How the Credit Committee Approval Process Works in 2026

In the sophisticated landscape of 2026, the bridge between a term sheet and a funded transaction has become narrower and more precarious. For the C-suite, high-net-worth individuals (HNWIs), and institutional investors, the credit committee approval process is no longer a mere administrative formality or a “rubber-stamping” exercise. It has evolved into the primary execution risk in any significant financing transaction.

As we navigate a post-2025 financial environment characterised by tighter capital adequacy requirements, heightened sensitivity to market volatility, and a fundamental shift in risk appetite, understanding the inner workings of the credit committee is essential.

This guide provides a deep dive into the mechanics of the credit committee approval process in 2026, offering the clarity and strategic insight required by seasoned borrowers to ensure certainty of capital.

What Is the Credit Committee Approval Process?

At its core, the credit committee approval process is the formal governance mechanism through which a financial institution evaluates, challenges, and ultimately decides whether to commit capital to a specific borrower or project.

In 2026, this process applies almost exclusively to high-value, complex, or bespoke credits, such as commercial real estate finance, luxury asset finance, and large-scale securities-based lending. While smaller, standardised loans are now handled almost entirely by AI-driven algorithmic underwriting, the credit committee remains the “human-in-the-loop” sanctuary for transactions that require nuanced judgement, sector expertise, and a departure from standard risk models.

For the sophisticated borrower, the committee is the final gatekeeper. It is where the narrative of the deal meets the cold reality of the bank’s balance sheet constraints and regulatory obligations.

How the Credit Committee Approval Process Works in Practice

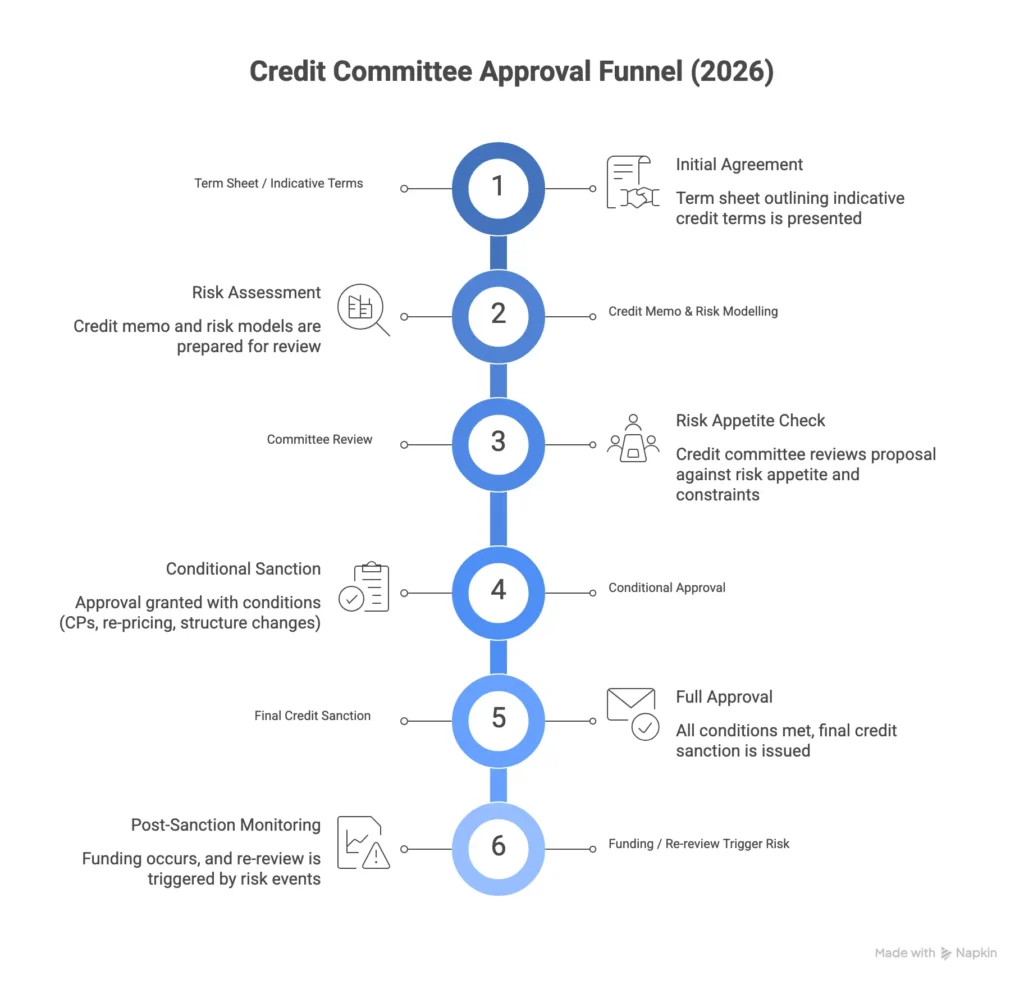

The journey through a credit committee in 2026 is more rigorous than in previous cycles. The process generally follows a five-stage trajectory, but the friction points have shifted.

1. Initial Review and Documentation

Before a file even reaches the committee, it undergoes a “pre-screen.” In 2026, this involves not just traditional financial statements, but a comprehensive digital audit. Credit analysts use real-time data feeds to verify liquidity, asset valuations, and cash flow durability. If the initial documentation does not meet the stringent risk management benchmarks, the deal is often killed before it gains any momentum.

2. The Credit Memo and Risk Assessment

The relationship manager or credit analyst prepares a formal “Credit Memo.” This document is the primary tool used by the committee to evaluate the proposal. It covers:

- Risk Assessment: A detailed breakdown of the borrower’s profile.

- Risk Models: How the deal performs under various “black swan” stress tests.

- External Credit Assessment: Integration of third-party ratings and market data.

3. Committee Deliberation

The committee typically comprises senior figures: the Chief Risk Officer (CRO), heads of lending, sector specialists, and occasionally a representative from the legal or compliance department. In 2026, these meetings are often hybrid, utilising advanced data visualisation to “stress” the deal in real-time. The deliberation focuses on risk appetite, not just whether the deal is “good,” but whether it fits the bank’s current risk exposure limits.

4. Decision, Amendments, or Conditions

The committee rarely issues a simple “Yes” or “No.” The most common outcomes in 2026 are:

- Approved with Conditions (CPs): Approval is granted, provided specific conditions precedent are met (e.g., higher equity contribution, additional collateral, or revised covenants).

- Restructured Approval: The committee likes the credit but dislikes the structure, leading to a mandatory re-pricing or a reduction in the Loan-to-Value (LTV) ratio.

- Deferred: The committee requests more information or waits for a specific market event to pass.

5. Documentation, Funding, and Monitoring

Once approved, the deal moves to legal documentation. However, in 2026, the credit committee approval process includes an ongoing monitoring component. The committee may set “triggers” that allow them to revisit the approval if market conditions shift significantly before the first drawdown.

What Credit Committees Focus on in 2026

To navigate the process successfully, one must understand the lenses through which the committee views every application. The priorities of financial services institutions have shifted toward defensive positioning.

Risk Appetite vs. Portfolio Exposure

A borrower may have an impeccable credit history, but if the bank is already at its limit for “London Prime Residential” or “Tech-Sector Mezzanine Debt,” the committee will likely decline the deal. In 2026, risk appetite is governed by portfolio diversification. Committees are hyper-aware of concentration risk and will often sacrifice a high-quality deal to maintain a balanced book.

Liquidity, Leverage, and Cash Flow Durability

In an era of persistent inflation and fluctuating interest rates, “static” cash flow projections are ignored. Committees now demand “dynamic” models that show how a borrower handles a 300-basis-point rise in rates or a 20% drop in revenue. They are looking for “durability”, the ability of the credit to survive prolonged market stress.

Collateral Quality and Downside Protection

For luxury asset finance or commercial real estate finance, the quality of the underlying asset is paramount. Committees in 2026 are sceptical of “optimistic” valuations. They focus on the “liquidation value” in a distressed scenario. If the asset cannot be exited quickly, the committee will demand lower leverage or higher pricing to compensate for the illiquidity.

Governance, Controls, and Execution Risk

For corporate borrowers, the committee scrutinises internal risk controls and governance structures. They want to see that the borrower has the professional infrastructure to manage the debt. Governance changes within the borrowing entity are often flagged as red flags, as they suggest potential instability.

Where Borrowers Misunderstand Approval

Even experienced CFOs and HNWIs often fall into traps during the committee review phase. These misconceptions can lead to broken deals and wasted time.

Conditional Approval vs. Final Approval

A “Credit Approved” email from a relationship manager is often misinterpreted as a guarantee of funding. In 2026, “Credit Approval” is almost always conditional. Until the final “Credit Sanction” is issued and the audit trail is complete, the terms are subject to change.

The “Last-Minute” Pivot

It is common for a committee to approve a deal on a Monday, only for a global market event on Tuesday to trigger a “re-review.” In 2026, committees have the mandate to pull or amend approvals right up until the point of funding if the market risk profile changes.

Internal Politics and Capital Allocation

Large banks are not monoliths. Sometimes, a deal is rejected not because of its credit quality, but because another department won the internal battle for capital allocation

Real-World Scenarios: The Credit Committee in Action

To illustrate the complexities of the credit committee approval process in 2026, consider these anonymised examples based on recent market activity.

Scenario A: The Restructured CRE Deal

A developer sought a £50m facility for a sustainable office refurbishment in the City of London. The borrower had a 20-year track record and 40% equity.

- The Committee’s View: While the credit was strong, the committee was concerned about the “exit cap rate” in a high-rate environment.

- The Outcome: Approved, but with a mandatory “interest reserve” held in escrow for 24 months and a reduction in the LTV from 60% to 52%. The borrower had to pivot their capital strategy last minute to fill the gap.

Scenario B: The Securities-Based Lending Delay

An HNWI wanted to leverage a significant portfolio of Tier-1 equities to fund a private equity commitment.

- The Committee’s View: The equities were liquid, but the committee’s risk models flagged a high correlation between the borrower’s portfolio and the bank’s existing risk exposure in the tech sector.

- The Outcome: The deal was delayed by three weeks while the committee debated the concentration risk. It was eventually approved only after the borrower agreed to a more diverse “collateral basket,” including sovereign bonds.

Scenario C: The Downsized M&A Facility

A mid-cap firm sought funding for a strategic acquisition.

- The Committee’s View: The acquisition made sense, but the committee felt the “pro-forma” leverage was too aggressive given the internal capital adequacy assessment process (ICAAP) guidelines.

- The Outcome: The deal was approved but downsized by 15%. The borrower had to secure a mezzanine layer of debt at a higher cost to complete the acquisition.

Why the Credit Committee Approval Process is Becoming More Restrictive

The tightening of the credit committee approval process is not a temporary cyclical shift; it is structural. Several factors are driving this trend in 2026:

- Capital Constraints: Regulatory frameworks (evolving from Basel IV) have made capital “more expensive” for banks to hold. Every pound lent must work harder, leading to extreme selectivity.

- Increased Internal Scrutiny: Post-2024, internal audit and compliance functions have been given more power. Every committee review is now documented with the expectation that it will be scrutinised by national regulators.

- Market Volatility: The speed at which market conditions change in 2026 means that “stale” data (even a week old) is viewed with suspicion. This leads to more frequent requests for updated information, slowing the process down.

AI and Risk Modelling: While AI helps in data processing, it has also made committees more conservative. When a risk model shows a 5% chance of total loss in a stress scenario, human committee members are increasingly hesitant to override the machine’s warning

What Borrowers Should Consider: Strategic Guidance

For those seeking certainty of execution, the following strategies are essential when facing the credit committee approval process in 2026.

1. Anticipate Objections Early

Do not wait for the committee to find the “hole” in your deal. Address it in the initial memo. If your leverage is high, explain the specific cash flow protections you have in place. If your sector is volatile, provide third-party data to justify your projections.

2. Structure for Downside Protection, Not Just Pricing

In 2026, a committee is more likely to approve a deal with a slightly higher interest rate but “tight” covenants than a “cheap” deal with loose terms. If execution certainty is your priority, offer the committee the protections they crave, such as robust reporting requirements or additional collateral.

3. Build Timing Buffers

The days of “two-week approvals” for complex credits are largely over. Assume the credit committee approval process will take 30% longer than your relationship manager suggests. Build these buffers into your purchase agreements and M&A timelines.

4. Understand the “Internal Capital” Context

Ask your lender: “How does your current portfolio exposure look for my sector?” and “Are there any internal capital constraints I should be aware of?” A transparent conversation about the bank’s internal “appetite” can save months of wasted effort.

5. Explore Alternative Capital Routes

Where certainty of execution is paramount and the traditional credit committee approval process appears too restrictive, consider alternative capital providers. Private credit funds and family offices often have more streamlined committee review structures and a different risk appetite than Tier-1 institutional banks.

Conclusion: Approval is No Longer the Finish Line

In 2026, the credit committee approval process has become the crucible of modern finance. It is the point where strategic intent meets regulatory and balance-sheet reality. For the C-suite and HNWIs, navigating this process requires more than just a strong balance sheet; it requires an understanding of the psychological and structural drivers behind credit decisions.

The key takeaway for 2026 is that approval is no longer a binary “yes.” It is a dynamic state that must be managed through meticulous preparation, strategic structuring, and an acute awareness of the lender’s internal constraints. In this environment, certainty of execution is the most valuable currency.

Discuss Your Execution Strategy

Navigating the complexities of credit committee expectations requires a discreet and informed approach. Whether you are restructuring existing debt, seeking Commercial Real Estate Finance, or exploring asset-based lending, understanding the current risk management landscape is vital.

- Assess Execution Risk: Evaluate your transaction’s viability before it reaches the committee.

- Structure for Certainty: Align your deal parameters with 2026 risk appetite benchmarks.

- Explore Alternatives: Identify capital routes where timing and flexibility are prioritised.

A discreet discussion can clarify execution risk before a transaction reaches committee review.