Crypto Loans Gain Traction with Hedge Funds in 2025 – Here’s Why:

In today’s volatile macroeconomic environment, sophisticated investors are seeking agile ways to unlock value without compromising long-term positions. For hedge funds, family offices, and institutional players active in digital assets, liquidity is key. This is why crypto loans are evolving from niche offerings into core financial tools.

With credit markets tightening and institutional adoption of assets like BTC and ETH rising, funds holding significant digital positions face a dilemma: stay liquid without selling, triggering tax events or missing future upside. Crypto backed loans and credit lines solve this by using digital assets as collateral to unlock capital.

This article explores the loan structures, advantages, and practical considerations that make crypto loans a strategic choice for high-level investors, not as speculation, but as a prudent lever in a hybrid market.

Understanding Crypto Loans: More Than Just Borrowing

At its core, crypto loans offer a loan facility that allows investors to borrow crypto or fiat currency by pledging digital assets as collateral. While the fundamental concept mirrors traditional a securities-based loan or luxury asset finance (using an asset you own to get a loan without selling it), the underlying mechanics and available structures in the digital asset space offer distinct advantages.

There are primarily two models gaining traction with institutional players:

- Traditional Crypto Backed Loans (The “Stock Loan” Model):

- Structure:This is akin to a fixed-term, fixed interest rate, fixed-amount loan. The borrower pledges a specific amount of crypto as collateral (e.g., Bitcoin, Ethereum, or other major cryptocurrencies) to receive a set loan amount in fiat (USD, GBP, EUR)

- Mechanics: The loan-to-value (LTV) ratio is agreed upon upfront (e.g., 50% LTV means you can borrow £50 for every £100 worth of crypto collateral). The loan term is fixed (e.g., 2-3 years), and fixed interest accrues over this period. Repayment typically occurs at the end of the term, though some structures allow for periodic interest payments.

- Use Case: Ideal for funding specific, known capital needs over a defined period, such as a private equity co-investment, a real estate acquisition (linking to commercial real estate finance principles of leveraging assets), or a significant operational expense, all without selling the underlying crypto holdings. Typical interest rates are fixed at 3-5%

- Crypto Credit Lines (Flexible Drawdown Facilities):

- Structure:More flexible than traditional loans, these function like a revolving credit facility. A maximum borrowing limit is established based on the pledged crypto collateral on account. The borrower can then draw down funds (in fiat) as needed, up to the limit. Interest is typically only paid on the drawn amount.

- Mechanics: An LTV is agreed upon, and the facility is evergreen or has a flexible term. The borrower has the flexibility to borrowing funds, repay, and borrow again within the agreed parameters. Managing the LTV is crucial to avoid a margin call.

- Use Case: Perfect for tactical liquidity needs, such as quickly capitalising on short-term market opportunities, hedging positions, managing cash flow fluctuations, or having a strategic reserve available to navigate periods of market stress. This offers the speed often associated with an instant crypto loan, providing cash without selling, however variable interest rates are far higher, typically SOFR + 4-5%.

Both models allow funds to leverage the value of your crypto assets, providing liquidity without the need for asset disposal. The collateral is held securely by the lender or a trusted third-party custodian or on account with the lender for the loan term.

The Strategic Edge: Why Hedge Funds Leverage Crypto Assets

For hedge funds and sophisticated investors, the appeal of crypto loans extends far beyond simple borrowing. They represent a strategic play offering several key advantages:

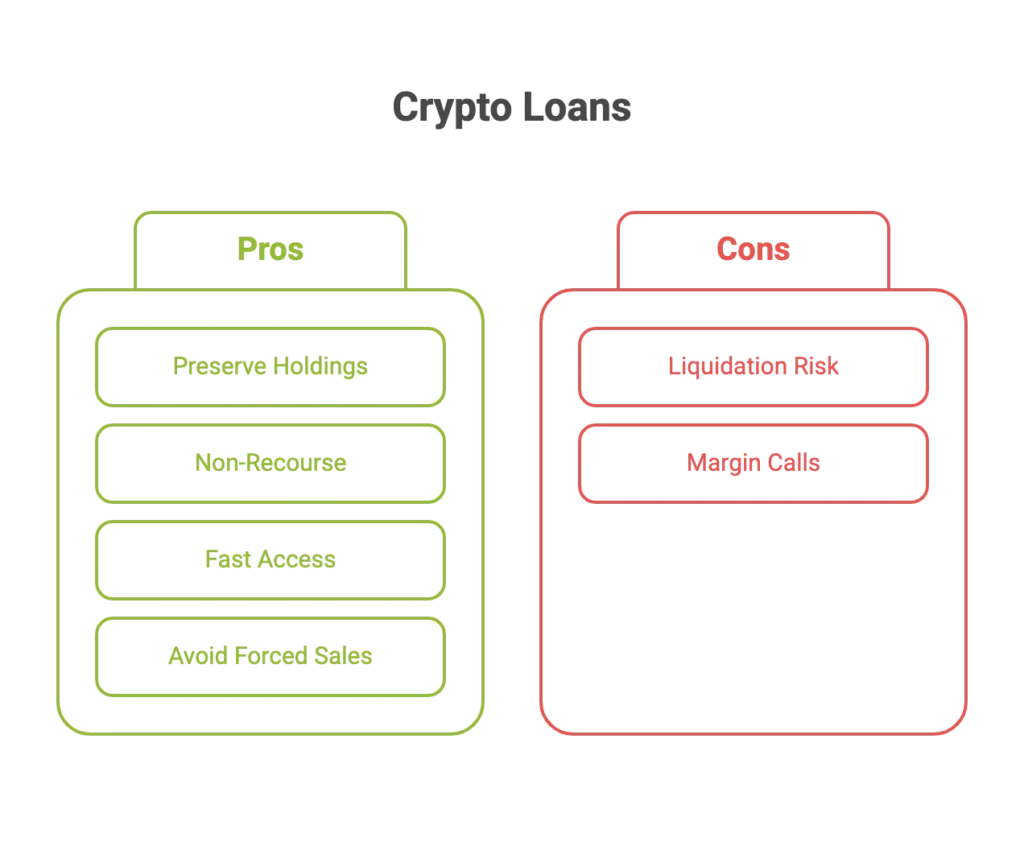

- Preserve Crypto Holdings While Accessing Liquidity: This is the primary driver. Funds can unlock the value tied up in their Bitcoin (BTC) and Ethereum (ETH) or other digital asset portfolios without selling them. This means they retain exposure to potential future price appreciation, aligning with their long-term investment thesis.

- Non-Recourse Nature: Typically, crypto backed loans are non-recourse to the fund’s other assets. The loan is secured only by the pledged crypto collateral. While the collateral can be liquidated if the LTV or loan-to-value ratio reaches a certain threshold and a margin call is not met, the lender cannot pursue the fund’s other assets to recover losses. This provides a layer of strategic downside protection for the broader portfolio.

- Credit Lines Enable Faster Response to Market Events: In fast-moving markets, speed is critical. A pre-arranged crypto credit line allows a fund to access capital almost instantly, enabling rapid deployment for arbitrage, hedging, or seizing fleeting opportunities that might disappear by the time assets could be sold. This is the essence of using crypto and get immediate access to funds.

- Avoid Forced Selling During Downturns or Illiquid Periods: Market downturns create a double bind: asset values fall while liquidity needs rise, whether to meet redemptions or cover margin calls. A cryptocurrency credit line or fixed loan offers a vital alternative, helping funds avoid forced sales at distressed prices. By using digital assets as collateral, capital is protected and positioned to benefit from a future recovery.

These advantages position crypto loans as a sophisticated tool for portfolio rebalancing and risk management, allowing funds to maintain their desired asset allocation while accessing necessary capital.

Real-World Crypto Loans Applications and Use Cases

To illustrate the practical application, consider these scenarios:

- Funding Private Equity Co-investment:A hedge fund holds a substantial amount of Bitcoin. An attractive opportunity arises to co-invest in a promising private technology company, requiring £10 million in cash within 30 days. Instead of selling their BTC (triggering capital gains tax and losing future upside exposure), the fund pledges a portion of their Bitcoin as collateral for a fixed-term crypto-backed loan in US Dollar or GBP. They receive the £10 million, make the investment, and plan to repay the loan using future fund inflows or by strategically managing their crypto holdings later. This is a classic example of using your crypto to get a loan for diversification or expansion.

- Tactical Hedging or Arbitrage:A quantitative fund identifies a short-term arbitrage opportunity requiring £5 million in stablecoins for execution. They hold significant Ethereum and USDC. They utilise a pre-approved crypto credit line, drawing down the required stablecoins against their ETH and USDC collateral. They execute the trade, repay the drawn amount quickly, and only pay back interest for the few days the funds were used. This showcases the power of a flexible borrowing facility.

- Navigating Market Volatility (Scenario: March 2024 Selloff): During a sharp, unexpected market correction in cryptocurrencies, a fund might face margin calls on other leveraged positions or anticipate increased redemption requests. Instead of being forced to sell their core crypto holdings into a falling market, they draw on their crypto credit line. This provides the necessary fiat or crypto liquidity to meet obligations, stabilise the portfolio, or even opportunistically buy assets at depressed prices, all without selling their primary collateral assets. This highlights how crypto loans can act as a vital safety net.

These examples demonstrate how crypto loans provide strategic flexibility, enabling funds to act decisively in various market conditions while preserving their core investment strategy.

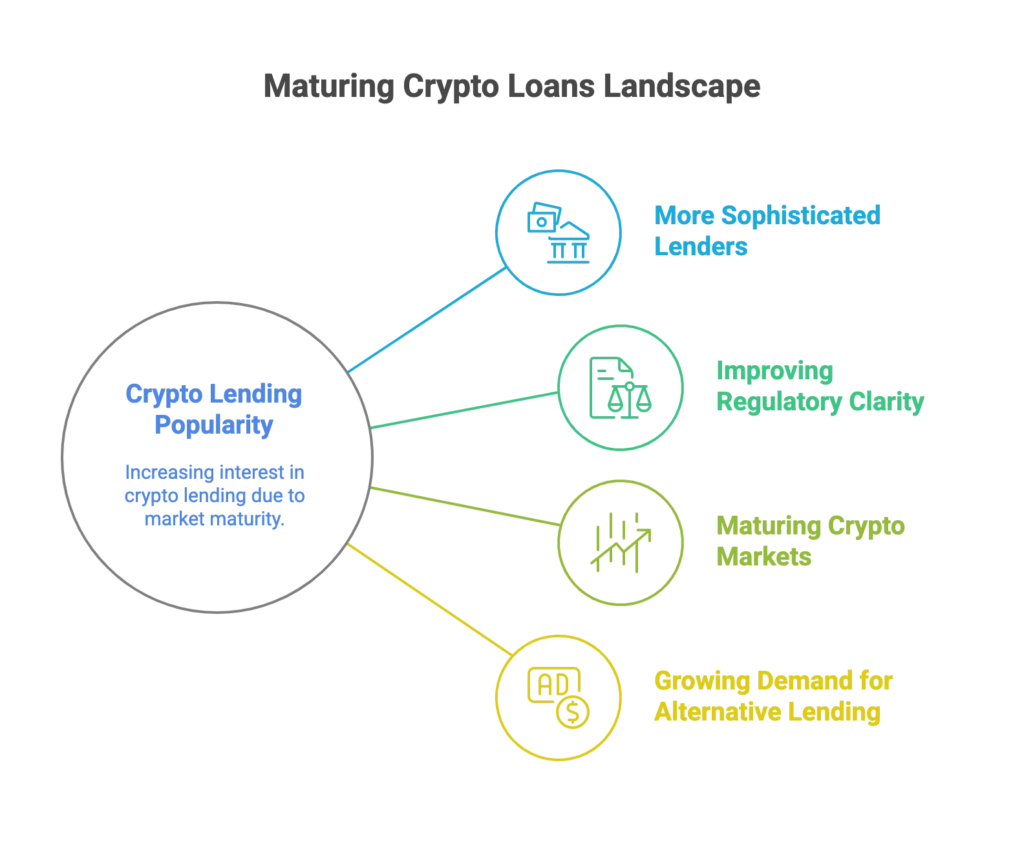

The Maturing Landscape: Why Crypto Loans Are Gaining Popularity Now

- More Sophisticated Lenders: Established institutions and crypto-focused lenders now have solid underwriting, risk management, and LTV/margin call systems tailored to volatile crypto assets.

- Improving Regulatory Clarity: Key markets are defining clearer rules around digital asset lending, boosting confidence in loan enforceability and collateral security.

- Maturing Crypto Markets: Better liquidity and market depth lower execution risk for lenders, resulting in tighter spreads and more competitive rates.

- Growing Demand for Alternative Lending: Traditional lenders seek yield in crypto backed loans, attracted by the risk-adjusted returns when loans are structured carefully.

This confluence of factors has made crypto loans more accessible, reliable, and strategically viable for institutional-grade borrowers.

Key Considerations for Sophisticated Borrowers

While the benefits are clear, prudent due diligence and careful structuring are essential when engaging with crypto loans. High-level decision-makers must consider:

- Volatility Risk: Crypto prices can drop fast, triggering margin calls. Keep LTV low, monitor closely, and be ready to add collateral or repay to avoid liquidation.

- Loan Type: Fixed loans suit long-term needs; credit lines offer short-term flexibility. Pick what fits your strategy.

- Lender Due Diligence: Vet lenders carefully. Check financial health, compliance, security, experience, and fee transparency.

- Legal Clarity: Use legal experts to ensure loan agreements and collateral claims hold up across jurisdictions.

- Tax Implications: Borrowing usually isn’t taxable, but rules vary. Get tax advice to understand your position.

By carefully considering these factors and working with experienced counterparties, funds can effectively mitigate risks and harness the power of crypto loans.

Conclusion: The Strategic Liquidity Play

Crypto backed loans have evolved from simple borrowing tools into sophisticated instruments for hedge funds and institutional investors managing liquidity. They allow funds to access capital without selling digital assets, supporting diversification, tactical moves, and navigating market swings.

For savvy investors, understanding loan structures, managing LTV, and conducting thorough lender due diligence is crucial. These loans protect against forced sales while enabling smart capital deployment. As digital assets continue integrating with traditional finance, crypto backed loans will become a core part of institutional strategy.

Looking To Access Liquidity From Your Digital Assets, Discreetly?

Forbes Le Brock structures crypto backed loans and credit lines for hedge funds, institutional investors, and clients worldwide.

→ Book a confidential consultation to explore options tailored to your portfolio and risk profile.

🎙️ Prefer an audio summary? Check out the Deep Dive discussion for more insights into the blog post’s content. 🎧