Lombard Loans: Understanding The Mechanics

A Lombard loan is not simply a loan against a portfolio. It’s a specific private banking instrument with its own pricing logic, collateral treatment and lender expectations, and the distinction matters when you are negotiating terms.

For UHNW borrowers and family offices already familiar with securities-based lending, the question is not whether a Lombard facility works. It is how to ensure the structure reflects your interests rather than your lender’s default template. The terms on offer vary significantly between private banks and non-bank lenders, and the difference between a well-structured facility and a poorly negotiated one can be material.

If you are new to Lombard lending, the securities-based lending guide covers the fundamentals. This post focuses on how Lombard loans are specifically structured, priced and negotiated in practice.

Strategic Benefits of Using Lombard Loans

Strategic Benefits of a Lombard Facility

- Remain invested: Access liquidity without triggering a sale, preserving your portfolio strategy and avoiding an unnecessary capital gains event.

- Fast drawdown: Typically days rather than weeks, unlike traditional secured borrowing.

- Non-recourse structure: In most facilities the lender’s claim is limited to the pledged securities, protecting other assets.

- Unrestricted use of funds: Capital can be deployed for new investments, property acquisition, business needs or personal liquidity.

- Negotiable pricing: Rates are linked to benchmark rates plus a margin, reflecting facility size, duration and asset quality. There is meaningful room to negotiate if you understand how lenders assess those factors.

Key Features of Lombard Loans

- Eligible collateral: Listed equities, bonds, mutual funds and other marketable securities, monitored continuously against the agreed LTV threshold.

- Loan-to-Value (LTV): The percentage of collateral value the lender will advance, varying by asset class, liquidity and concentration.

- Interest rates: Variable, tied to benchmark base rates plus a margin. Lombard loan interest rates reflect facility quality and duration.

- Loan terms: Flexible, from short-term revolving facilities to longer committed arrangements with tailored repayment structures.

- Margin calls: If collateral value falls below the LTV threshold, the lender may require additional assets or partial repayment. Failure to comply gives the lender the right to realise the pledged securities.

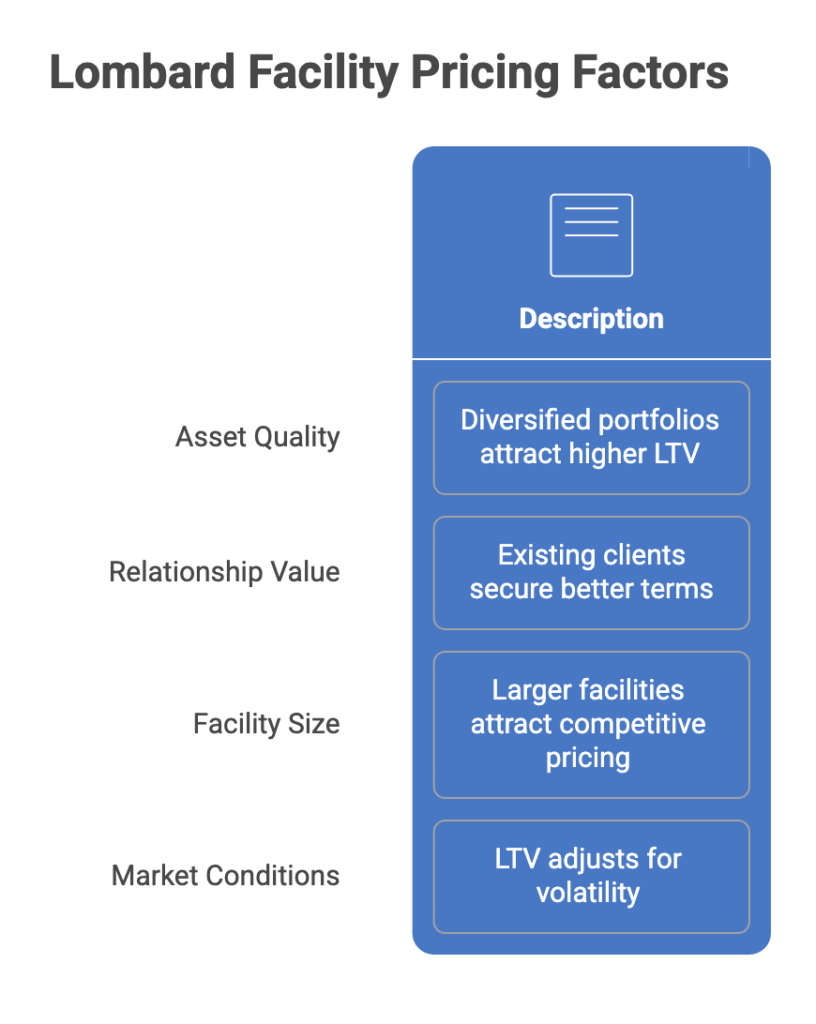

How Lenders Actually Assess and Price a Lombard Facility

Private banks and specialist lenders do not price Lombard loans on portfolio value alone. The assessment typically covers four factors that borrowers rarely see discussed explicitly.

Asset quality and liquidity

Lenders apply a concentration discount to portfolios heavily weighted towards a single stock, sector or geography. A diversified portfolio of blue chip equities will attract a significantly higher LTV than a concentrated position in a single listed company, regardless of the headline portfolio value. Where a borrower holds illiquid or thinly traded securities, lenders may exclude those positions from the eligible collateral pool entirely or apply a steep haircut. The composition of the portfolio, not just its value, determines the facility ceiling.

Borrower relationship value

Private banks price Lombard loans partly on the depth of the overall client relationship. A borrower with custody assets, advisory mandates or other products with the same institution will typically access better LTV ratios and tighter margins than a standalone borrower presenting a single transaction. For borrowers approaching a lender for the first time, understanding this dynamic is important. Non-bank private credit lenders tend to be more transactional in their pricing, which can work in the borrower’s favour where the relationship premium at a private bank does not offset the rate differential.

Facility size and duration

Larger facilities and longer committed terms generally attract more competitive pricing. A committed three-year facility of material size will be priced more favourably than a short-term revolving line drawn opportunistically. Short-term facilities carry a premium that reflects both the lender’s operational cost and the uncertainty around drawdown timing. Borrowers who can demonstrate a clear, longer-dated liquidity need are in a stronger position to negotiate on margin.

Market conditions at drawdown

LTV ratios are not fixed. Lenders reserve the right to adjust them in response to market volatility, and many do so without prior notice beyond what is specified in the facility agreement. Borrowers who negotiate LTV floors at the term sheet stage have materially better downside protection than those who accept standard documentation. In volatile markets, an unprotected LTV can compress rapidly, triggering margin calls on a facility that appeared conservatively structured at inception. Negotiating a floor, even a modest one, changes the risk profile significantly.

Understanding these four factors before approaching a lender puts the borrower in a significantly stronger negotiating position.

Strategic Applications for Lombard Loans

Beyond portfolio preservation, lombard loans are deployed across a range of capital needs: new investment opportunities, business acquisitions, property finance, and short-term cash flow management. The facility structure adapts to the purpose, revolving lines suit opportunistic deployment, while committed term facilities work better for longer-dated needs such as development finance or acquisition funding.

For borrowers considering a loan against an investment portfolio more broadly, the Lombard structure offers distinct advantages in speed and flexibility that standard portfolio lending does not always provide.

Lombard Loans: Risks and Considerations

The primary risk is market volatility. A significant downturn can reduce collateral value, triggering a margin call that requires additional assets or partial repayment. Borrowers should stress test their position before drawdown and ensure the agreed LTV provides sufficient buffer against realistic market movements.

Documentation is the second risk. Standard lender templates favour the lender. Margin call thresholds, LTV floors and enforcement rights should be reviewed and negotiated before signing, not after stress emerges. The Financial Conduct Authority provides guidance on borrower protections relevant to secured lending arrangements in the UK.

For borrowers with concentrated equity positions, the interaction between collateral concentration and LTV is particularly important. The risks specific to that structure are covered in stock loans for concentrated shareholders.

For a broader understanding of how loan to value ratio is applied across private credit structures, see the linked post in the Borrower Trust and Due Diligence Playbook.

Conclusion

A Lombard loan is only as effective as the terms behind it. LTV ratios, margin call thresholds and enforcement rights vary significantly between lenders, and the difference between a well-negotiated facility and a standard template can be material in a volatile market.

Borrowers who understand how lenders assess and price these facilities before approaching the market are in a fundamentally stronger position. The four factors covered above, asset quality, relationship value, facility size and market conditions, are the levers that determine the terms on offer.

If you are evaluating a Lombard loan structure and want to ensure the terms reflect your interests, we welcome a discreet conversation. Contact Us

For a more structured breakdown of how Lombard loans fit within a broader securities-based lending strategy, see the Securities-Based Lending Playbook.