ESG Lending Criteria 2026: The Credit Layer Borrowers Miss

For the better part of a decade, Environmental, Social, and Governance (ESG) considerations were often viewed by C-suite executives and High-Net-Worth Individuals (HNWIs) as a peripheral concern, a matter of corporate social responsibility (CSR) reports, glossy brochures, and reputational management. However, as we approach a pivotal regulatory horizon, the landscape has shifted fundamentally.

By 2026, ESG is no longer a marketing overlay; it has become a formal, non-negotiable credit risk layer.

For CFOs, Treasurers, and sophisticated borrowers, the implications are stark. The ESG lending criteria 2026 framework represents a transition from “alignment” to “creditworthiness.” Lenders are no longer asking if your business is “good” for the planet; they are asking if your ESG profile makes you a default risk. If you are still treating ESG as a disclosure exercise rather than a core component of your capital structure, you are missing the very layer that will determine your access to liquidity in the coming 24 months.

The Shift: From Policy Language to Mandatory Credit Input

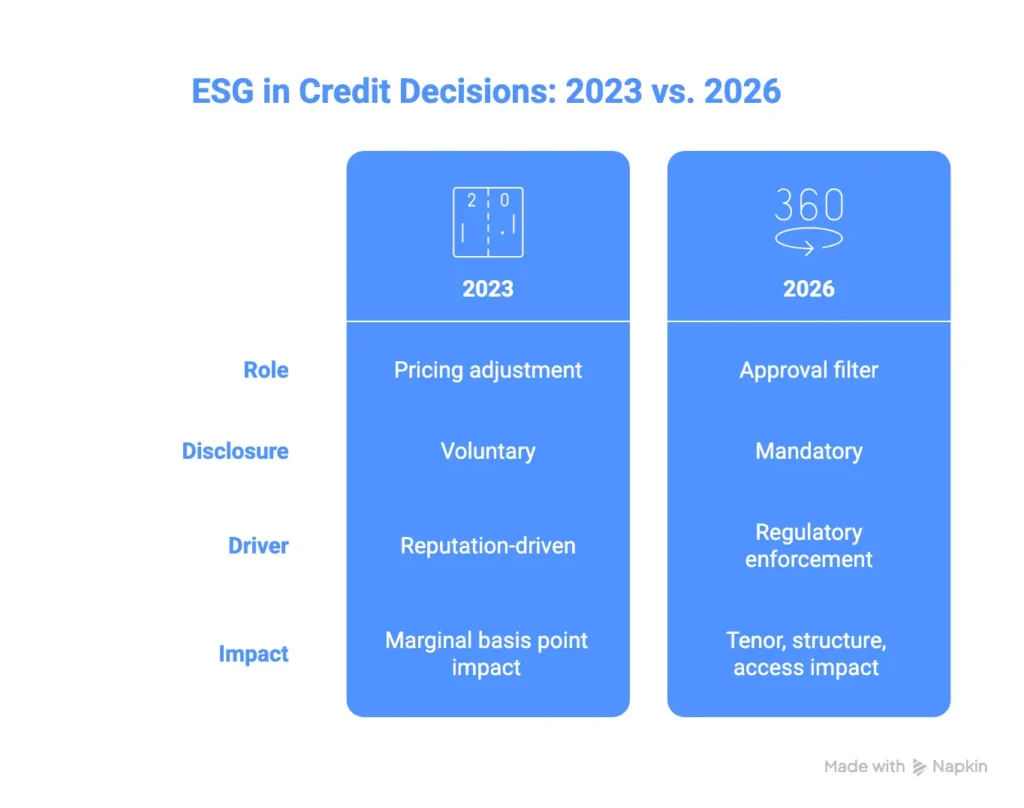

The transition we are witnessing is driven by a convergence of regulatory enforcement and the hardening of internal bank risk models. Historically, a borrower’s ESG score might have earned them a five-basis-point discount on a revolving credit facility (RCF). In the 2026 landscape, these criteria are being used to determine whether a credit committee approves a loan at all.

This shift is underpinned by the European Banking Authority (EBA) and its guidelines on the management of ESG risks. These guidelines mandate that financial institutions integrate ESG factors into their risk management frameworks, credit granting processes, and monitoring systems. By January 2026, the grace period for “soft” implementation will have evaporated. Banks in the UK and EU will be required to demonstrate to regulators exactly how ESG data influences their capital allocation and risk-weighted assets.

For the borrower, this means that ESG lending criteria 2026 is the new “Credit Committee Gatekeeper.”

What Are ESG Lending Criteria in 2026?

To navigate this new environment, one must distinguish between three distinct types of ESG:

- Marketing ESG: The public-facing narrative (largely irrelevant to credit).

- Regulatory ESG: Compliance with the Corporate Sustainability Reporting Directive (CSRD) and EU Taxonomy (the baseline requirement).

- Credit ESG: The specific metrics that influence a lender’s internal rating of your business (the focus of this article).

In 2026, credit ESG functions as a predictive indicator of financial distress. Lenders are looking for financial risks stemming from ESG factors. For example, a company with a high carbon footprint isn’t just “un-green”; it is a company facing imminent carbon taxation, rising energy costs, and potential “stranded asset” status. These are direct threats to cash flow durability and debt serviceability.

The Role of the EBA and the Regulatory Framework

The European Banking Authority (EBA) has been clear: ESG risks are not a new category of risk, but rather drivers of existing financial risks (credit risk, market risk, and operational risk). Under the management of ESG risks framework, banks must now assess:

- Physical Climate Risks: Does the borrower have assets in flood zones or areas prone to extreme weather?

- Transition Risks: How vulnerable is the borrower’s business model to regulatory changes like the EU Taxonomy Regulation or the phase-out of internal combustion engines?

- Governance Risks: Does the board have the expertise to manage a transition plan, or is the company exposed to litigation risk?

Why ESG Became a Credit Risk, Not a Sustainability Metric

The reason ESG lending criteria 2026 has become so potent is that it is now embedded in capital allocation models. Banks are under pressure from their own investors and regulators to de-risk their balance sheets. A borrower with poor ESG performance increases the bank’s own “Green Asset Ratio” (GAR) volatility.

Consequently, ESG is now treated with the same analytical rigour as leverage ratios, interest cover, and EBITDA margins.

Financial Materiality vs. Values

The 2026 credit environment ignores “values-based” investing in favour of financial materiality. Lenders are assessing risks and opportunities through a cold, analytical lens. If a borrower cannot provide audit-ready ESG data, the lender must assume the worst-case scenario in their risk model. This “data gap” results in a higher cost of capital or a lower credit internal rating, regardless of the borrower’s actual performance.

How Lenders Actually Apply ESG Lending Criteria

In the credit room, the three pillars of ESG are dismantled and reassembled as financial risk indicators.

1. Environmental: Transition Credibility vs. Ambition

By 2026, lenders will look past “Net Zero 2050” pledges. They want to see a transition plan that is backed by transition finance and clear Capex commitments.

- Refinancing Risk: If your primary assets do not meet EU Taxonomy standards for energy efficiency, will a lender be willing to refinance them in five years?

- Physical Asset Exposure: Lenders are using sophisticated geospatial data to map physical climate risks across a borrower’s portfolio. If your supply chain is concentrated in a climate-vulnerable region, your credit limit may be capped.

2. Social: Labour and Supply Chain as Operational Risk

Social criteria are often the most misunderstood. In a credit context, “Social” equals “Operational Continuity.”

- Supply Chain Disruption: Under the Corporate Sustainability Due Diligence Directive (CSDDD), borrowers are responsible for their entire value chain. A breach in labour standards three tiers down your supply chain can lead to legal injunctions, halting your ability to generate revenue.

- Litigation Risk: Social failures lead to class-action lawsuits. Lenders view these as contingent liabilities that threaten the seniority of their debt.

3. Governance: The Proxy for Management Quality

In 2026, governance is the most critical “Sovereign” layer of the credit decision.

- Data Integrity: If a borrower’s ESG reporting is found to be inaccurate (greenwashing), it is treated as a failure of internal controls, a major red flag for any credit officer.

- Board Oversight: Lenders want to see that ESG is a standing item on the board agenda, not delegated to a junior sustainability officer. Weak governance is seen as a proxy for a management team that is unprepared for the complexities of the modern capital market.

Real-World Credit Scenarios Borrowers Miss

To understand the impact of ESG lending criteria 2026, we must look at how deals are being structured today for the 2026 horizon.

Case Study A: The “Stranded” Commercial Real Estate Asset

A HNWI holds a portfolio of prime London office space. While the location is excellent, the buildings have poor EPC ratings and do not align with the EU Taxonomy Regulation. In 2023, this was a minor pricing issue. By 2026, the lender refuses to provide a 10-year term, offering only a 3-year “bridge to upgrade” at a significantly higher margin. The lender’s rationale: the asset will be un-lettable and un-sellable by 2030.

Case Study B: The Margin Ratchet Failure

A mid-cap manufacturer secures a loan with an ESG-linked margin ratchet. However, due to poor data collection processes, they fail to provide verified ESG data by the reporting deadline. Not only does the margin increase, but the failure triggers a “Technical Default” clause, allowing the lender to renegotiate the entire sustainable finance framework of the loan, imposing stricter reporting and due diligence requirements.

Case Study C: The Narrowing Private Capital Pool

A family office seeking access to capital for a new industrial venture finds that 40% of their usual lender pool is “closed for business” because the venture does not meet the EU Taxonomy disclosures required for the bank’s “Green Transition” portfolio. The remaining lenders, sensing a lack of competition, demand equity-like returns for senior debt.

Why This Tightens Further in 2026

The “wait and see” approach is the most dangerous strategy a borrower can employ. Several factors will cause the credit market to tighten significantly as we enter 2026:

- Mandatory ESG Risk Management: The EBA guidelines move from “recommendation” to “supervisory expectation.” Banks that fail to show monitoring of esg risks in their portfolios will face higher capital charges from their central banks.

- The January 2026 Deadline: This is the point where many of the reporting obligations under CSRD and ESRS become mandatory for a wider range of companies, including many large private firms.

- Data Quality and Standardisation: The “wild west” of ESG ratings is ending. Lenders are moving toward standardised reporting standards, making it impossible for borrowers to hide poor performance behind bespoke metrics.

- Integration of ESG into ESMA and EBA Frameworks: The European Securities and Markets Authority (ESMA) and the EBA are aligning their views on financial disclosures, ensuring that what you tell your investors is exactly what you tell your lenders.

What Borrowers Should Focus On Now

For CFOs and decision-makers, the goal is to preserve access to capital and maintain investment decisions flexibility. This requires a shift in how ESG is managed internally.

Treat ESG Like Financial Reporting, Not Marketing

Your ESG data must be as robust as your P&L. This means implementing risk management frameworks that capture esg factors in real-time. Lenders in 2026 will expect audit-ready ESG data that has been through a rigorous due diligence process.

Focus on Transition Sequencing

Lenders do not expect you to be “Green” tomorrow. They do, however, expect a credible transition plan. This plan should outline:

- How you will reduce carbon intensity.

- The Capex required to meet regulatory requirements.

- How these investments will be funded (e.g., through transition finance).

Understand Your Lender’s Constraints

Every bank has a different sustainable finance framework. Some are focused on reducing their “Brown” exposure; others are aggressively chasing “Green” assets to meet their own reporting and due diligence targets. Knowing where your lender stands in their own ESG journey is essential for successful negotiation.

Data Quality is the New Collateral

In the absence of high-quality esg data, lenders will apply “proxy data,” which is almost always more conservative (and expensive) than your actual data. Investing in data collection and monitoring of esg risks is no longer an administrative cost—it is a capital-preservation strategy.

The Impact of ESG on Structured Credit and Luxury Assets

Even in the realms of Luxury Asset Finance and Securities-Based Lending, ESG is making its presence felt.

- Superyachts and Private Aviation: Lenders are increasingly looking at the propulsion systems and carbon offset programmes associated with these assets. A “dirty” asset is becoming harder to finance on a long-term basis.

- Commercial Real Estate Finance: As discussed, the “Green Premium” is being replaced by a “Brown Discount.” Assets that do not meet EU Taxonomy regulation standards are seeing their loan-to-value (LTV) ratios squeezed.

- Portfolio Rebalancing: For HNWIs, investment decisions are increasingly influenced by the ESG ratings of the underlying securities. A portfolio with poor ESG metrics may face higher haircuts in a securities-based lending (SBL) facility.

Conclusion: ESG Is Now a Gatekeeper, Not a Badge

As we look toward January 2026, the message for high-level decision-makers is clear: ESG lending criteria 2026 represent the most significant change to credit underwriting in a generation.

The “Credit Layer” that many borrowers miss is the fact that ESG is now a fundamental component of financial risk. It is no longer about being a “good corporate citizen”; it is about proving that your business model is resilient to the tectonic shifts of the energy transition, social upheaval, and regulatory scrutiny.

Borrowers who adapt early, by integrating esg risk management into their core operations and providing transparent, audit-ready ESG data, will find themselves with a competitive advantage. They will enjoy wider access to capital, better pricing, and more flexible covenants.

Those who continue to treat ESG as a disclosure obligation will find the credit markets increasingly cold. By 2026, the question won’t be whether you have an ESG policy, but whether your ESG profile allows you to remain a “bankable” entity.

Actionable Insights for the C-Suite:

- Audit Your Data: Ensure your esg reporting meets European sustainability reporting standards before your next refinancing cycle.

- Review Your Transition Plan: Is it a marketing document or a financial roadmap? Ensure it includes specific Capex for transition finance.

- Engage Your Lenders Early: Ask your banks how they are applying eba guidelines to your specific sector.

- Monitor Regulatory Changes: Stay ahead of uk and eu regulatory shifts to avoid being caught by “sudden” due diligence requirements.

For borrowers assessing refinancing, structured credit, or private capital solutions in 2026, understanding how ESG is applied inside credit decisions, not how it is reported, is now essential. The difference between a successful capital raise and a failed one may well sit within this “missing” credit layer. To discuss your options contact us today