Cross Collateralisation in Private Credit: Multi-Asset Loan Structures

In the intricate world of high-stakes finance, where capital structures are as unique as the portfolios they underpin, the strategic deployment of credit is paramount. For UHNW individuals, family offices, and institutional investors, the ability to unlock liquidity and optimise borrowing power without immediate asset disposal is a constant pursuit. In 2026, with underwriting discipline tightening and refinancing windows narrowing, cross collateralisation in private credit has shifted from technical detail to structural necessity.

Borrowers holding concentrated positions across diverse asset classes, from commercial real estate and operating businesses to sophisticated listed securities portfolios, are increasingly seeking innovative financial strategies. This article delves into how cross collateralisation functions as a sophisticated tool, capable of either enhancing liquidity or concentrating risk, depending entirely on its meticulous engineering and the negotiation leverage applied.

What Is Cross Collateralisation in Private Credit?

At its core, cross collateralisation in private credit refers to a loan structure where one or more assets are pledged as security for multiple credit facilities, or where multiple assets are pooled together to secure a larger, single credit line.

Unlike a typical retail mortgage where one property secures one loan, private credit structures treat collateral as part of a broader capital architecture.

In institutional terms, cross collateralisation means treating a portfolio as a single security pool rather than as isolated assets.

Key structural components typically include:

- Multi-asset security pooling

- Dragnet clauses linking present and future obligations

- Cross-default provisions across facilities

- Blended loan-to-value assessment

- Portfolio-level underwriting rather than asset-level underwriting

Dragnet clauses within loan agreements often stipulate that all pledged assets secure all present and future obligations the borrower has with that lender. Cross-default provisions are frequently intertwined, meaning a default on one facility can trigger default across the entire secured structure.

The distinction between retail and private credit application is critical. In retail lending, cross collateralisation might involve using equity from a primary residence to secure a second mortgage. In private credit, it enables lenders to underwrite diversified asset pools, commercial real estate, private equity stakes, operating businesses and liquid securities, as one integrated credit proposition.

The result is a more holistic assessment of risk and borrowing capacity, shifting the focus from standalone valuations to the strength of the portfolio as a whole.

The Strategic Edge: Liquidity Without Immediate Disposal

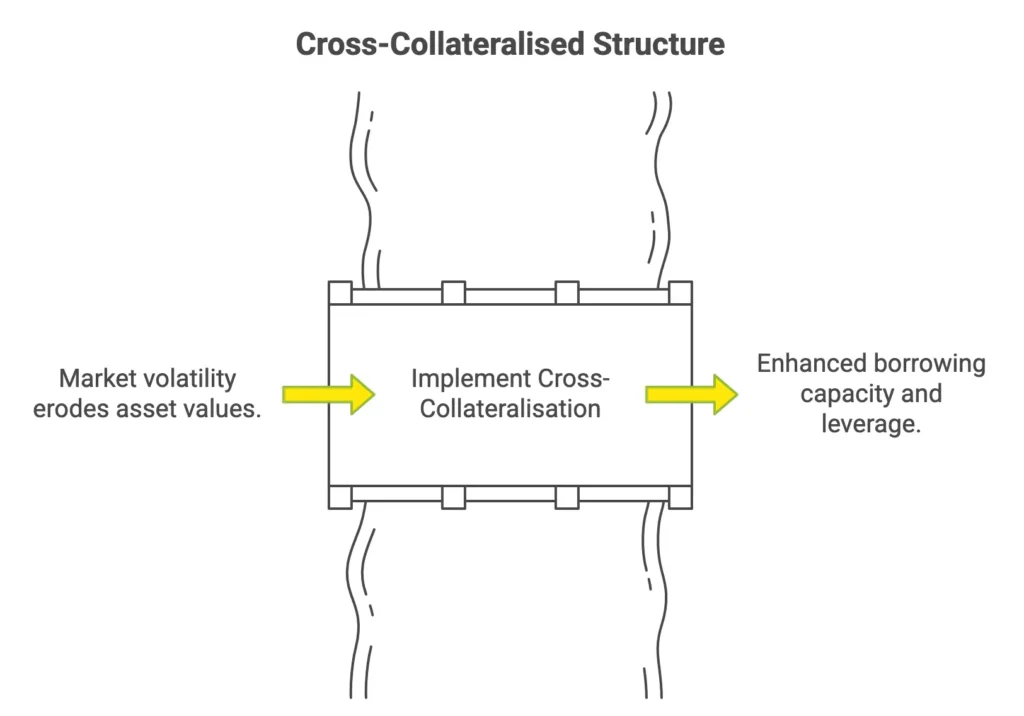

In an environment where market volatility can rapidly erode asset values and traditional financing avenues may prove restrictive, cross collateralisation offers a compelling strategic edge. For UHNWIs and family offices, the ability to access substantial liquidity without being forced into distressed sales of prized assets is invaluable.

This loan structure enhances the blended loan-to-value ratio across a portfolio. Instead of assessing individual assets in isolation, a private credit lender can view the combined value of multiple assets, potentially allowing for a higher overall credit facility than would be achievable through separate, standalone loans. This strengthens lender confidence, as the broader security package provides a more robust buffer against market fluctuations or specific asset underperformance. In 2026, many private credit lenders quietly prefer broader security pools, particularly where single-asset underwriting would otherwise constrain facility size.

Strategic advantages include:

- Enhanced borrowing capacity

- Reduced forced asset sales

- Consolidated refinancing

- Greater negotiation leverage

- Portfolio-level credit assessment

Consider a scenario where a borrower holds significant equity in a commercial real estate portfolio but also has substantial, illiquid holdings in a private operating business. By employing cross collateralisation, they can pledge both the real estate and a minority stake in the operating business to secure a single, larger credit facility. This avoids the need to sell part of the business or refinance individual properties at unfavourable terms, preserving long-term value and control.

As existing credit lines mature, the ability to consolidate multiple loans under one private credit lender, secured by a diversified asset pool, can streamline the refinancing process, reduce administrative burden and potentially secure more favourable loan terms. It supports complex family office capital structures by providing a flexible mechanism to manage intergenerational wealth transfer, fund new ventures or bridge temporary cash flow gaps without disrupting core investment strategies. The emphasis is on liquidity engineering and disciplined capital deployment, not deposit avoidance.

Real-World Scenarios: Structuring Nuance in Practice

To truly appreciate the power of cross collateralisation in private credit, examining real-world institutional examples is essential. These scenarios highlight the practical structuring nuance involved and the bespoke nature of private credit solutions.

Scenario 1: The Diversified Family Office Facility

A prominent family office holds a diverse portfolio comprising several income-generating commercial real estate properties, a significant stake in a successful tech start-up, and a liquid portfolio of listed equities. They require substantial capital for a new venture without divesting any core assets.

Instead of seeking separate loans for each asset class, a commercial mortgage for the properties, a venture debt facility for the start-up stake, and a securities-based loan for the equities, the family office approaches a private credit fund. The fund structures a single, multi-asset facility, cross-collateralised by the entire portfolio. This allows for a blended LTV ratio that reflects the combined strength and diversification of their holdings. The loan structure includes carefully negotiated partial release mechanics, allowing specific assets to be sold or refinanced in the future without triggering a default on the entire facility, provided certain loan-to-value covenants are maintained.

Scenario 2: Consolidating Business Debt for Refinancing Stability

A successful business owner has grown their enterprise through a series of acquisitions, resulting in multiple loans from various lenders, each secured by specific operating assets or subsidiaries. As refinancing risk looms in 2026, they seek to streamline their capital structure and reduce the complexity of their debt obligations.

A private credit lender steps in to consolidate these multiple loans into a single, larger facility. This new loan is secured by a cross-collateralisation agreement encompassing the entire operating business, including its various subsidiaries, intellectual property, and key revenue streams. This approach stabilises refinancing risk by moving from fragmented, short-term facilities to a more comprehensive, longer-term solution with a single counterparty. The lender benefits from a broader security package, while the borrower gains simplified repayment schedules and potentially more favourable overall loan terms. This consolidates counterparty risk and reduces refinancing uncertainty.

Scenario 3: Portfolio-Backed Facility with Negotiated Release Mechanics

An investor holds a portfolio of high-value luxury assets, including a superyacht, a private jet, and a collection of fine art. They wish to unlock liquidity against these assets to fund a new investment opportunity.

A specialist private credit provider structures a portfolio-backed facility where all three assets serve as eligible collateral for a single credit line. Crucially, the negotiation includes detailed release mechanics. For instance, if the investor decides to sell the superyacht, the agreement specifies the conditions under which that asset can be released from the security package, perhaps by repaying a pro-rata portion of the loan or substituting it with alternative collateral. This demonstrates how sophisticated cross collateralisation can be tailored to provide both robust security for the lender and essential flexibility for the borrower, allowing for active portfolio rebalancing without triggering punitive clauses.

These examples underscore that cross collateralisation is not a one-size-fits-all solution but a highly customisable financial strategy that, when expertly structured, can unlock significant borrowing power and provide critical liquidity for sophisticated borrowers.

Why it is Gaining Traction in 2026

The increasing prevalence of cross collateralisation in private credit in 2026 is not coincidental. It reflects a direct response to macroeconomic pressure, lender discipline and borrower demand for structural flexibility, themes also tracked in the Global Financial Stability Report.

Primary drivers in 2026 include:

- Valuation volatility

- Private credit expansion

- Bank balance sheet constraints

- Borrower demand for structural flexibility

Valuation volatility across asset classes has made traditional standalone asset-backed lending more restrictive. Lenders seek broader security packages to offset potential declines in individual asset values. A multi-asset structure provides a more diversified collateral pool and reduces underwriting concentration risk.

The continued expansion of private credit funds has created a more flexible lending environment. Unlike traditional banks, which remain constrained by regulatory capital treatment and internal exposure limits, private credit providers can structure bespoke facilities around complex asset combinations. This is particularly relevant where capital usage, asset concentration thresholds or balance sheet allocation would otherwise limit bank appetite.

At the same time, many banks continue to reduce balance sheet flexibility for complex structured transactions involving mixed asset classes. This has created space for private credit lenders to step in with tailored multi-asset facilities.

Borrowers are also more structurally aware. Presenting an entire portfolio as collateral can enhance negotiation leverage, improve loan-to-value outcomes and secure more adaptable terms than fragmented asset-level borrowing.

Together, these forces make cross collateralisation a structural feature of the 2026 liquidity cycle rather than a niche financing technique.

What to Consider: Risks and Structuring Discipline

While cross collateralisation in private credit offers clear advantages, it demands rigorous structuring discipline. Without precision in documentation and negotiation, a mechanism designed to enhance liquidity can instead concentrate risk.

Key structural risks include:

- Cross-default trigger exposure

- Blended LTV sensitivity

- Release clause rigidity

- Counterparty concentration

- Intercreditor complexity

- Enforcement reality

Cross-default trigger exposure

A default on any single obligation within a cross-collateralised structure can trigger default across all secured facilities. An issue in one asset or business segment can therefore place the entire portfolio at risk, even where other components remain stable. The precise scope of cross-default clauses must be understood before execution.

Blended LTV sensitivity

Blended loan-to-value ratios increase borrowing capacity, but they also increase sensitivity to valuation swings. A material decline in one major asset can weaken the overall ratio and lead to margin calls, partial repayments or additional collateral requirements. Stress testing across multiple market scenarios is essential.

Release clause rigidity

Release mechanics are often the difference between flexibility and restriction. If poorly drafted, assets may become effectively trapped within the security package. Clear conditions for partial release, including repayment thresholds, substitution rights and valuation methodology, must be negotiated in advance.

Counterparty concentration

While the lender benefits from diversified collateral, the borrower may become concentrated with a single counterparty. This can reduce refinancing flexibility and limit optionality if market conditions shift or lender appetite changes.

Intercreditor complexity

Where multiple lenders exist across a broader capital structure, priority and enforcement rights must be carefully mapped. Intercreditor arrangements determine who controls enforcement, asset sales and recovery distribution in a stress scenario.

Enforcement reality

In a downside case, the lender’s legal rights over the pooled security package become decisive. Borrowers must understand not only contractual language but also practical enforcement pathways and jurisdictional considerations.

Cross collateralisation is a powerful structural tool. Its effectiveness depends entirely on documentation precision, release design and trigger control. The structure must be engineered before capital is committed, not renegotiated after stress emerges.

Conclusion: Structure Determines Outcome

In 2026, cross collateralisation in private credit is not a technical footnote. It is a structural decision that shapes control, flexibility and downside exposure.

For UHNWIs, family offices and sophisticated borrowers, the distinction is simple. Properly engineered, cross collateralisation enhances liquidity, strengthens negotiation leverage and protects long-term portfolio integrity. Poorly structured capital, concentrates risk and restricts optionality at precisely the wrong moment.

Outcome is determined by documentation, release mechanics and trigger design. The value is not inherent. It is engineered.

Unlock Your Portfolio’s Potential

If you are evaluating a multi-asset facility, seeking to optimise your capital structure, or restructuring existing credit lines in 2026, a properly engineered security structure can materially alter your liquidity profile and borrowing capacity.

Borrowers considering cross-collateralised structures should assess documentation, release mechanics and trigger design carefully before committing to terms. If you are exploring a similar structure, you can make an enquiry here.