock Loans? Demystifying the Mechanics

At its core, a stock loan is a non-recourse or limited-recourse loan secured by publicly traded securities. The borrower pledges a specific parcel of their shares as collateral to a specialised lender in exchange for a cash loan amount. Crucially, while the shares are used as security for the loan, the borrower typically retains beneficial ownership or economic exposure to the asset, including any dividend income and potential capital appreciation, depending on the loan structure.

Key characteristics distinguish these sophisticated stock loan arrangements from more common retail products like a typical margin loan from a private bank or brokerage:

- Non-Recourse or Limited-Recourse Nature: This is often marketed as a key differentiator, but it’s important to understand the nuance. In a stock loan structured as non-recourse, the lender’s primary remedy is typically limited to the pledged shares, meaning they cannot pursue the borrower’s other assets. However, most non-recourse or limited-recourse loans still include margin maintenance clauses. If the loan-to-value (LTV) ratio drops below a pre-agreed threshold due to market movements, the borrower may be required to top up the collateral with additional shares or cash to maintain the margin. This differs from traditional margin loans, where margin calls can trigger automatic liquidation or extend to other pledged assets across accounts.

- Collateral Transfer: The pledged shares are usually transferred to a custodian or a Special Purpose Vehicle (SPV) controlled by the lender for the loan term. This temporary transfer of title or a perfected security interest over the shares ensures the lender’s security. Upon full repayment of the loan and any accrued loan interest, the stock back is returned to the borrower.

- Tailored Structures: Unlike standardised bank offerings, stock loans from specialist providers are often highly customised. Terms such as the loan amount, Loan-to-Value (LTV) ratio, interest rate, and repayment schedule can be negotiated to suit the specific needs of the borrower and the characteristics of the pledged equity.

- Off-Balance Sheet Potential: Depending on the jurisdiction and accounting treatment, some stock loan structures may be considered off-balance sheet financing, enhancing financial privacy and potentially improving certain financial ratios.

- Focus on Liquidity, Not Leverage for Speculation: While margin loans are typically used to increase market exposure and can trigger forced sales or cross-asset margin calls, these bespoke stock loans are structured to unlock liquidity from an investment portfolio for broader business or investment purposes. Although non-recourse in nature, most include LTV thresholds that require topping up collateral if values fall, without exposing the borrower’s other assets.

It’s important to distinguish these arrangements from “securities lending” programs run by large custodians where shares are lent out to facilitate activities like short selling. While both involve the lending of securities, the purpose of a stock loan for the borrower (the original shareholder) is to raise capital, not to facilitate another party’s trading strategy. The lender in a stock loan provides cash; in traditional securities lending for short selling, the lender of shares receives a fee.

Stock Loan Advantage: Why Opt for This Flexible Liquidity Tool?

The appeal of stock loans for HNWIs, family offices, and corporate principals lies in a unique combination of benefits, particularly when compared to traditional lending options or outright asset sales.

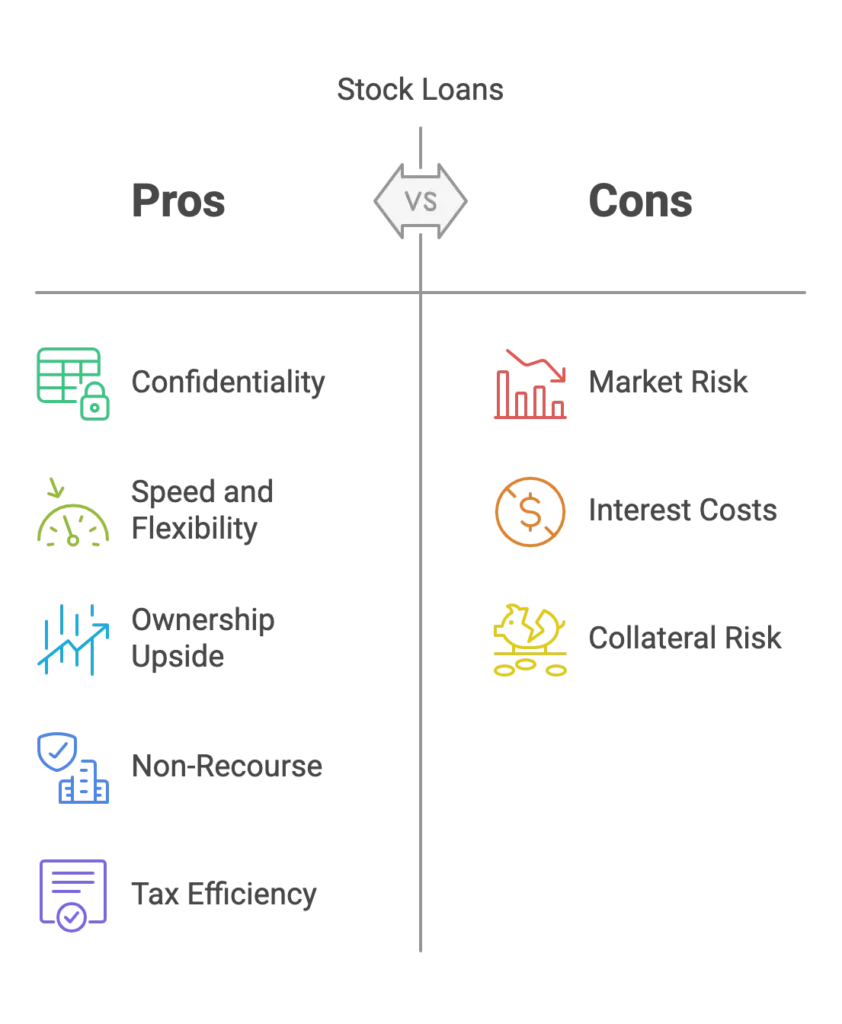

- Confidentiality and Discretion: Transactions are typically private agreements between the borrower and the specialist lender. This avoids public disclosure of share sales, which could negatively impact market perception or alert competitors.

- Speed and Flexibility: The application process for a stock loan can often be quicker than traditional bank financing, especially when dealing with liquid, blue-chip securities. Terms are generally more flexible and tailored to the borrower’s specific circumstances and the nature of the collateral.

- Preservation of Ownership Upside: The borrower retains economic exposure to the pledged shares. If the market value of the stock increases during the loan term, the borrower benefits from this appreciation (net of loan costs). They also typically continue to receive dividends, which can sometimes be structured to service the loan interest.

- Non-Recourse Security: As mentioned, the non-recourse feature provides significant peace of mind, limiting the borrower’s liability to the pledged shares, thus protecting other personal or business assets from potential risks associated with market downturns.

- Tax Efficiency (Jurisdiction-Dependent): A crucial advantage, particularly in jurisdictions like Australia with significant Capital Gains Tax (CGT), is that a properly structured stock loan is not a disposal event. This means the borrower can secure a loan and access liquidity without having to sell their shares and trigger an immediate CGT liability. This allows for strategic capital deployment while deferring tax events.

- Diversification Without Selling: Proceeds from a stock loan can be used to diversify investments, for portfolio rebalancing, perhaps to invest in managed funds, real estate, or private equity, without crystallising gains on existing concentrated stock positions.

Jurisdictional Nuances:

- Australia: The CGT deferral is a primary driver. Founders of newly listed companies or long-term holders of appreciated stock find this particularly attractive. The ability to borrow money to invest in other ventures or meet liquidity needs without an immediate tax burden is a powerful incentive. However, it’s crucial to ensure the structure complies with Australian tax law to avoid being deemed a disposal.

- Europe (e.g., Switzerland, UK, Luxembourg): European family offices and HNWIs often utilise stock loans for diverse purposes. These can include providing a liquidity bridge during complex estate planning or succession, seeding new private equity vehicles without diluting existing holdings or involving traditional banks, or discreetly raising capital for strategic opportunities. The sophisticated financial infrastructure in these regions supports complex stock financing and equity lending arrangements, often involving offshore custodians and SPVs for enhanced privacy and efficiency.

Real-World Scenarios: Stock Loans in Action

To illustrate the practical applications of this lending solution, consider these scenarios:

- Australia – The Tech Founder’s Diversification:

- Situation: The founder of a recently ASX-listed technology company holds a significant portion of their wealth in company stock. They wish to diversify by acquiring a commercial real estate property but are hesitant to sell a large block of shares, fearing negative market signalling and a substantial CGT bill.

- Solution: The founder engages a specialist asset based lender to arrange a stock loan, pledging a portion of their shares as collateral. They receive a loan amount equivalent to 60% of the shares’ current market value.

- Outcome: The founder successfully acquires the real estate, diversifies their asset base, and defers CGT. The stock loan is structured with an interest rate that is partially offset by the dividends from the pledged shares. They retain upside potential in their tech company stock.

- Switzerland – The Family Office’s Private Equity Play:

- Situation: A multi-generational Swiss family office identifies a compelling co-investment opportunity in a new private equity fund. They need to commit €10 million within a short timeframe but prefer not to liquidate part of their core blue-chip equity portfolio, which is managed for long-term growth.

- Solution: They utilise a stock loan facility, pledging a diversified basket of their European blue-chip shares held with a private custodian. The lender provides the required capital quickly.

- Outcome: The family office seizes the private equity opportunity without disrupting their strategic asset allocation or facing the delays and scrutiny of traditional bank borrowing. The non-recourse nature of the loan protects their broader wealth.

- London – The Entrepreneur’s Bridge Finance:

- Situation: A UK-based entrepreneur is awaiting the proceeds from the sale of a privately-held business, which is taking longer than anticipated. They require £5 million in bridge finance to pursue another time-sensitive investment. Their primary liquid asset is a substantial holding in a FTSE 100 company.

- Solution: A wealth manager facilitates a short-term stock loan for the client with a broker. The shares are custodied offshore, and the loan is structured with flexible repayment terms, allowing for early settlement once the business sale completes.

- Outcome: The client accesses the necessary liquidity discreetly and efficiently, bridging the financial gap without a fire sale of their listed equity. The lender understood the temporary nature of the need and tailored the loan term accordingly.

Why Are Stock Loans Gaining Popularity?

Several converging factors are contributing to the renewed relevance and increasing popularity of stock loans among sophisticated investors:

- Credit Tightening by Traditional Banks: As regulatory pressures increase and economic uncertainty looms, traditional banks have become more conservative in their lending practices, particularly for securities-based borrowing. This pushes HNWIs and businesses to explore alternative lending solutions.

- Unlocking ‘Lazy Capital’: Large, concentrated holdings of listed securities often represent “lazy capital”, valuable but not actively working to generate immediate liquidity or fund new opportunities. Stock loans activate this capital.

- Demand for Capital Agility: The post-pandemic economic landscape and evolving market dynamics necessitate greater capital agility. Investors need to be able to move quickly to seize opportunities or manage unforeseen circumstances. Stock loans allow you to borrow swiftly.

- Technological and Transparency Improvements: Advances in financial technology, secure custodial arrangements, and improved data analytics are enabling more efficient and transparent pricing from specialist lenders. This enhances borrower confidence.

- Evolution of Offshore Structuring: Sophisticated offshore financial centres have refined their legal and regulatory frameworks, allowing for compliant, secure, and efficient structuring of stock loans, often utilising SPVs for enhanced asset protection and confidentiality.

- Increased Awareness and Education: Wealth managers, private bankers, and financial advisors are becoming more familiar with the strategic benefits of stock loans, recommending them to clients where appropriate as part of a holistic wealth management strategy.

Key Considerations Before Choosing a Stock Loan

While stock loans offer compelling advantages, they are complex financial instruments — which makes borrower due diligence on the lender, and careful evaluation of terms, absolutely essential:

- Asset Type and Liquidity: Not all listed securities are eligible. Lenders typically prefer shares with high liquidity, a substantial market capitalisation, and relatively low volatility. Shares traded on major exchanges (e.g., ASX, LSE, SGX and major European bourses) are generally favoured. Bonds, ETFs and certain managed funds (if listed) may also be considered.

- Loan-to-Value (LTV) Ratios: The LTV represents the percentage of the shares’ market value that the lender is willing to advance as a loan amount. LTVs typically range from 40% to 70%, depending on the quality and volatility of the stock, market conditions, and the overall structure of the loan. A lower LTV offers a greater buffer against market risk for the lender.

- Jurisdictional Treatment and Tax Implications: This is paramount. In Australia, ensuring the stock loan does not trigger a CGT event requires careful structuring. In Europe, withholding taxes on dividends and cross-border considerations must be addressed. Always seek specialist tax and legal advice relevant to your jurisdiction. The information prepared without taking into account your specific financial situation or needs is general; professional advice is crucial.

- Custody and Legal Structure: Understand where and how your shares will be held during the loan term. Reputable lenders use established, regulated custodians. The legal agreements, often involving an SPV, should be thoroughly reviewed by legal counsel. The security arrangements for the collateral are critical.

- Term and Cost: Loan terms can range from 2-5 years. Shorter terms, although possible, will cost more. Interest rates vary based on the LTV, the underlying stock’s risk profile, the loan amount, duration, and prevailing market rates. Some lenders offer interest-only payments, while others may require amortisation. Be clear on all fees, including setup, legal, and custodial charges.

- Lender Reputation and Expertise: Work only with trusted, experienced, and well-capitalised lenders or specialist brokerage firms with a proven track record in stock financing and equity lending.

- Potential Risks:

- Market Risk: While often non-recourse to other assets, a significant drop in the value of the collateral could, in some limited-recourse scenarios or at loan renewal, lead to requirements to put up collateral (more shares) or a portion of the loan being called if not purely non-recourse.

- Counterparty Risk: The risk associated with the lender itself, although typically mitigated by robust legal structures and custodial arrangements.

- Loss of Voting Rights: Depending on the structure, the borrower might temporarily lose voting rights associated with the pledged shares. Typically, not the case, this needs to be clarified upfront.

- Complexity: These are not simple loans. The documentation and structure can be intricate, requiring professional advice.

It’s worth distinguishing products like NAB Equity Builder, where NAB acts as the issuer. These facilities are designed for individuals borrowing to invest in approved managed funds or listed securities, and typically involve recourse and variable interest rates of up to 9.75% p.a., which is extremely high by private lending standards.

In contrast, the stock loans discussed here are strictly non-recourse, offer significantly lower fixed rates and fixed terms, and are arranged through private lenders or specialised institutions for HNWIs seeking flexible liquidity against substantial existing shareholdings, without the need to sell or assume personal liability.

Conclusion: Liquidity Without Compromise, Security Through Strategy

In a financial world where flexibility is power and strategic capital allocation is key to wealth preservation and growth, stock loans offer a quiet but potent lever. For HNWIs, family offices, and corporate leaders holding significant listed equity portfolios in Australia, UK and Europe, it is time to reconsider how capital is accessed. The ability to borrow money and unlock substantial liquidity without having to sell core assets, trigger immediate tax liabilities, or lose exposure to future market upside is a game-changer.

These sophisticated securities lending arrangements, when structured correctly with reputable partners, provide a discreet, efficient, and strategically advantageous path to funding new ventures, managing financial obligations, or diversifying investments. By understanding the mechanics, benefits, and critical considerations of stock loans, decision-makers can harness the full potential of their listed assets, transforming lazy capital into active, productive financial power. This form of borrowing against security is more than just a loan; it’s a strategic financial tool for the discerning investor.

How We Can Help You Unlock Liquidity

At Forbes Le Brock, we provide discreet, structured lending solutions for clients holding significant listed equities across Australia, APAC, UK, Europe, and other major markets.

We also support U.S. equities held by non-U.S. residents. Our tailored stock loans and securities-based lending facilities enable access to capital without triggering a sale or disrupting your long-term investment strategy.

If you or your clients are exploring strategic capital options, arrange a confidential, no-obligation call to discover how we can help unlock liquidity while preserving your core holdings.

🎧 Prefer to listen? Catch the key takeaways from our Stock Loans Australia & Europe: 2025 Guide, in the latest → Deep Dive