Real Estate Finance Basics 2025: Key Metrics & Loan Types

For property developers, commercial investors, and high-net-worth individuals, a strong grasp of real estate finance basics is not optional, it’s a competitive edge. Real estate has long been a foundational asset class for wealth preservation, income generation, and capital growth. But to unlock its full potential, investors must understand how capital flows in, how debt is structured, and how risk is managed.

In 2025, navigating this space means more than just comparing mortgage rates or negotiating terms. It’s about structuring deals with foresight, leveraging financing tools strategically, and using financial metrics to evaluate opportunity and risk in an increasingly complex market.

This guide lays out the core elements every investor should master, from the key lending metrics, to types of financing for various property strategies, and how to approach risk management in a volatile global environment.

What Real Estate Finance Basics Mean for Strategic Investors

At its core, real estate finance basics is the art of structuring capital around property, whether it’s an income-producing commercial building, a development site, or a diversified portfolio. It’s where investment meets lending, and where cash flow, leverage, and valuation intersect.

Understanding real estate finance allows you to:

- Evaluate the viability of new acquisitions

- Scale portfolios efficiently using leverage

- Select the right funding structures to match project timelines

- Navigate market cycles with a defensive strategy

In short, it’s the foundation of any serious real estate strategy, especially when deploying seven, eight, or nine figures into property assets.

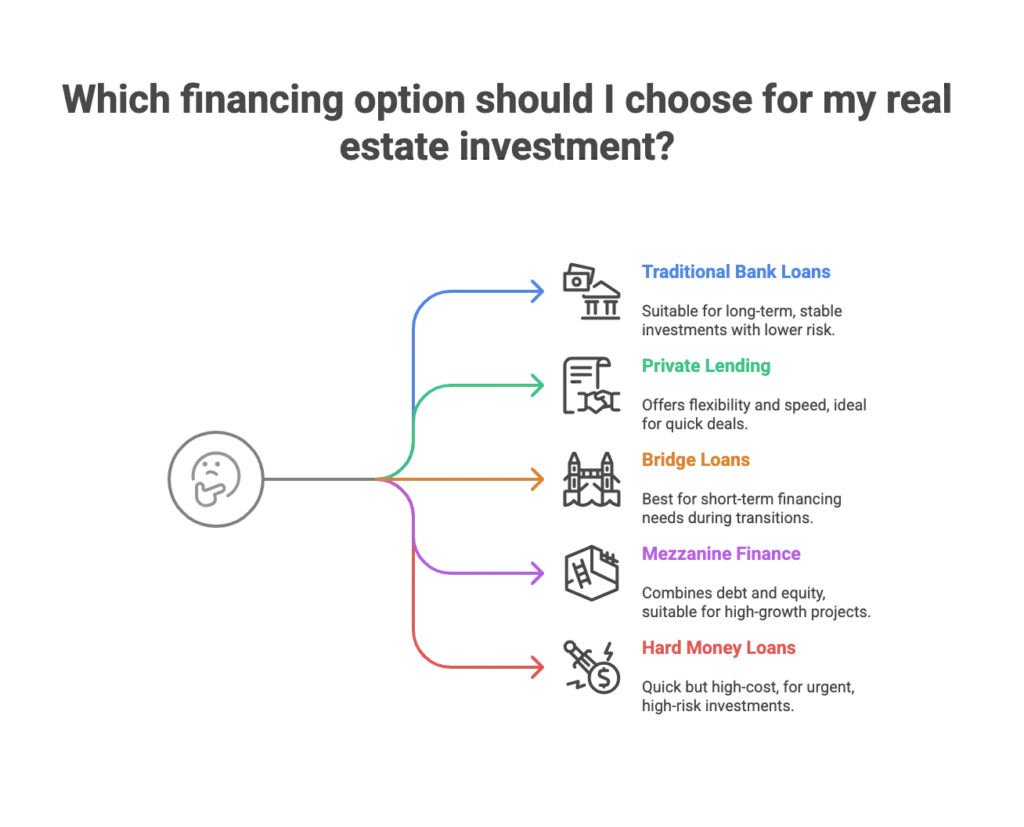

Financing Options: Beyond the Real Estate Finance Basics

While most people associate real estate finance basics with mortgages, serious investors tap into a broader toolkit. The right financing approach depends on asset type, timeline, liquidity needs, and risk appetite. Below is a breakdown of key funding structures relevant in 2025:

1. Traditional Bank Loans & Commercial Mortgages

These remain the backbone of real estate finance for stabilised, income-generating properties.

- Use case: Office buildings, industrial sites, multi-family housing with steady cash flow

- Structure: Fixed or variable rates, amortised terms, typically 3–10 years

- Requirements: Strong credit, income verification, property valuation, and sometimes personal guarantees

- Upside: Competitive interest rates and long-term stability

- Downside: Slower approval timelines and lower LTVs

2. Private Lending and Asset-Based Loans

Private lenders, including funds and family offices, offer flexible financing, particularly for assets that fall outside traditional lending criteria.

- Use case: Fast acquisitions, distressed assets, offshore borrowers, or niche real estate

- Upside: Speed, asset-backed structures, fewer hoops to jump through

- Downside: Higher cost of capital, often short-term

3. Bridge Loans

Used to cover short-term funding gaps — such as acquiring a new property while waiting to exit another.

- Use case: Interim solutions between buying and refinancing or selling

- Terms: 6–24 months, interest-only

- Upside: Maintains momentum; avoids forced sales

- Downside: Higher interest, exit fees

4. Mezzanine Finance

A hybrid of debt and equity that sits behind senior debt in the capital stack. Often used in development or large acquisitions.

- Use case: Filling equity gaps without diluting ownership

- Structure: May include equity kicker or profit-sharing

- Upside: Leverage without giving up full control

- Downside: Expensive and complex; may include covenants

5. Hard Money Loans

Short-term, asset-backed loans based on the property’s value rather than the borrower’s credit.

- Use case: Renovation projects, flips, or properties with valuation upside

- Terms: Often 6–18 months, interest-only

- Upside: Fast, flexible, no pre-sale required

- Downside: High rates, lender fees, and tight timelines

Alternative Investment Access: Pooled Real Estate Vehicle

Investors seeking real estate exposure without direct ownership may prefer pooled structures that offer liquidity and diversification.

Real Estate Investment Trusts (REITs)

- Structure: Public or private companies that own or finance real estate

- Upside: Liquidity, passive income, professional management

- Downside: Market correlation, lower control

Real Estate Crowdfunding

- Structure: Online platforms pooling investor capital for specific projects

- Upside: Access to deals with low entry thresholds

- Downside: Varies in quality, due diligence is crucial

These options are not for everyone, but they offer scalable exposure — especially when direct ownership isn’t feasible or desirable.

Commercial Real Estate Financing structures often play a key role here, particularly when tied to larger development or acquisition projects.

The Metrics That Matter – Real Estate Finance Basics

Financial due diligence on real estate assets requires a sharp eye on the numbers. Below are the most important performance and financing metrics in 2025:

Loan-to-Value Ratio (LTV)

- What it is: Loan amount ÷ Property value

- Why it matters: Indicates leverage and equity contribution

- Investor takeaway: Lower LTVs = safer positions and better rates. Higher LTVs may reduce liquidity in down markets.

Debt Service Coverage Ratio (DSCR)

- What it is: Net Operating Income ÷ Annual debt payments

- Healthy benchmark: DSCR of 1.25 or higher

- Why it matters: A primary underwriting metric for lenders; signals sustainability of cash flow

Net Operating Income (NOI)

- What it is: Income from the property minus operating expenses

- Why it matters: Core to determining value, loan size, and ROI

- Investor tip: Watch for hidden costs (vacancy rates, deferred maintenance) that eat into NOI

Cap Rate (Capitalization Rate)

- What it is: NOI ÷ Property purchase price

- Why it matters: Gauges return on investment and asset class risk

- 2025 trend: Cap rates have widened slightly due to global uncertainty and interest rate volatility

Interest Rates and Loan Terms

- Key considerations: Fixed vs. variable, prepayment penalties, amortization schedules

- Strategic insight: In high-rate environments, short-term fixed or floating structures may offer more flexibility

Managing Risk in a Real Estate Finance Basics Strategy

A robust finance strategy doesn’t just chase yield, it manages downside

1. Interest Rate Risk

Rates have been volatile, and debt service costs can quickly shift.

- Solution: Lock in fixed rates when favorable, or use interest rate caps in floating-rate loans

2. Liquidity Risk

Real estate isn’t as liquid as equities. Quick exits can be costly or impossible in downturns.

- Solution: Maintain buffer capital, lines of credit, or keep some exposure through liquid REITs

3. Regulatory and Tax Risk

Policy shifts can affect zoning, tax treatment, and loan structuring.

4. Geographic Concentration

Overexposure to one market magnifies local risk — whether economic, political, or environmental.

- Solution: Diversify regionally and by asset class

Regional Considerations in 2025

Different markets, different playbooks. Financing structures, tax laws, and underwriting criteria vary substantially by region.

- UK & Europe: Commercial real estate lending remains conservative; development finance is highly localised

- Asia-Pacific: Strong growth in mixed-use and urban renewal projects; access to offshore capital increasing

- Middle East & US: More structured equity participation models; credit tightening has created opportunities for private lenders

Working across regions? Local expertise is critical, from legal frameworks to borrower credibility standards.

Conclusion

Whether you’re acquiring a portfolio of stabilised commercial assets or funding a development pipeline, a solid command of real estate finance basics is non-negotiable in 2025.

Key metrics like DSCR, NOI, and LTV offer a lens into asset performance, while structured financing, from bridge loans to mezzanine finance, enables tailored strategies based on timing, risk, and return objectives.

The best investors don’t just buy property — they structure capital strategically, manage risk proactively, and leverage finance as a tool for long-term growth.

Ready to structure smarter real estate investments? Contact us today for tailored solutions that fit your investment goals across the UK, Europe & Asia-Pacific.

🧠 Want to hear others’ take on the blog post? Listen to this Deep Dive for the highlights.🎙️