How Securities-Backed Loans Work in Practice

Understanding how securities-backed loans work is critical when borrowing is driven by collateral behaviour and lender control, not access. Borrowing capacity depends on collateral quality, executable liquidity, and how the lending arrangement performs under market conditions. This detailed exposition will dissect the operational framework of securities-backed loans from a structuring and lender perspective, focusing exclusively on the practicalities of their implementation.

What is a Securities-Backed Loan?

A securities-backed loan is a collateralised financing structure where a borrower obtains a loan or line of credit by pledging marketable securities from their investment portfolio as collateral. The structure enables borrowing against the value of pledged securities.

The investment portfolio serves as collateral, with ownership retained, but control restricted during the loan term. This is the foundation of how securities-backed loans work.

How Securities-Backed Loans Work in Practice

Execution follows a defined process driven by lender risk assessment, which determines how securities-backed loans work in real terms

Initially, the lender undertakes a comprehensive assessment of the borrower’s marketable securities. Assessment focuses on executable liquidity and risk, not just market value. Eligibility varies by liquidity, volatility, and concentration. Not all securities meet lender criteria, regardless of headline value. Highly liquid, publicly traded equities and investment-grade bonds are typically preferred due to their predictable valuation and ease of liquidation if required. Illiquid or concentrated positions may be excluded or subject to tighter terms.

Following the collateral assessment, the lender determines the value of pledged securities and subsequently establishes the maximum loan amount or credit line available to the borrower. Loan amount is derived from liquidity, volatility, and lender risk parameters.

Once the borrowing capacity is established, the lending arrangement is formalised. This agreement outlines the terms, including the interest rate, repayment schedule, and the conditions under which the collateral for a loan is secured. The lender then takes control of the pledged securities, typically by holding them in a segregated account. Ownership is retained, but control over pledged securities is restricted.

Finally, upon the successful establishment of the lending facilities and the securing of collateral, the loan proceeds are released to the borrower. These funds are then available for deployment as per the borrower’s requirements, subject to any stipulations within the lending arrangement, such as restrictions on using the proceeds to purchase additional securities within the same collateralised account.

Collateral and Loan-to-Value Mechanics

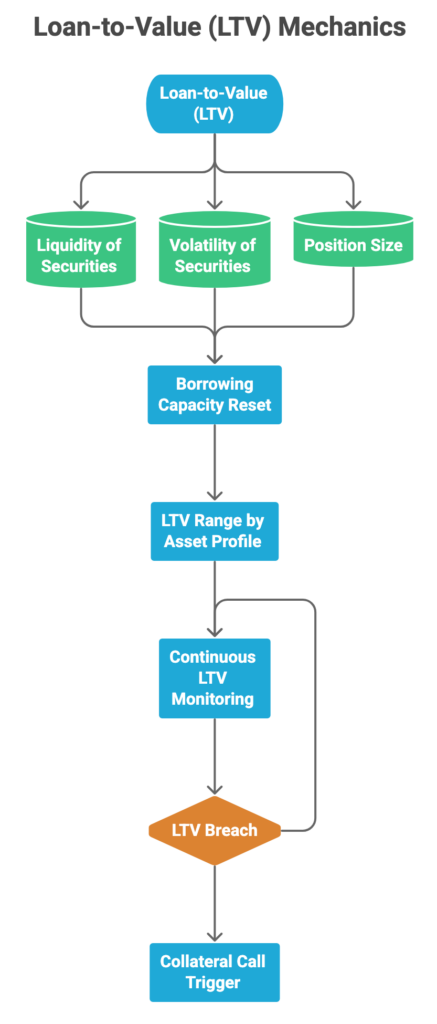

The cornerstone of how securities-backed loans work lies in the mechanics of collateral and the loan-to-value (LTV) ratio. The LTV ratio represents the proportion of the loan amount relative to the market value of the pledged securities. Loan to value is dynamic and reset based on risk:

- Market Value of Pledged Securities: Market value is a reference point, not the decision driver.

- Liquidity of Securities: Highly liquid securities, which can be readily sold without significantly impacting their price, typically command higher LTV ratios. Less liquid assets result in lower LTVs.

- Volatility of Securities: Assets with higher price volatility are considered riskier and are assigned lower LTVs to provide a buffer against price declines.

- Diversification of the Investment Portfolio: A well-diversified portfolio reduces concentration risk and can support more favourable LTVs than a concentrated position.

- Market Conditions: During periods of heightened volatility or uncertainty, lenders may reduce LTVs to manage exposure.

Borrowing capacity is set at inception based on liquidity, volatility, and position constraints, not adjusted dynamically as markets move. For instance, a portfolio of highly liquid listed equities may support an LTV around 50%, with adjustments driven by liquidity, volatility, and position size. Less liquid or more volatile positions are structured more conservatively or may not be financeable.

Once in place, the LTV ratio is continuously monitored rather than reset. A decline in collateral value increases the effective LTV against a fixed loan amount, which may lead to margin pressure and trigger collateral calls.

This dynamic is central to how securities-backed loans work under changing market conditions.

Margin Call and Liquidation

A critical aspect of how securities-backed loans work is the mechanism of the margin call and the lender’s right to liquidate pledged securities. This is the lender’s primary control mechanism.

A margin call is triggered when the market value of pledged securities falls below a predetermined threshold, causing the LTV ratio to exceed the agreed-upon maximum. This threshold is explicitly defined within the lending arrangement terms. The lender issues a margin call requiring immediate action.

The borrower typically has two primary options to address a margin call:

- Provide additional collateral: The borrower can pledge more eligible securities from their investment portfolio to increase the total value of pledged securities, thereby reducing the LTV ratio back to an acceptable level.

- Repay part of the loan: Under some structures, the borrower can make a partial principal payment on the outstanding loan amount, which directly reduces the numerator of the LTV calculation, bringing the ratio back into compliance.

Failure to meet a margin call allows the lender to liquidate pledged securities without consent. Liquidation is executed to recover the loan and protect lender capital. It is imperative to understand that this liquidation occurs at the prevailing market value, which may be significantly lower than the original purchase price of the securities, potentially crystallising substantial losses for the borrower. The lender is not obligated to seek the borrower’s consent before liquidation once a margin call has been breached.

Interest Rate and Repayment Structure

Cost is driven by interest rate and repayment structure.

Interest rate treatment depends on the lender and structure. Bank securities-backed lines are often variable, commonly linked to benchmarks such as SOFR plus a spread.

Private stock loan or securities-backed loan structures may instead use fixed interest for a defined term. The difference matters because variable-rate facilities expose the borrower to benchmark movement, while fixed-rate structures provide clearer cost certainty from the outset.

Repayment structures vary depending on the facility. Many securities-based lines of credit facilities allow for interest-only payments for a defined period, with the principal due at maturity or on repayment. This structure defers principal repayment. Term loans involve scheduled payments of both principal and interest over a defined period.

Regardless of structure, the full outstanding loan amount is due at the end of the term. .

The lending arrangement sets payment frequency, method, and any penalties for late or early repayment.

Risks Associated with Securities-Backed Loans

Securities-backed loans carry structural risks that must be understood.

Market volatility is the primary risk driver. A downturn in market conditions can rapidly reduce the value of pledged securities and trigger a margin call. Even in stable markets, a decline in the value of specific securities within the portfolio can have the same effect.

Forced liquidation is the defining downside risk. If a margin call is not met, the lender can sell pledged securities to reduce exposure. Forced liquidation can lock in losses under adverse conditions and materially alter the borrower’s investment position.

Interest rate risk must also be considered. For variable-rate structures, increases in benchmark rates such as SOFR raise the cost of borrowing over time.

Concentration risk further amplifies exposure. A portfolio heavily weighted to a single position or sector is more vulnerable to valuation declines, increasing the likelihood of margin pressure and enforcement.

What to Check Before Entering a Securities-Backed Loan

Before entering a loan, key structural factors must be assessed.

Eligible securities should be clearly defined. Confirm which assets within the investment portfolio qualify as collateral and understand any restrictions or haircut assumptions applied by the lender.

The value of pledged securities must be understood in practical terms. This includes how the lender calculates market value and how that translates into the applicable loan-to-value ratio.

Review lending arrangement terms, including pricing, repayment, and covenants. The structure of the facility determines how the loan performs over time, not just at inception.

Margin call exposure must be fully understood. This includes the specific LTV thresholds that trigger a margin call, the notification process, and the timeframe for remediation, as well as the borrower’s ability to respond.

Assess ability to meet repayment and margin requirements under stress. This includes both ongoing interest obligations and the capacity to reduce exposure or provide additional collateral if conditions deteriorate.

Conclusion

Outcomes are driven by collateral behaviour, lender control, and execution under market conditions. For high-level decision-makers, understanding how securities-backed loans work in practice is a critical component of financial strategy. The structure enables borrowing against an investment portfolio but requires a clear understanding of LTV mechanics, margin exposure, and the lender’s right to liquidate pledged securities.

If you are evaluating a securities-backed loan, the key variable is not access to borrowing, but how the structure performs under changing market conditions. A focused discussion can clarify achievable loan size, collateral requirements, and risk profile based on the underlying securities.

If you are assessing a securities-backed loan against a specific position, get in touch to assess whether your position can actually support a loan, and under what constraintsFor a more structured breakdown of how these strategies are applied in practice, see the Securities-Based Lending Playbook