CRE Financing Guide: Matching Capital Source to Transaction Type

Banks’ share of UK commercial real estate lending fell from 40 per cent to 36 per cent last year, according to Bayes Business School data reported by Bloomberg. Debt funds alone have more than doubled their share to 31 per cent in five years. This CRE financing guide starts from that shift, because it has moved too far to ignore.

For what each financing type actually is and how lenders calculate the metrics behind it, see our Real Estate Finance Basics guide. For the sequential process of structuring and closing a transaction once the source is chosen, see Commercial Real Estate Financing: 9 Steps to Close. This guide sits before both: how to match the right capital source to the transaction in front of you, before either process starts.

Why the Matching Decision Has Got Harder

The split between bank and non-bank lending has moved fast. Post-crisis capital requirements and tightening regulatory scrutiny have pushed UK and European banks toward stabilised, simpler loan structures and away from transitional, bridge and development lending. That gap didn’t close. Debt funds and other private credit lenders filled it, closing in on banks as the largest source of UK commercial real estate debt, per the data above.

This isn’t a temporary dislocation a sponsor can wait out. It’s a structural change in who lends against what. A transitional logistics asset and a stabilised office building no longer compete for the same pool of senior lenders, and approaching the wrong pool costs weeks before the rejection even arrives. That mismatch is exactly what this CRE financing decision needs to get right before any process starts.

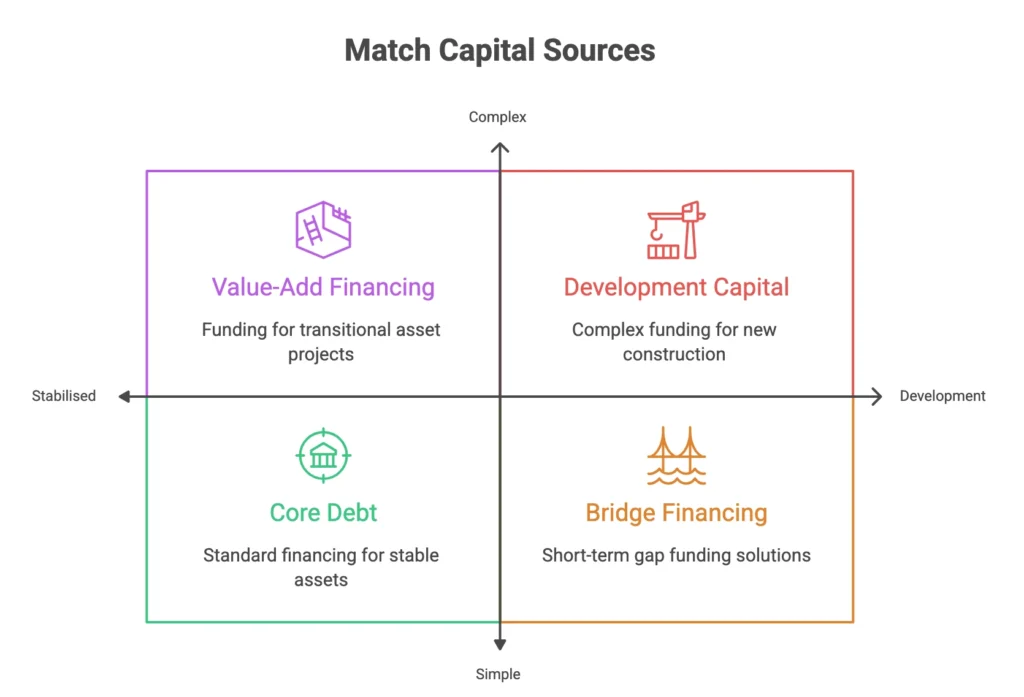

Matching Capital Source to Transaction Type

This CRE financing guide breaks that choice down by transaction type, not by financing label, since the label matters far less than what the deal actually needs.

Stabilised Acquisition or Refinance

In-place income, established occupancy, a clean rent roll. This is where bank and insurance company senior debt remains competitive, and where CMBS continues to provide scale. The asset’s job here is to look unremarkable.

Value-Add or Transitional Asset

Below-market occupancy or a repositioning plan in progress. Banks generally won’t underwrite the plan, only the in-place income. This is where debt funds and private credit lenders price off the credibility of the business plan rather than current cash flow, often layered with a mezzanine facility if the gap between senior proceeds and equity is still too wide. See our Mezzanine Financing in Real Estate guide for how that layer is structured and enforced.

Ground-Up Development

No income to underwrite at all. Construction debt covers the base, and the gap between that and the sponsor’s equity is typically closed with mezzanine debt or preferred equity, not a further equity call. Our Preferred Equity in Real Estate guide sets out when that route is faster to close than a mezzanine facility.

Time-Sensitive Acquisition or Refinancing Gap

A maturing loan that can’t be replaced at the same leverage, or a closing deadline a permanent lender can’t meet. This is bridge territory: short-term, priced on the credibility of the exit rather than current income. See Bridge Loan Commercial Real Estate for how that’s structured and priced.

A Pure Capital Stack Sizing Problem

Sometimes the asset is fine and the issue is simply that senior proceeds and sponsor equity don’t meet in the middle. That’s a mezzanine-versus-preferred-equity decision rather than a lender-type decision, and it sits one level below the choices above. Our Capital Stack Structuring guide covers how that layer is sized against the rest of the stack.

What Lenders Actually Scrutinise When Matching Capital to a Deal

The factors that decide which lender pool will actually engage are not the same as the factors a sponsor tends to lead with.

Data room quality travels across every lender type. A bank, a debt fund and a bridge lender are all assessing the same underlying question, whether the numbers and the plan hold up to scrutiny, even though they price and structure around it differently. A thin or inconsistent data pack costs a sponsor credibility with all three simultaneously, not just the one they’re currently talking to.

Asset and property type drive lender appetite before pricing does. Logistics, multifamily and healthcare currently attract the broadest pool of both bank and private credit appetite across the UK, European and Asia-Pacific markets. Office, retail and hospitality require a materially stronger in-place story before either pool engages seriously, regardless of the rate on offer.

Execution certainty is priced as carefully as the headline rate. A lender choosing between two otherwise comparable deals will favour the one with a signed term sheet on the exit, a credible refinancing plan, or a sponsor with a completed comparable scheme, because that certainty reduces the lender’s own downside exposure more than a marginally better DSCR does.

Being shopped to the wrong pool is visible and it costs more than time. Lenders within the same asset class talk, and a sponsor whose deal has clearly been declined elsewhere for fundamental reasons, rather than simply timed out, faces a steeper credibility climb with the next lender approached. Matching the source correctly the first time isn’t just efficiency, it protects the sponsor’s standing in the market they’ll need again.

Worked Example: Matching the Source to the Asset

A sponsor holds a logistics asset at 65 per cent occupancy, mid-way through a leasing programme that will take it to a stabilised income profile within 18 months. Three financing routes are on the table: wait and approach a bank once stabilised, accept a debt fund’s stretch senior loan now priced off the leasing plan, or take a smaller bank loan today and layer a mezzanine facility to bridge the remaining gap.

The bank route is cheapest on paper but assumes the leasing programme executes on schedule with no senior lender willing to fund the interim period. The debt fund route is faster and prices the plan directly, at a real cost premium for that flexibility. The blended senior-plus-mezzanine route preserves a lower blended rate on the senior piece but adds the intercreditor complexity covered in our mezzanine guide. None of the three is wrong. The choice depends on how much certainty the sponsor needs against how much the flexibility is worth, which is precisely the matching decision this guide exists to frame, not resolve in the abstract.

Conclusion

The widening gap between what UK and European banks will lend and what ambitious commercial real estate transactions actually need is not a temporary market condition. Choosing the right capital source for a specific transaction, before structuring it and before approaching a lender, has become as important to a successful close as the underwriting itself.

This CRE financing guide sits within our broader review of capital structuring in commercial real estate. For the process once a source is chosen, see our Commercial Real Estate Financing: 9 Steps to Close guide, the starting point for our Commercial Real Estate Finance Playbook.

If you are weighing which capital source actually fits your transaction, we welcome a discreet conversation. Contact us today