Loan Against Investment Portfolio: Access Liquidity Without Selling

A loan against investment portfolio is one of the more misunderstood structures in securities-based lending. The concept is straightforward: pledge listed assets as collateral, draw capital, retain ownership. The execution is not, because lenders are not assessing a single position. They are assessing a mixed pool of assets, each with different liquidity profiles, volatility characteristics and correlation risks.

This post explains how that assessment works in practice, how lenders size a facility against a diversified portfolio, and where the structure differs materially from a stock loan or a margin facility.

How a Loan Against an Investment Portfolio Is Structured

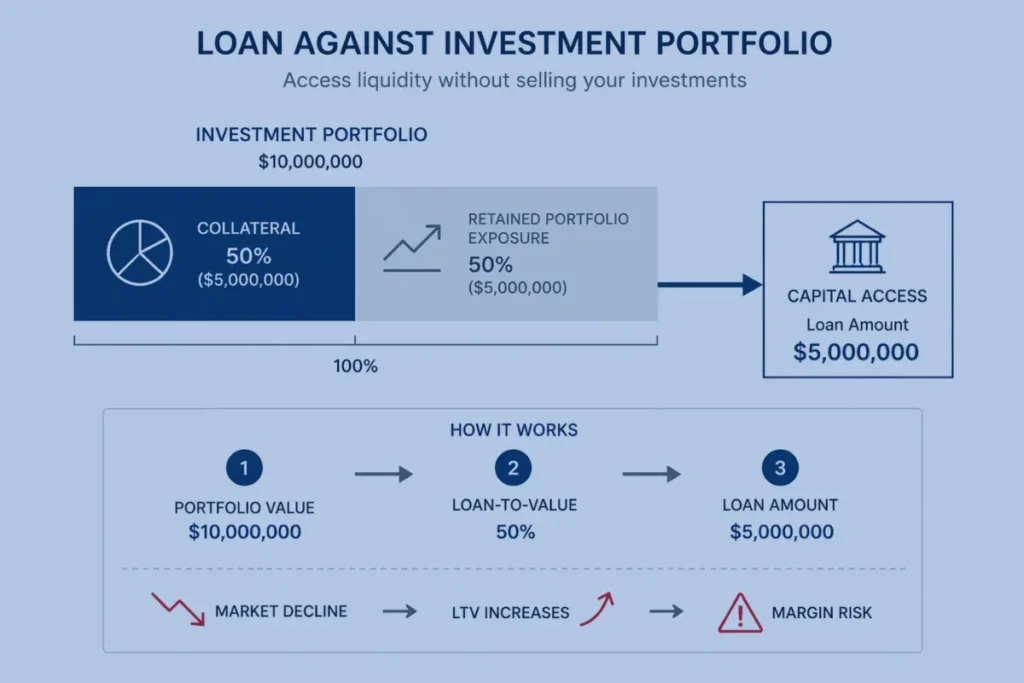

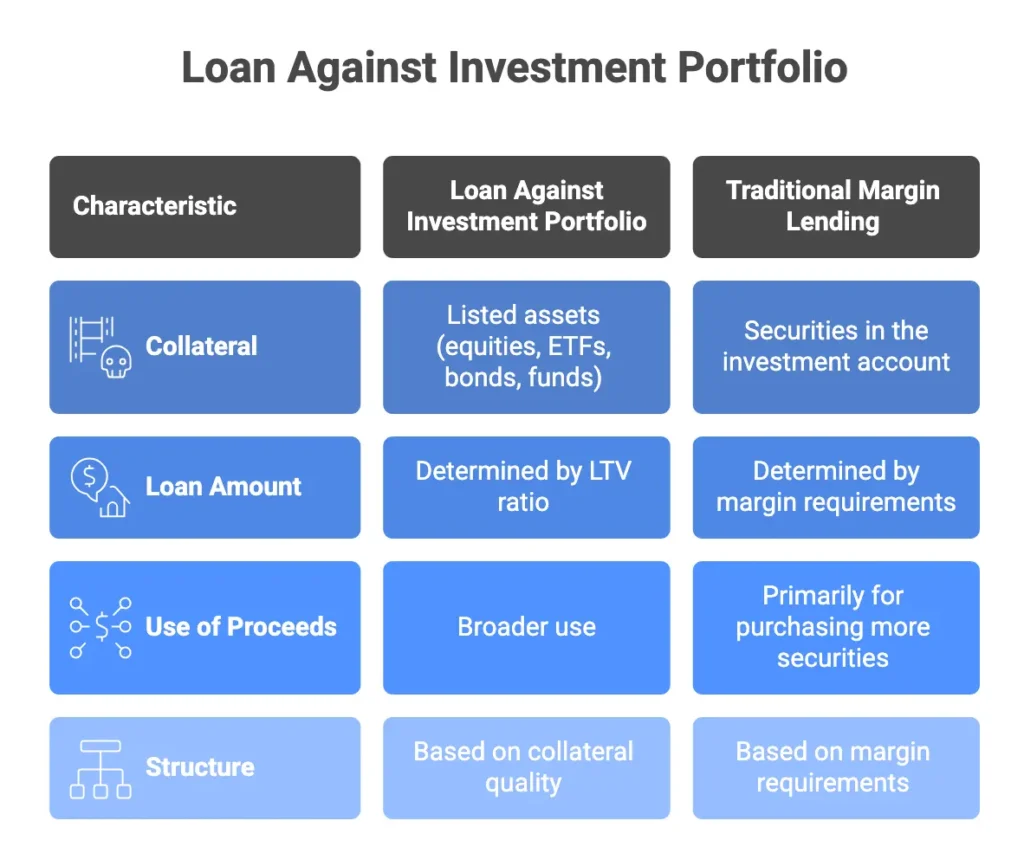

A loan against investment portfolio is a form of securities-based lending in which a diversified pool of listed assets is pledged as collateral. Eligible securities typically include listed equities, ETFs, investment-grade bonds and liquid funds. The borrower retains beneficial ownership throughout. The lender takes a security interest over the pledged assets, which activates only on default or a missed margin call.

The facility is sized using a loan-to-value ratio applied across the eligible pool. A well-diversified, liquid portfolio might support 50 to 65% LTV. A portfolio with significant concentration, illiquid positions or high volatility will attract lower LTV, or have portions excluded from the eligible pool entirely.

This is structurally different from a margin loan. Margin lending is designed for leveraged investing within a brokerage account, uses standardised margin rules and restricts use of proceeds. A loan against investment portfolio is structured around the quality of the collateral and permits broader capital deployment. For a detailed comparison of mechanics, How Do Securities-Backed Loans Work? covers the underlying structure.

How Lenders Assess a Mixed Collateral Pool

Portfolio composition

The asset mix sets the floor for achievable LTV. A portfolio weighted toward large-cap equities and investment-grade bonds attracts higher advance rates than one concentrated in small-cap, emerging market or sector-specific positions. Each asset class carries a different haircut, and those haircuts are applied position by position before the blended LTV is calculated.

Concentration within the pool

A well-diversified portfolio can still carry significant concentration risk. A single position representing 30% or more of the portfolio value is underwritten as a single-name risk and discounted accordingly, regardless of what else is held alongside it. Lenders do not aggregate away concentration risk. How that risk builds gradually through market movement is covered in Portfolio Drift Rebalancing 2026.

Aggregate liquidity

Daily traded value across all positions matters more than total portfolio value. Where a position is large relative to its average daily volume, the lender applies an additional discount to reflect the execution risk of orderly realisation. Very illiquid positions may be excluded from the eligible pool altogether.

LTV, Haircuts and Margin Thresholds

LTV is not a single figure applied uniformly. It is the output of individual haircuts applied to each position, then aggregated across the eligible pool.

A large-cap listed equity might attract a 65 to 70% advance rate. An ETF tracking a volatile index might attract 55%. An illiquid small-cap holding may be excluded entirely. The blended LTV reflects the weighted outcome across all eligible positions. For a detailed explanation of how LTV thresholds are structured in secured lending, see Loan to Value in Securities-Based Lending.

Understanding advance rates and haircut methodology in institutional securities lending provides useful context for how private lenders approach the same mechanics, though terms vary significantly.

If the portfolio declines in value, the outstanding loan becomes a larger proportion of the eligible collateral pool. At the margin call threshold, additional collateral must be pledged or a portion of the loan repaid. In practice, lenders set this threshold conservatively, creating a buffer that triggers a review conversation well before the facility reaches forced realisation.

Custody and Control During the Facility

Collateral is pledged to an approved custodian. Upon closing, the collateral is released to the lender and the borrower is paid.

Some structures permit collateral substitution: positions can be swapped provided the replacement meets eligibility criteria and does not weaken the blended LTV. This flexibility matters for investors managing active portfolios who do not want a static lock on the entire holding.

During the facility term, dividend income and coupon payments on pledged collateral are typically passed through to the borrower, though the mechanics depend on the loan agreement. Corporate actions require lender consent. Voting rights are generally retained by the borrower, but this should be confirmed at the structuring stage, as terms vary across lenders and jurisdictions.

Loan Against an Investment Portfolio vs. Stock Loan: Different Situations

A loan against investment portfolio and a stock loan address different problems and are underwritten differently.

A stock loan is built around a single concentrated position, typically a founder holding, executive stake or anchor shareholding. Credit assessment focuses on that single asset: its tradeable liquidity, volatility, any lock-up or regulatory restrictions, and the exit options available to the lender.

A loan against investment portfolio is assessed across a diversified pool. Spread risk typically supports higher LTV on the overall facility, but the multi-asset structure introduces complexity: haircuts, eligibility and concentration must be managed across the entire pool. If the primary need is raising capital against a specific concentrated holding, Stock Loans for Concentrated Shareholders addresses that structure in detail.

Lender Insight: How Mixed Portfolios Are Actually Underwritten

From a lender’s perspective, a loan against investment portfolio is not underwritten on current value. It is underwritten on what the eligible pool looks like after a 20 to 25% drawdown.

Composition determines the eligible floor

Lenders run stress scenarios to identify the minimum eligible pool value under adverse market conditions. Positions that fall below minimum market cap or daily volume thresholds drop out of the eligible pool under stress. The facility is sized against what remains, not peak portfolio value.

Haircuts are applied before aggregation

Each position is haircut individually. A portfolio that appears well-diversified may carry implicit concentration if multiple top holdings are highly correlated. Lenders assess pairwise correlation across the largest positions to identify this. Two positions that each represent 12% of the portfolio but move together function as a 24% single-name risk under stress.

Usable LTV is lower than the headline rate

The margin call threshold is set conservatively, typically 10 to 15 percentage points above the default level. The practical result is that the borrower cannot draw to the full headline LTV without immediately sitting inside the margin buffer. Experienced borrowers structure the facility with headroom built in from the outset.

Custodian quality affects both terms and speed

Facilities secured through recognised custodians, prime brokers or major banks can process faster and attract better pricing. Where assets are fragmented across platforms or custodians with limited standing, consolidation adds time and occasionally cost to execution.

When This Structure Is Appropriate

A loan against investment portfolio is most suitable where:

- Capital is needed for a specific opportunity, investment or liquidity event, but a long-term portfolio position should not be liquidated

- The portfolio is genuinely diversified and holds sufficient liquid positions to support an adequate eligible pool

- The borrower can service the loan from external cash flow rather than relying on portfolio income

- The facility is structured with enough LTV headroom to absorb normal market volatility without triggering the margin call threshold

It is less suited to portfolios that are heavily concentrated, where the borrower depends on portfolio income to service the debt, or where the underlying assets are thinly traded.

Structuring a Facility

If you hold a diversified listed portfolio and require capital without liquidating positions, the terms available will depend directly on portfolio composition, custody arrangements and the size of the facility required.

Forbes Le Brock structures and places portfolio lending facilities for UHNW investors, family offices and private clients across the UK, Europe and Asia-Pacific. If you are assessing whether your portfolio supports a facility, we welcome a discreet conversation.