Crypto Loans and Hedge Fund Liquidity Strategies in 2025

Crypto loans are no longer a niche workaround for digital asset holders. In 2026, they are becoming a structured liquidity tool for investors managing concentrated crypto exposure under tighter credit conditions.

For funds, treasury teams, and high-value holders of Bitcoin and Ethereum, the problem is straightforward: access liquidity without triggering disposal, tax events, or signalling weakness to the market.

This is where crypto loans sit. Not as speculation, but as a form of securities-based lending applied to digital assets, structured, collateralised, and increasingly institutional.

The question is no longer if crypto-backed lending works. It is whether it is structured correctly.

Understanding Crypto Loans: More Than Just Borrowing

At its core, crypto loans allow investors to borrow fiat or digital currency by pledging crypto assets as collateral. The concept mirrors securities-based lending and other forms of asset-backed finance: access liquidity without selling the underlying position. Where crypto differs is in execution, higher volatility, stricter collateral control, and more active loan-to-value management.

For institutional borrowers, two primary structures dominate.

Traditional Crypto-Backed Loans (Fixed-Term Structures)

This model closely resembles a stock loan. A borrower pledges a defined amount of crypto, typically Bitcoin or Ethereum, in exchange for a fixed loan amount in fiat. Terms are agreed upfront, including interest rate, duration, and loan-to-value ratio.

The LTV is set at origination, often around 30–50%, providing a buffer against volatility. The loan runs for a fixed period, typically two to three years, with interest accruing over the term and repayment due at maturity, although some structures allow periodic servicing.

This structure suits situations where capital needs are known in advance. Examples include funding private equity co-investments, acquiring real estate, or covering defined operational requirements, all while maintaining exposure to the underlying crypto position. Pricing is typically fixed, often in the 3–5% range depending on structure and counterparty.

Crypto Credit Lines (Flexible Facilities)

A more flexible alternative is the crypto-backed credit line. Here, the borrower establishes a borrowing limit against pledged assets and can draw down capital as required, rather than taking a fixed amount upfront.

The facility operates on a revolving basis. Borrowers can draw, repay, and redraw within agreed parameters, with interest charged only on utilised amounts. The LTV is continuously monitored, making active management essential to avoid margin calls.

This structure is better suited to short-term or tactical liquidity needs. It allows investors to respond quickly to market opportunities, manage cash flow, or hold liquidity in reserve during periods of volatility. The trade-off is cost and variability, with pricing typically floating, often at a spread over benchmark rates such as SOFR.

Both structures achieve the same objective: unlocking liquidity without forcing a sale. The difference lies in how that liquidity is accessed and managed. In all cases, control of the collateral remains central, with assets held either by the lender or through an approved custody arrangement for the duration of the facility.

The Strategic Edge: Why Hedge Funds Leverage Crypto Assets

For hedge funds and sophisticated investors, crypto loans are not simply a borrowing tool. They are a way to manage liquidity without disrupting portfolio construction, particularly where digital assets represent a core position.

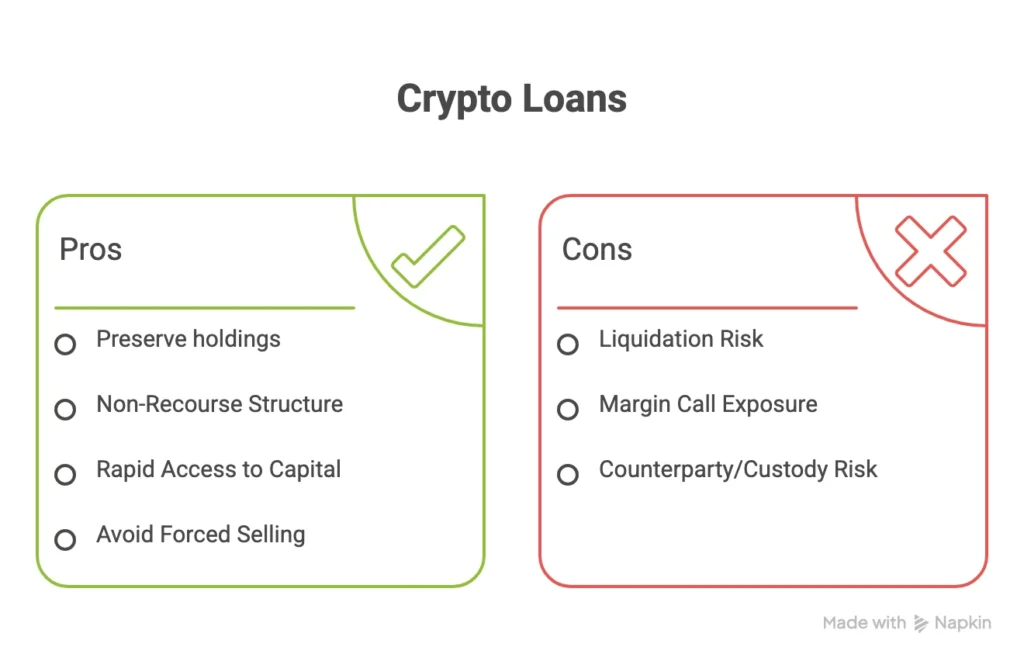

Preserve Crypto Holdings While Accessing Liquidity

The primary advantage is the ability to access capital without selling underlying holdings. Funds can unlock liquidity tied up in Bitcoin, Ethereum, or other digital assets while retaining exposure to future price appreciation. This allows them to maintain their investment thesis rather than compromise it for short-term cash needs or forced portfolio rebalancing

Non-Recourse Nature

Most crypto-backed loans are structured on a non-recourse basis, meaning the lender’s claim is limited to the pledged collateral. If loan-to-value thresholds are breached and margin calls are not met, the collateral may be liquidated, but the lender cannot pursue the rest of the portfolio. This creates defined downside risk contained within the structure.

Credit Lines Enable Faster Response to Market Events

In volatile markets, speed is critical. A pre-arranged crypto credit line allows funds to draw capital almost immediately, enabling execution of arbitrage strategies, hedging positions, or capturing short-lived opportunities without needing to unwind existing assets.

Avoid Forced Selling During Downturns or Illiquid Periods

Market stress creates pressure to sell into weakness. A crypto-backed facility provides an alternative, allowing funds to meet obligations, stabilise positions, or deploy capital opportunistically without forced liquidation.

Real-World Applications and Use Cases

To illustrate how crypto loans are applied in practice, consider the following scenarios.

Funding Private Equity Co-Investment

A hedge fund holds a substantial Bitcoin position. An attractive opportunity arises to co-invest in a private technology company, requiring £10 million within a short timeframe. Rather than selling BTC and triggering tax or losing upside exposure, the fund pledges a portion of its holdings as collateral for a fixed-term crypto-backed loan.

The capital is deployed into the investment, while the underlying crypto position remains intact. Repayment can be managed through future inflows or portfolio adjustments, allowing the fund to diversify without disrupting its core exposure.

Tactical Hedging or Arbitrage

A quantitative fund identifies a short-term arbitrage opportunity requiring £5 million in stablecoins. With significant Ethereum and USDC holdings, the fund draws on a pre-approved crypto credit line, accessing capital immediately without needing to liquidate positions.

The trade is executed, the facility is repaid shortly after, and interest is only incurred for the duration of use. This demonstrates the advantage of flexible, on-demand liquidity in fast-moving markets.

Navigating Market Volatility

During periods of sharp market correction, liquidity pressures can intensify as asset values decline and margin requirements increase. In this scenario, a fund may face redemption requests or margin calls on other positions.

Instead of selling core crypto holdings into a falling market, the fund draws on its crypto-backed facility. This provides immediate liquidity to meet obligations, stabilise the portfolio, or deploy capital opportunistically at lower valuations, all without forced liquidation.

These examples demonstrate how crypto loans function as a strategic liquidity tool, enabling funds to respond to market conditions while preserving long-term positionin

The Maturing Landscape: Why Crypto Loans Are Gaining Popularity Now

- More Sophisticated Lenders: Institutions now apply structured underwriting, active risk management, and disciplined LTV frameworks tailored to crypto volatility.

- Improving Regulatory Clarity: Key jurisdictions are defining clearer rules, increasing confidence in enforceability and collateral protection.

- Maturing Crypto Markets: Greater liquidity and depth reduce execution risk, supporting tighter spreads and more competitive pricing.

- Growing Demand for Alternative Lending: Traditional capital is entering the space, attracted by risk-adjusted returns when structures are properly controlled.

Lender Insight: What Actually Gets Approved

From a lender’s perspective, crypto loans are not about optimism on digital assets. They are about control, liquidity, and downside protection.

Three things drive approval:

- Asset quality and liquidity: BTC and ETH dominate for a reason. Depth, volatility profile, and exit certainty matter more than narrative.

- LTV discipline, not maximum leverage: Most institutional lenders will sit closer to 30–50% LTV, not because they are conservative, but because crypto volatility demands margin for error.

- Custody and enforceability: If the lender does not control the collateral directly (custodian or on-platform), the deal does not happen. Structure always overrides intent.

Where borrowers get this wrong is assuming crypto lending behaves like margin lending. It doesn’t. It behaves like private credit, with stricter collateral control and faster enforcement.

Key Considerations for Sophisticated Borrowers

While the benefits are clear, careful structuring and due diligence are essential.

- Volatility Risk: Crypto prices can move quickly, triggering margin calls. Maintain conservative LTVs and active monitoring to avoid liquidation.

- Loan Type: Fixed-term loans suit defined capital needs, while credit lines provide flexibility. Align structure with strategy.

- Lender Due Diligence: Assess counterparty strength, compliance, custody arrangements, and fee transparency.

- Legal Clarity: Ensure enforceability of collateral and loan terms across relevant jurisdictions.

- Tax Implications: Borrowing is typically non-taxable, but treatment varies. Professional advice is essential on regulatory clarity for digital assets.

Conclusion: The Strategic Liquidity Pla

Crypto loans have moved beyond niche structures into a practical liquidity tool for institutional investors. They allow capital access without forcing asset sales, preserving exposure while improving flexibility.

For borrowers who understand structure, LTV control, and counterparty risk, they provide a controlled way to navigate volatility and deploy capital efficiently.

Looking To Access Liquidity From Your Digital Assets?

Forbes Le Brock structures crypto-backed loans and credit lines for institutional investors and large holders.

→ Book a confidential discussion to explore suitable structures.