Lombard Loan Case Studies: How HNW Investors Unlock Capital in 2025

Our Lombard loan case studies demonstrate how HNWIs, executives, and investors unlock liquidity without selling assets. Wealth is often tied up in long term investments that aren’t easily liquidated. Selling can trigger tax, disrupt strategy, and cut future returns. A Lombard loan keeps your portfolio intact while giving you access to fast capital.

A Lombard loan allows investors to borrow against listed securities such as shares, bonds, or funds, without disrupting your portfolio. It is a core tool in private banking, giving clients access to capital while keeping long term investments intact.

This collection of Lombard loan case studies focuses on real outcomes across the UK, EU, and APAC. Each example highlights how a tailored approach to Lombard lending meets specific client objectives, navigates complex underwriting, and delivers efficient results in practice..

Key Takeaways

- Unlock liquidity without selling core assets

- Use Lombard loans for bridge finance, tax planning, or growth

- Avoid capital gains and preserve portfolio structure

- Tailored underwriting unlocks better terms

- Execution can be completed in under 3 weeks

Understanding Lombard Lending: A Strategic Tool for Wealth Management

A Lombard loan, at its core, is a secured credit line or loan where the collateral is the borrower’s marketable securities or other liquid assets. Rather than using property as security, as with a mortgage, you leverage your investment portfolio

This form of financing is particularly advantageous for HNWIs for several key reasons:

- Speed and Efficiency: A Lombard loan can often be arranged swiftly, especially when dealing with an existing private bank that already holds the assets. This provides a critical advantage when opportunities require immediate capital.

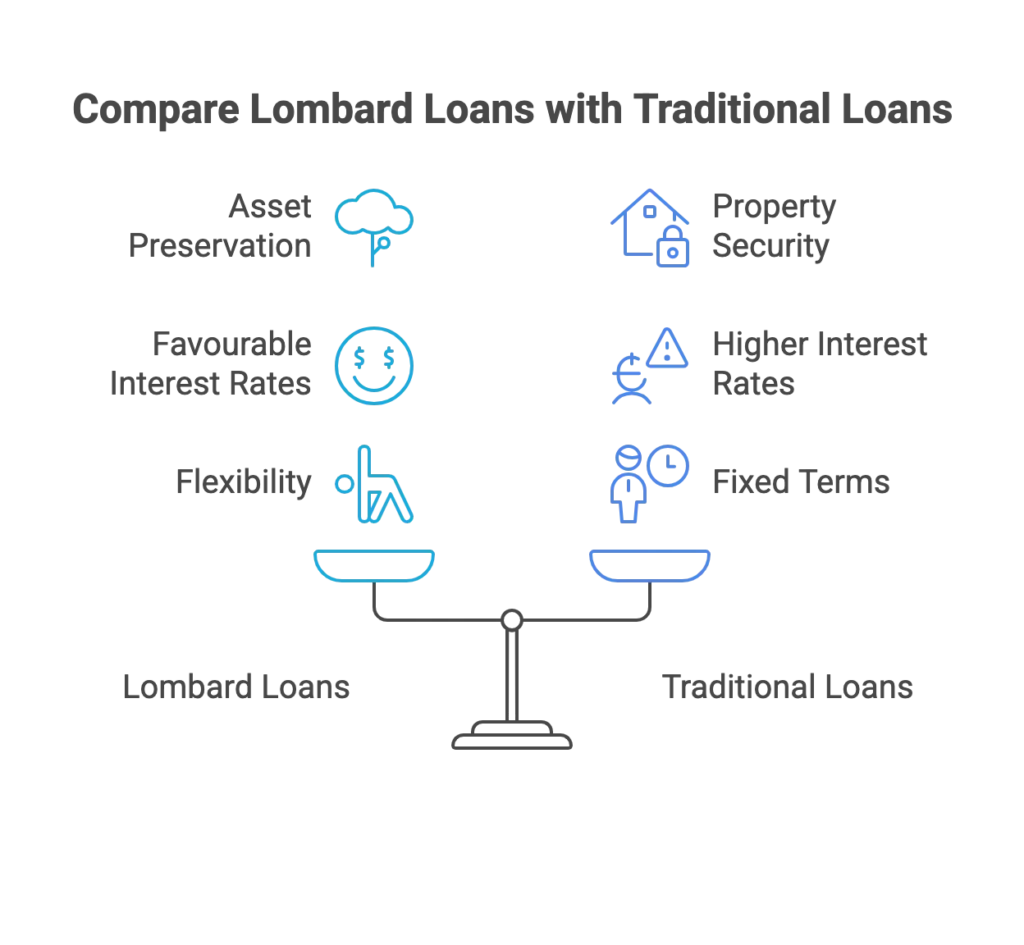

- Preservation of Assets: The primary benefit is accessing liquidity without selling your investments. This keeps your long term wealth strategy intact, allowing your portfolio to continue generating returns and appreciating in value.

- Favourable Interest Rates: Because the loan is secured by high quality, liquid collateral, lenders view it as a lower risk product. This often translates into comparatively favourable interest rates compared to unsecured borrowing.

- Flexibility: Lombard loans can be structured as a flexible credit line, allowing you to drawdown funds as needed, or as a lump sum term loan. Repayment terms can also be tailored, often with interest only options and a bullet repayment at the end of the term.

In the UK, Lombard lending is a well established market, regulated by the Financial Conduct Authority (FCA). Lenders and brokers must adhere to strict standards, ensuring a transparent and secure underwriting process for global clients and UK residents alike.

Lombard Loan Case Studies: From Theory to Practical Application

To truly understand the strategic power of Lombard financing, we must examine how it is applied. The following Lombard loan case studies illustrate how to arrange bespoke solutions for high net worth individuals with diverse objectives.

Case Study 1: The Entrepreneur Seizing a Private Equity Opportunity

Client Profile: A successful tech entrepreneur based in London with a significant personal investment portfolio valued at £15 million. The portfolio was well diversified, comprising blue-chip equities, corporate bonds, and several managed funds, all held with a single private bank.

The Objective: The client was presented with a time sensitive opportunity to participate in a £5 million private equity co-investment alongside their venture capital firm. Divesting from their existing portfolio to raise the capital would have incurred a substantial Capital Gains Tax liability and disrupted their long term investment allocation. They needed to secure the £5 million Lombard loan swiftly to meet the funding deadline.

The Challenge: While the client’s portfolio was substantial, a portion was held in less liquid, alternative funds. The initial offer from their private bank was based only on the most liquid stocks, falling short of the required amount and at a less favourable interest rate. The client needed a lender who could take a more holistic and bespoke approach to the valuation of their entire portfolio.

Our Solution and the Underwriting Process:

As a specialist broker, our role was to source a lender that could appreciate the full value and quality of the client’s assets.

- Portfolio Analysis: We conducted a deep dive into the entire £15 million portfolio, creating a detailed breakdown of each asset class, its liquidity profile, and historical performance.

- Lender Negotiation: We presented this comprehensive analysis to a panel of private banks and specialist lenders, including those known for their flexible underwriting. We successfully negotiated with a lender willing to offer a higher LTV by including a larger portion of the managed funds in their calculation.

- Structuring the Loan: We arranged a £5 million Lombard loan structured as a flexible credit line. This gave the client the ability to drawdown the funds exactly when needed for the private equity transaction. The loan was secured with a favourable interest rate, fixed for two years to provide certainty.

- Swift Execution: The entire process, from initial consultation to drawdown of funds, was completed in under three weeks, ensuring the client did not miss the investment deadline.

The Outcome: The client successfully made the private equity investment without selling a single share from their core portfolio. This allowed them to maximise their wealth by participating in a high growth opportunity while their existing assets continued to perform. The bespoke approach ensured they secured the full amount needed at a competitive rate.

Case Study 2: Financing a Prime UK Property Investment with a Lombard Bridge

Client Profile: A multinational executive residing in Singapore, looking to acquire a prime buy-to-let property in Kensington, London, for £3.5 million. The client had a significant investment portfolio of £10 million, held with an international private bank.

The Objective: The London property market is highly competitive. The client needed to act as a cash buyer to secure the property ahead of other bidders. A traditional mortgage application would be too slow and complex, given their non-resident status and multinational income streams. They required a short term financing solution to bridge the purchase.

The Challenge: Arranging financing for non-residents can be fraught with complexity. The client needed a lender that was comfortable with their international status and could move at the pace required for a prime property acquisition. The objective was to secure funds within a month.

Our Solution and the Underwriting Process:

A Lombard loan was the ideal instrument to act as a bridge.

- Collateral Leverage: We identified that their £10 million investment portfolio was the perfect collateral to secure the required financing swiftly.

- Lender Sourcing: We approached a private lender with a strong appetite for offering Lombard loans to global clients for UK property investment. Their underwriting process was specifically designed to handle complex financial profiles.

- Loan Structuring: We arranged a £3.5 million Lombard loan with a 12-month term. This gave the client the immediate liquidity to purchase the property. The loan-to-value (LTV) was set at a conservative 35% of their portfolio, providing a significant buffer against market volatility.

- Exit Strategy: The loan was structured with a clear exit plan. Once the purchase was complete, we began arranging a long term buy-to-let mortgage. The proceeds from the mortgage would be used for the full repayment of the Lombard loan.

The Outcome: The client secured the property, leveraging their investment portfolio to act as a cash buyer. The Lombard loan provided the speed and certainty that a conventional mortgage could not. Within six months, the long-term financing was in place, and the Lombard facility was closed. This demonstrates how Lombard loans are particularly advantageous as a form of bridge financing for strategic asset acquisition.

Case Study 3: A Pension Trustee Client Managing Liquidity and Tax Planning

Client Profile: The trustees of a UK based Self-Invested Personal Pension (SIPP), holding assets on behalf of a high-net-worth individual. The pension portfolio was valued at over £8 million and was managed for long term, stable growth.

The Objective: The HNWI, as the beneficiary, wished to make a significant lifetime gift to their children for a property purchase. However, drawing down a large sum from the pension would trigger significant income tax liabilities. The objective was to raise £1 million in liquidity for the gift without creating a taxable event.

The Challenge: Lending against a pension portfolio is highly specialised and subject to strict regulations. The structure had to be compliant and serve the best interests of the pension trustee client, not just the beneficiary. The solution required deep expertise in both Lombard lending and pension rules.

Our Solution and the Underwriting Process:

This complex financial situation required a highly personalised and compliant solution.

- Regulatory Compliance: We worked closely with the client’s tax advice and legal teams to ensure the proposed structure was fully compliant. The loan was made to the individual, secured against their personal investment portfolio held outside the pension.

- Bespoke Collateral Arrangement: The client had a separate personal portfolio of £4 million. We arranged a £1 million Lombard loan against this portfolio.

- Favourable Terms: Due to the high quality of the collateral and the low LTV (25%), we secured exceptionally favourable interest rates. The loan was structured with minimal repayment requirements during its term, preserving the client’s cash flow.

The Outcome: The client was able to gift the £1 million to their children without triggering a premature and costly drawdown from their pension. The Lombard loan provided the necessary liquidity while preserving the tax-efficient status of the pension wrapper. This case study highlights the role of Lombard lending in sophisticated, multi generational wealth planning.

Conclusion: Realise the Value – Join Our Lombard Loan Case Studies

Lombard loans are far more than a simple line of credit, they are a sophisticated instrument for strategic wealth management. As our Lombard loan case studies demonstrate, these facilities enable high net worth individuals in the UK, Europe and APAC to seize investment opportunities, access liquidity for property acquisitions, and implement efficient tax strategies, without disrupting their core investment holdings.

Success with Lombard lending hinges on a bespoke approach. It demands a clear understanding of each client’s financial goals, in-depth analysis of the pledged assets, and access to lenders who offer the flexibility and expertise to structure complex deals. By leveraging existing portfolios, investors can unlock significant capital, transforming static wealth into a dynamic vehicle for growth and diversification.

Take the Next Step

To explore how a Lombard loan could unlock the potential of your portfolio, contact our team at Forbes Le Brock for a confidential, no obligation consultation. Let’s determine whether your situation could become the next success story in our growing collection of Lombard loan case studies.

Get in touch now, unlock capital, stay invested, and join the clients already featured in our Lombard loan case studies.

🎙️ Prefer audio? Listed to a Deep Dive on Lombard Loan Case Studies for HNW Investors HERE🎧