Special Situations Finance 2026: Tension Before Collapse

Many companies and large shareholders operate under a comfortable illusion. Liquidity appears adequate. Covenants are intact. Banking relationships feel stable. The capital stack looks manageable.

In 2026, that perception can be dangerously misleading.

Refinancing windows narrow quickly. Credit committees tighten without warning. Sector limits shift. Risk appetites recalibrate. What looked stable twelve months ago can become constrained almost overnight.

It is in this widening grey zone, between apparent comfort and genuine stress, that special situations finance has evolved from a rescue tool into a strategic instrument. Structured capital is no longer deployed only after distress has set in. It is increasingly used before pressure escalates, when optionality still exists and negotiating leverage remains intact.

The distinction is critical. Timing determines control.

What Exactly Is Special Situations Finance?

Special situations finance is often misunderstood. It is frequently associated with distressed debt funds circling failing companies or last-minute rescue capital in bankruptcy courts. That interpretation is incomplete.

At its core, special situations finance is bespoke structured capital deployed during a typical, transitional, or event-driven moments in a company’s lifecycle or capital structure. These moments may involve:

- Refinancing pressure

- Shareholder liquidity constraints

- Covenant stress

- Acquisition opportunities

- Litigation exposure

- Spin-offs

- Complex restructurings

Importantly, special situations finance is not inherently distressed capital. Its most powerful application is preventive.

It can include:

- Mezzanine capital positioned between senior debt and equity, often with warrants or participation rights

- Hybrid instruments blending debt characteristics with equity upside

- Structured debt incorporating equity-linked features

- Asset-backed facilities secured against specific illiquid holdings

- Bridge-to-exit financing aligned to IPO, M&A, recapitalisation, or asset sales

The defining characteristic is structural adaptability. Traditional banks rely on standardised products and rigid underwriting templates. Special situations capital is structured around complexity, not around product categories.

That flexibility becomes decisive when markets shift.

The Unique Advantage in 2026

The macro backdrop has fundamentally altered the financing environment.

Higher rates remain embedded across developed markets. The refinancing cost of legacy debt has risen materially. Maturity walls are clustering over the next several years, creating compression in refinancing timelines. Traditional banks are slower, more compliance-driven, and more conservative in capital allocation. Internal capital charges and regulatory constraints reduce their appetite for bespoke or event-driven structures.

Meanwhile, private credit has matured. Institutional capital pools backing private credit strategies have expanded significantly. Dedicated special situations funds now operate with institutional scale and underwriting sophistication.

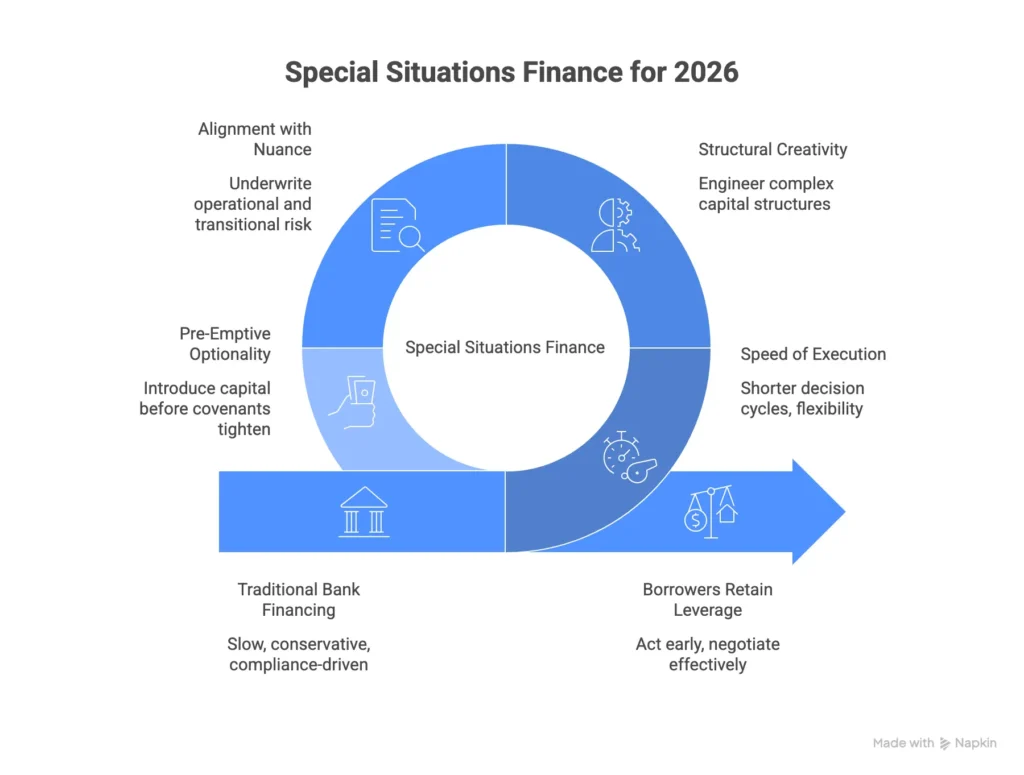

Within this environment, special situations finance offers four structural advantages:

1. Speed of Execution

Decision cycles are materially shorter. Investment committees are typically aligned around mandate-driven flexibility rather than balance sheet protection.

2. Structural Creativity

Complex intercreditor dynamics, layered capital stacks, and hybrid structures can be engineered rather than avoided.

3. Alignment with Nuance

Specialist capital providers are prepared to underwrite operational detail, transitional risk, and event-driven complexity.

4. Pre-emptive Optionality

Capital can be introduced before covenants tighten or refinancing windows close.

The difference is not cosmetic. It is structural. Borrowers retain negotiating leverage when they act early. They lose it when they wait.

Three Scenarios Where Timing Wins

Scenario 1: Pre-Refinancing Stabilisation

A mid-market industrial company faces a significant maturity in eighteen months. Performance is stable, but broader credit markets are selective. Traditional refinancing discussions begin, but lenders are cautious. Terms are conservative. Flexibility is limited.

Rather than wait for the maturity to compress negotiating leverage, management introduces structured special situations capital.

The facility extends runway, partially refinances existing exposure, and reduces short-term refinancing pressure. The company preserves strategic flexibility and maintains negotiating strength for the eventual refinancing.

The outcome is stability without distress. Equity value is protected because action was taken before urgency dictated terms.

Scenario 2: Shareholder Liquidity Constraint

A family office holds a concentrated, illiquid equity stake. External portfolio pressures create a temporary liquidity need. A forced sale would undermine long-term positioning and signal weakness.

Traditional lenders offer recourse-backed facilities tied to broader balance sheet exposure.

A specialist special situations provider structures non-recourse financing ring-fenced to the specific asset. The facility provides liquidity without contaminating unrelated holdings. Exposure is isolated. Estate risk is contained.

The asset is retained. Optionality is preserved. Liquidity is secured without strategic compromise.

Scenario 3: Event-Driven Opportunity

A corporate identifies a distressed competitor available at an attractive valuation. Traditional banks hesitate. Internal risk models flag the target’s financial stress. Credit committees slow execution.

A special situations provider underwrites the opportunity as an event-driven structure, bridging the acquisition with capital aligned to an integration and stabilisation plan. Longer-term refinancing can follow once performance normalises.

The acquisition proceeds. Market share expands. Strategic positioning strengthens.

In each case, the defining advantage is timing plus structural flexibility.

Why Special Situations Finance is Gaining Ground

The expansion of special situations finance reflects structural evolution in global capital markets.

- Traditional credit markets remain selective. Complexity is often avoided rather than analysed.

- Regulatory capital frameworks constrain bank balance sheets. Certain asset classes carry heavier capital charges. Risk appetite is shaped by policy, not by opportunity.

- Volatility compresses reaction time. Market dislocations create both risk and opportunity within short windows.

- Private capital pools are deeper than at any prior period. Pension funds, insurance capital, family offices, and institutional allocators increasingly back private credit and event-driven strategies.

Investors in this space are drawn to structured downside protection combined with equity-like participation. They seek asymmetric return profiles aligned to identifiable corporate events.

The result is institutionalisation. Special situations finance has moved from niche to mainstream within private capital markets.

What to Consider Before Engaging

Structured capital is powerful. It is also complex. Precision matters.

Cost Versus Control

Structured capital often carries a premium relative to conventional debt. That premium reflects flexibility, speed, and risk isolation. The evaluation should focus on total strategic value, not headline pricing alone.

Equity Participation

Hybrid structures may include warrants or conversion features. Dilution implications must be understood and negotiated carefully.

Intercreditor Alignment

Introducing new capital into an existing structure requires rigorous documentation and priority clarity. Poorly structured intercreditor dynamics can create future friction.

Exit Clarity

A defined repayment or refinancing pathway must exist. Structured capital is most effective when integrated within a broader strategic roadmap.

Covenant Design

Flexibility should be explicit, not assumed. Trigger thresholds and discretionary elements require careful review.

The optimal time to engage structured capital is before negotiating power deteriorates. Once distress is visible, pricing shifts and optionality narrows.

Conclusion: Before Distress, Not After

The historic narrative framed special situations finance as reactive. That framing is outdated.

In 2026, it is increasingly proactive capital deployed to stabilise balance sheets, protect equity, and preserve control before pressure escalates.

Those who move early define structure. Those who wait accept structure.

In volatile markets, timing determines leverage. Structured capital deployed before distress protects autonomy when it matters most.

Special situations finance is not about desperation. It is about strategic anticipation.

Call to Action

If refinancing timelines are approaching, shareholder liquidity pressures are emerging, or event-driven opportunities require decisive capital, structured special situations finance may provide clarity before markets tighten further.

Confidential discussions are available for complex or time-sensitive situations