Liquidity Risk in Lending 2026: How Maturity Mismatch Is Reshaping Credit Pricing

In the sophisticated corridors of private credit, structured finance, and family office principal investing, the year 2026 has ushered in a profound realisation: the era of cheap, ubiquitous refinancing is over. While the global economy has adjusted to a higher-for-longer interest rate environment, a more insidious challenge has emerged for high-net-worth individuals (HNWIs) and institutional sponsors.

The primary threat to capital preservation and portfolio stability is no longer just credit risk or simple over-leverage. It is liquidity risk in lending.

The distinction between solvency and liquidity has become decisive. Most lending failures in 2026 are not failures of asset value, but failures of timing. Liquidity, not leverage, now determines pricing and approval outcomes.

Defining Liquidity Risk in Lending: The Misunderstood Risk

In an institutional context, liquidity risk in lending is the risk that a counterparty, or the lender itself, cannot meet its financial obligations as they fall due without incurring unacceptable losses. For the borrower, it is the inability to access capital to settle a debt or roll over a facility. For the lender, it is the risk that funding disappears before an asset can be realised at its intrinsic value.

To understand the current market, we must bifurcate this risk into two distinct categories:

Funding Liquidity Risk

Funding liquidity risk refers to the ease with which a borrower or institution can obtain the necessary cash to meet its obligations. In 2026, this is less about the “run on the bank” narratives of the past and more about the “refinancing wall.” It is the risk that, despite having a high-quality balance sheet, the specific funding sources required to bridge a maturity simply evaporate or become prohibitively expensive.

Market Liquidity Risk

Market liquidity risk is the inability to exit a position or sell an asset quickly at a transparent price. Even if an asset, be it a prime commercial estate in Mayfair or a portfolio of private equity interests, is objectively valuable, a thin transactional market creates a liquidity shortfall. If you cannot sell the asset to repay the lender, the liquidity position of the entire structure collapses, regardless of the equity cushion.

Why Liquidity is Not Leverage

The most common mistake made by sophisticated borrowers is conflating leverage with liquidity. Leverage is a static snapshot of a balance sheet, a ratio of debt to value. Liquidity is a dynamic measure of cash flow and market access.

A low LTV is no longer a guarantee of resilience. Assets with substantial equity cushions are still defaulting because equity does not generate cash, and markets do not clear on schedule. Leverage measures what you owe; liquidity determines whether you can refinance, amortise, or exit before maturity forces a decision. When the time required to realise value exceeds the time allowed by the capital structure, the problem is liquidity, not leverage.Lenders have shifted their focus. They are no longer just underwriting the asset; they are underwriting the liquidity stress of the exit.

In practical terms, this means underwriting the speed and certainty of capital recovery, not merely its theoretical sufficiency.

How Lenders Price Liquidity Risk in 2026

In the current market, liquidity risk in lending is not just a line item in a risk report; it is the primary driver of the “liquidity premium” added to interest rate spreads. When a credit committee reviews a proposal, they are looking for financial stability through the lens of three specific mechanics:

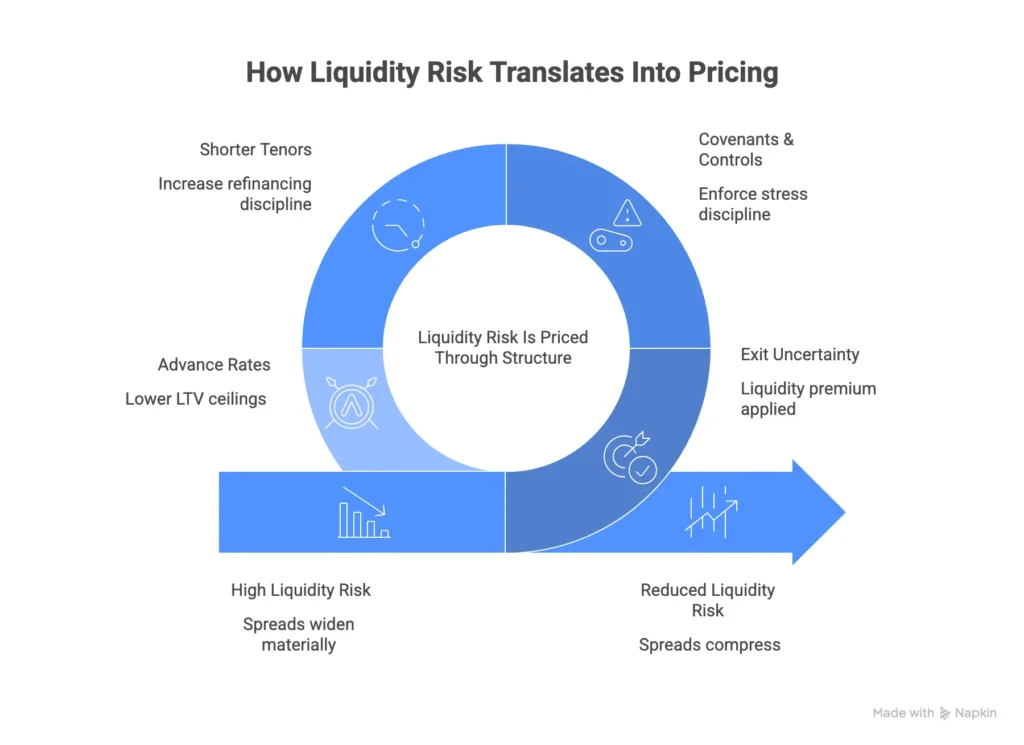

1. Exit Uncertainty and Spread Widening

If a borrower’s exit strategy relies on a public capital market or a highly specific buyer pool, lenders are applying a “liquidity haircut.” We are seeing higher spreads for assets that lack a deep, daily transactional market. Even if the credit risk is low, the market liquidity risk commands a premium.

2. Structural Controls and Tighter Covenants

Lenders are increasingly moving away from “covenant-lite” structures. Modern facilities now include more frequent stress testing requirements and tighter liquidity ratios. These are designed to act as early warning systems, forcing a deleveraging event or a capital injection long before a liquidity crisis becomes a solvency crisis.

3. Shorter Tenors and Amortisation

To mitigate funding liquidity risk, lenders are shortening tenors. By forcing more frequent refinancing or higher amortisation, the lender ensures the borrower remains “market-tested.” This prevents a situation where a borrower carries a large, un-amortised “bullet” payment into a volatile future market.

4. Advance Rates and Structural Subordination

Liquidity risk is also embedded in advance rates and intercreditor structures. Assets with uncertain exit depth are now facing lower loan-to-value ceilings, regardless of headline valuation. Senior lenders are increasingly requiring structural subordination beneath them to absorb liquidity shocks, while mezzanine capital is priced with an explicit liquidity premium. In practical terms, this means borrowers are contributing more equity not because credit risk has worsened, but because liquidity risk has become less tolerable.

Real-World Scenarios: Liquidity Pressures in Action

Scenario A: The Illiquid Trophy Asset

Consider a Commercial Real Estate (CRE) asset in a secondary UK city. The valuation remains robust based on discounted cash flow (DCF) models. However, the transactional volume for such assets has dropped by 60%. A borrower with a maturing facility finds that while their balance sheet shows 60% equity, no new lender is willing to provide a take-out loan because they cannot reliably price the market liquidity risk. The asset is valuable, but the liquidity position is terminal.

Scenario B: The Private Equity Sponsor

A sponsor-backed firm has used short-term funding to bridge an acquisition, planning to refinance into the high-yield bond market. A sudden spike in systemic volatility closes the bond window. Despite the company being profitable and having a healthy cash flow, the funding liquidity risk triggers a default. The lender, protecting their own liquidity reserve, is forced to take a hard line on the contingency funding plan.

Why Liquidity Risk Matters More Now

As we move through 2026, several factors have converged to make liquidity risk in lending the paramount concern for HNWIs and C-suite executives:

- Reduced Tolerance for Refinancing Dependency: Lenders are no longer assuming that “the market will be there” in three years. Every loan is being stress-tested against a “closed market” scenario.

- Increased Volatility in Funding Sources: The rise of private credit has provided more diversified funding, but these sources are often more sensitive to liquidity pressures than traditional clearing banks.

- Systemic Risk Awareness: Regulators and institutional investors are hyper-focused on failure to manage liquidity risk, leading to a more disciplined, and sometimes more rigid, credit environment. In short, liquidity stress is now assumed as a base-case modelling input, not a tail risk.

Strategic Considerations for Borrowers and Sponsors

For those managing significant capital stacks, the following disciplines are no longer optional:

- Stress-Test Exit Timing, Not Just Valuation: When modelling your downside, do not just ask “what if the value drops 20%?” Ask “what if it takes 24 months to sell instead of six?”

- Align Tenor with Asset Liquidity: Never fund an illiquid, long-term asset with short-term funding. The “liquidity mismatch” is the most common cause of avoidable default.

- Maintain a Liquidity Reserve: Ensure that you have stable funding or liquid assets (cash, gilts, or highly rated securities) that can be deployed to meet liquidity needs during a market freeze.

- Diversify Funding Sources: Do not rely on a single relationship or a single type of debt instrument. A diversified funding strategy is your best defence against a localized liquidity crisis.

Conclusion: Liquidity Determines Survival

In the financial landscape of 2026, the mantra has shifted. Leverage is a choice; liquidity is a necessity. While leverage can amplify returns during the upswing, it is the management of liquidity risk in lending that ensures survival during the inevitable contractions.

Lenders are no longer merely looking at what you own; they are looking at how quickly you can move. They are pricing the probability of your survival in a market where cash is not just king, but the only sovereign. Borrowers who continue to view their strength through the lens of LTV and asset value alone will find themselves increasingly misaligned with the reality of modern credit markets.

In 2026, leverage is negotiable. Liquidity is not. Understanding the nuances of balance sheet management and maintaining a robust liquidity position is the only way to protect both capital and reputation in an era of persistent uncertainty.

Contact Us

If your current capital structure assumes refinancing availability rather than proving liquidity resilience under stress, it warrants review. In 2026, disciplined liquidity management is not defensive positioning. It is a competitive advantage.