How Investors Unlock Liquidity from Blue Chip Shares Without Selling

For many investors, blue chip shares represent the core of long-term wealth. They provide stability, dividend income, and exposure to globally recognised companies.

The problem is not performance, it is liquidity.

When capital is needed, selling these positions can trigger tax, disrupt allocation, and remove exposure at the wrong time. This creates a structural tension between maintaining high-quality holdings and accessing capital when opportunities arise.

In 2025, more investors are solving this problem differently. Instead of selling, they are borrowing against blue chip shares to unlock liquidity while keeping their portfolios intact.

This is not a workaround. It is a deliberate capital strategy.

The Liquidity Dilemma: How to Avoid Selling Blue Chip Shares to Raise Capital

For many investors, blue chip shares represent stability, dividend income, and long-term exposure to high-quality companies.

The issue is not performance, it is liquidity.

When capital is needed, selling creates problems: tax, portfolio disruption, and loss of future upside. In many cases, this forces poorly timed decisions or unnecessary portfolio rebalancing.

As a result, investors face a simple question: how do you access capital without selling the assets that underpin your portfolio?

What Is Blue Chip Shares Backed Lending? A Smart Alternative to Selling Stocks

A blue chip shares backed lending strategy, part of securities-based lending, is a secured loan against listed equities.

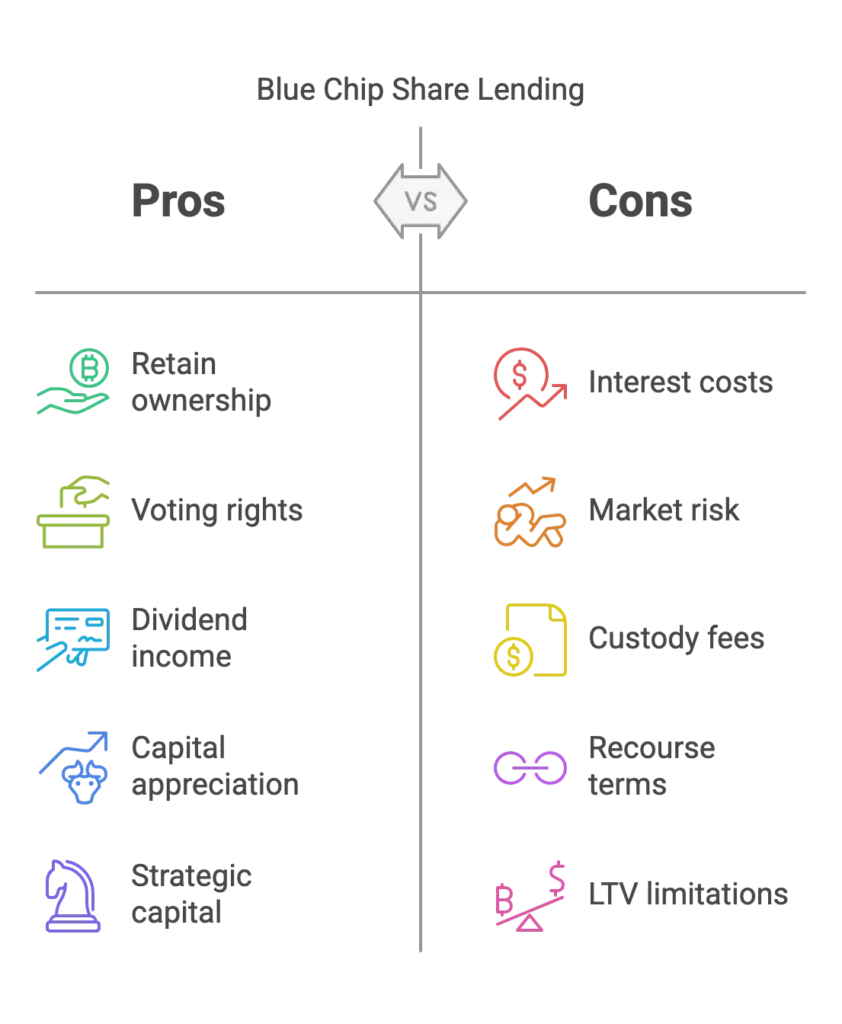

Instead of selling, investors use their shares as collateral to access liquidity while retaining ownership, voting rights, and market exposure.

These facilities are typically arranged through private lenders and structured finance desks.

Key Mechanics:

- Loan-to-Value (LTV): Driven by liquidity, not labels. For a deeper breakdown, see how the loan to value ratio is actually set in practice.

- Custody: Shares are held in a designated custody account with beneficial ownership retained.

- Recourse: Can be full, limited, or non-recourse depending on structure. Non-recourse is common in properly structured facilities.

- Interest Rates & Terms: Can be full, limited, or non-recourse depending on structure. Non-recourse is common in properly structured facilities.

This is not speculative borrowing. It is a structured way to extract liquidity from an existing portfolio without forcing a sale.

Why Lending Against Blue Chip Shares is Popular Among Investors

The current financial climate amplifies the appeal of blue chip shares backed lending. Here’s why it offers a distinct advantage:

- Maintained Market Exposure: Retain ownership of blue chip shares, benefiting from stock market upside and growth potential of blue chip companies.

- Tax Efficiency: Pledging blue chip stock isn’t a disposal, so no immediate CGT, allowing wealth to grow. A significant advantage over selling stocks to buy other assets.

- Preservation of Dividend Income: Continue receiving all dividend payments from pledged blue chip shares.

- Rapid Access to Liquidity: Quicker than property-backed loans or raising private equity.

- Discreet and Tailored Structuring: Highly customised terms, offering discretion preferred by UHNW individuals.

- Capital Efficiency: Makes existing assets work harder, leveraging blue chip shares for new investment opportunities.

- Strategic Portfolio Management: Facilitates dynamic portfolio adjustments, allowing diversification without selling best blue-chip stocks inopportunely.

This strategy aligns with wealth preservation, strategic capital deployment, and efficient management of a portfolio’s allocation to stocks, especially with large market capitalisation entities.

Real-World Scenarios: Putting Blue Chip Shares Finance into Practice

The versatility of blue chip share backed finance applies across various scenarios:

Family Office Diversifying into Private Equity

A family office with a £100M FTSE 100 blue chip shares portfolio needs £20M for a private equity investment. They secure a loan against their blue chip stock, avoiding CGT and maintaining their core holdings in these blue-chip companies while accessing capital. This allows them to invest in blue chip growth and private equity.

Entrepreneur Bridging to a Capital Event

A founder with personal blue chip shares needs £5M for a strategic acquisition pre-IPO. Leveraging their blue chip stock, they secure a flexible loan, repayable from IPO proceeds, avoiding dilution.

Asset Manager Seizing Real Estate Opportunities

An asset manager needs swift capital for a real estate deal for an UHNW client with a diverse blue chip shares portfolio (including blue-chip stocks in the UK). A credit line against these stocks provides immediate funds without liquidating stocks.

The Rising Tide: Why This Strategy is Gaining Prominence

Blue chip shares are not the story here. Liquidity is.

The growth in this space is being driven by structural changes in how capital is accessed, not by the assets themselves. As a result, securities-based lending is increasingly used as a practical alternative to traditional credit.

What’s Driving This Shift

- Tighter bank lending: Balance sheet constraints and risk limits are reducing flexibility.

- More specialist lenders: Private credit and structured lenders are filling the gap.

- Better risk and custody infrastructure: Execution is now more reliable across jurisdictions.

- Tax efficiency focus: Borrowing avoids immediate disposal and preserves structure.

- Demand for discretion: Private solutions avoid market signalling and disclosure.

- Recognition of embedded liquidity: Large equity positions are now treated as financeable assets, not just investments.

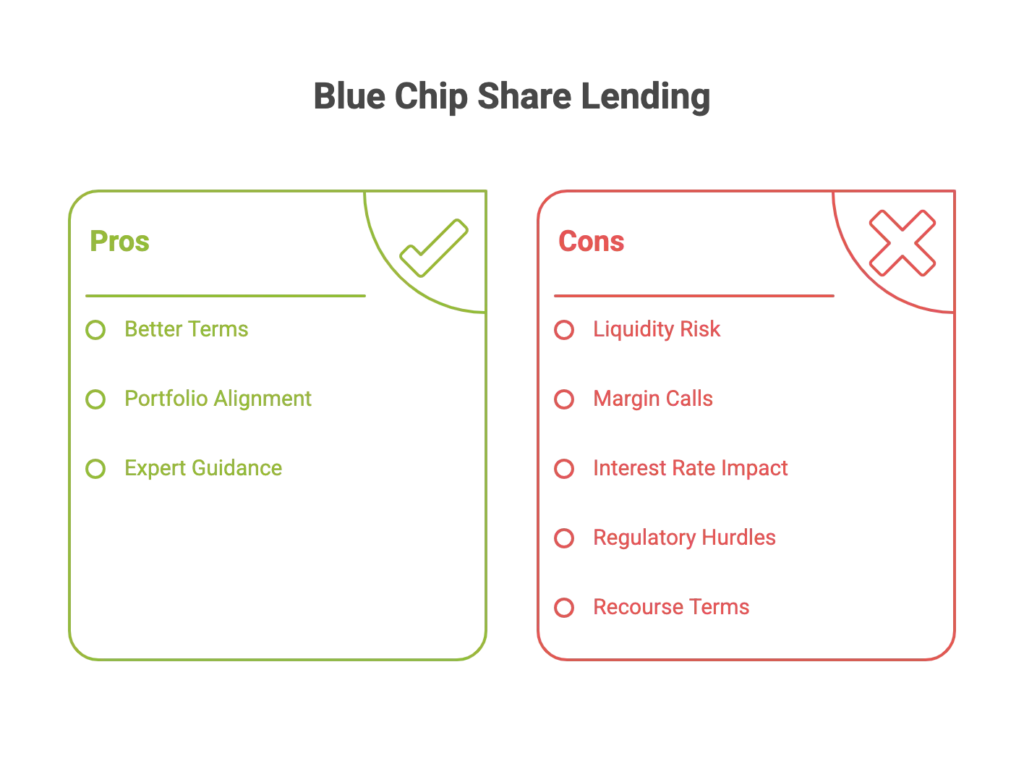

Key Considerations: Navigating Blue Chip Shares Finance Wisely

This structure is straightforward, but execution is not. Terms are driven by liquidity, structure, and lender behaviour.

- Liquidity and position size: Borrowing capacity is driven by trading volume and how large the position is relative to the market.

- Lender Appetite: Different lenders have different mandates, jurisdictions, and size preferences. Not all assets are financeable.

- Custody and Control: Shares must sit in an acceptable custody structure with clear rights over dividends and corporate actions.

- Downside protection: Understand how the facility behaves if the share price falls. Margin calls or pre-agreed protections will apply.

- Recourse: Know whether exposure is limited to the collateral or extends beyond it.

- Interest Rate: Rates are defined upfront, but still need to be assessed against the purpose of the financing.

- Regulatory constraints: Insider status, restrictions, or disclosure rules can affect whether a transaction is possible.

- Strategic fit: This should support your broader portfolio, not distort it.

If structured correctly, this is a capital tool, not a risk event.

Lender Insight: What Actually Drives Terms on Blue Chip Shares

Lending against blue chip shares is not about the label “blue chip”. It is about liquidity and execution risk.

From a lender’s perspective, three factors matter:

- Average Daily Trading Volume (ADTV): This ADTV is the single biggest driver. If a position cannot be exited in the market without disruption, it cannot support size. Large caps with strong turnover consistently achieve better terms.

- Position Size vs Market Liquidity: A £50M position in a highly liquid stock is very different from £50M in a thinner name. Terms tighten when the position represents multiple days of trading volume.

- Jurisdiction and Settlement Infrastructure: Eligible exchanges, custody mechanics, and enforceability matter more than most borrowers expect.

Not all listed shares are financeable, even if they appear “blue chip”.

In practice, this means two investors holding similar “quality” stocks can receive very different outcomes.

The difference is not credit quality, it is liquidity profile and structure.

Conclusion: Strategic Liquidity Without Compromis

Leveraging blue chip shares for liquidity is no longer niche. It is a practical solution for investors who need capital without disrupting core holdings.

The advantage is simple: access liquidity, avoid forced sales, and maintain exposure to high-quality assets.

Used correctly, stock loans are not leverage for the sake of it. It is a controlled way to improve capital efficiency while preserving long-term positioning.

If you are managing a concentrated equity position and need liquidity without selling, a properly structured facility can materially change your options.

You can make a confidential enquiry here.