Mezzanine Financing in Real Estate: How Debt Is Structured, Secured and Enforced

A senior lender capping leverage at 60 per cent loan-to-cost used to be the exception. In 2026 it is closer to standard practice, and the gap that leaves on a development or acquisition has to be filled by something other than a larger cheque from the sponsor.

Mezzanine financing in real estate is how that gap gets closed without diluting the sponsor’s equity position. What determines whether it works in practice, rather than just on the term sheet, is how the facility is documented against the senior lender, and what actually happens to control of the asset if the deal underperforms. For the basic mechanics of where mezzanine debt sits relative to senior debt and equity, see our Real Estate Finance Basics guide.

This post covers what that overview doesn’t: how mezzanine financing in real estate is structured, how the intercreditor relationship is documented, and how enforcement actually plays out.

How a Mezzanine Financing in Real Estate is Structured

Mezzanine financing in real estate is built around four components, each negotiated rather than assumed.

Interest structure: cash-pay, payment-in-kind (PIK), or a blend. PIK interest accrues to the principal rather than requiring monthly cash service, which preserves liquidity during construction or stabilisation but increases the redemption amount due at exit.

Equity kicker: warrants or a conversion option giving the mezzanine lender a stake in the project’s upside, typically a percentage of equity value crystallising on sale or refinancing.

Subordination: the mezzanine lender is repaid only after the senior facility is satisfied, formalised through the intercreditor agreement covered below. For how this layer sits against senior debt, preferred equity and common equity across a transaction, see our Capital Stack Structuring guide.

Fees: arrangement and exit fees are standard, with exit fees often structured to compensate for a shorter than expected hold period.

The Intercreditor Agreement: Documenting the Relationship with the Senior Lender

The intercreditor agreement is what actually governs the mezzanine lender’s position, not the headline rate. For how standstill periods, cure rights and payment subordination work generally, see our Intercreditor Agreement guide. What’s specific to real estate is the form the agreement takes and how subordination is achieved structurally rather than contractually.

UK and European real estate finance transactions involving mezzanine debt typically reference the LMA’s real estate finance intercreditor agreement, first published in 2014 and updated to cover contractual subordination structures in 2018.

Two subordination models are in use. Structural subordination lends the mezzanine debt to a separate holding entity sitting above the senior borrower, so the mezzanine lender’s claim runs through the corporate structure rather than directly against the property. Contractual subordination instead places senior and mezzanine financing in real estate in the same borrowing entity, with priority governed entirely by the intercreditor agreement’s payment waterfall.

This distinction, not the standstill period itself, is what a sponsor negotiating a real estate mezzanine facility needs to get right, since it determines which entity in the structure the mezzanine lender’s claim runs against if enforcement is ever triggered.

Enforcement: How a Mezzanine Lender Actually Takes Control

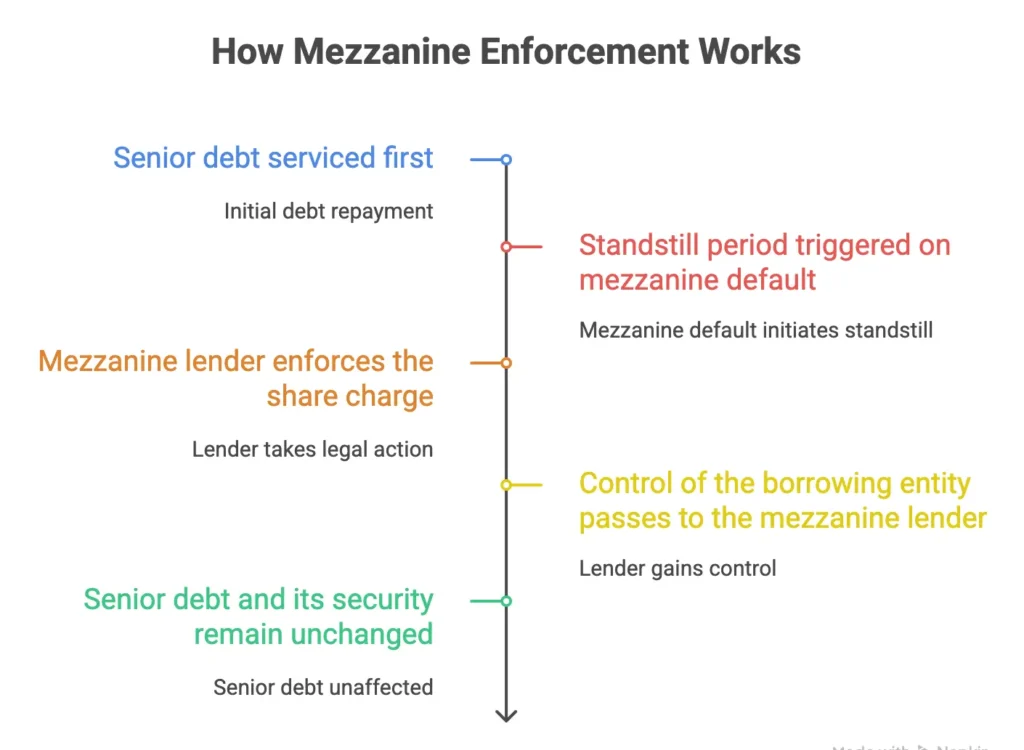

Mezzanine financing in real estate is not secured against the property. It is secured by a charge over the shares in the entity that owns, directly or indirectly, the property. That distinction is what gives mezzanine enforcement its defining characteristic: speed.

Where senior debt requires a property-level mortgage enforcement process, a mezzanine lender enforcing a share charge can, subject to the standstill period and any restrictions in the intercreditor agreement, take control of the borrowing entity directly. The senior debt and its security remain entirely intact and unaffected; only the equity sponsor’s position changes.

This is sometimes described as the mezzanine lender stepping into the sponsor’s shoes rather than foreclosing on the asset itself. It is faster than a property foreclosure, but the mezzanine lender’s ability to direct that process is still constrained by whatever instructions the intercreditor agreement gives to senior lenders or a common security trustee.

For a sponsor, the practical implication is that real protection against losing control sits in the intercreditor agreement’s standstill and cure provisions, not in the headline interest rate or the absence of a property-level mortgage.

What Mezzanine Lenders Underwrite in Real Estate Financing

Mezzanine lenders conduct due diligence that is distinct from, and in some respects more exacting than, a senior lender’s, because their recovery in a downside scenario depends entirely on enforcement working as drafted.

Sponsor track record carries disproportionate weight. A mezzanine lender is effectively underwriting the sponsor’s ability to deliver the business plan, since there is no direct property security to fall back on if execution falters. A developer without a comparable completed scheme will struggle to access pricing at the lower end of the range, regardless of asset quality, which is why a credible proposal for commercial real estate financing matters as much for a mezzanine raise as for the senior facility itself.

Senior debt terms are scrutinised as closely as the mezzanine lender’s own facility. The mezzanine lender’s position is only as strong as the intercreditor agreement governing it, so the senior facility’s covenants, default triggers and the senior lender’s willingness to negotiate cure rights all directly affect pricing and appetite.

Asset and location quality determine the realistic outcome if enforcement is ever needed. A mezzanine lender taking control of the borrowing entity still needs the underlying asset to be saleable or refinanceable on workable terms, so secondary locations and specialist asset types attract a wider pricing premium than the headline subordination risk alone would suggest.

Exit certainty is assessed independently of the sponsor’s stated plan. Lenders price in a meaningful probability that the stated exit, sale or refinancing, does not occur on schedule, and structure PIK accrual and maturity dates to survive a six to twelve month slippage without forcing a premature enforcement decision.

When Mezzanine Debt Makes Sense

Mezzanine financing in real estate is typically used in one of four scenarios.

Bridging a funding gap: the most common use, where total project cost exceeds the combined senior loan and the sponsor’s available equity.

Maximising leverage and returns: reducing the equity requirement on one project frees capital for deployment elsewhere.

Preserving ownership and control: an alternative to a further common equity partner, avoiding dilution of the sponsor’s stake.

Funding a time-sensitive acquisition: mezzanine finance can typically be arranged faster than a full equity raise, which matters in a competitive bidding process.

Worked Example: Closing a Capital Stack Gap

Consider a £100 million commercial property acquisition. Senior debt covers £60 million, the sponsor’s equity covers £20 million, and a £20 million mezzanine facility closes the remaining gap at 14 per cent with warrants over a 10 per cent equity interest.

What matters is what happens if the scheme underperforms. Say the senior facility goes into default. The intercreditor agreement’s standstill period stops the mezzanine lender acting for a fixed window. If it has negotiated cure rights, it can step in and cure the senior default directly, protecting the equity value its position depends on, rather than waiting out the standstill while that value erodes. Whether that option exists comes down to how the intercreditor agreement was drafted before the facility closed, not to anything in the loan’s headline terms.

Advantages and Disadvantages of Mezzanine Debt

Advantages:

- Preserves equity: avoids the ownership dilution that comes with raising further common equity.

- Flexible terms: PIK, cash-pay or blended interest can be matched to the project’s cash flow profile.

- Increased leverage: supports larger schemes than the sponsor’s equity alone would permit.

- Aligned interests: the equity kicker gives the mezzanine lender a direct stake in the scheme’s success.

Disadvantages:

- Higher cost of capital: rates and fees sit well above senior debt.

- Dilution risk on underperformance: warrant exercise dilutes the sponsor if returns fall short.

- Documentation complexity: the intercreditor agreement requires specialist legal review on both sides.

- Subordinate enforcement position: recovery depends on the senior facility being satisfied first, and on the standstill and cure provisions negotiated into the intercreditor agreement.

Mezzanine Financing vs Preferred Equity

Mezzanine debt and preferred equity fill the same gap in the capital stack, but the legal form is different, and that difference is what drives the choice between them. Mezzanine is a loan secured by a share charge and coordinated with the senior lender through the intercreditor agreement set out above. Preferred equity is an ownership interest with no lien and no intercreditor negotiation, which is often faster to close and is sometimes the only available option where the senior lender’s documents prohibit further subordinate debt.

For the equity-side comparison in full, including where preferred equity sits in the capital stack and how its control rights are negotiated, see our Preferred Equity in Real Estate guide.

Conclusion

Mezzanine financing in real estate remains one of the most effective tools for closing a capital gap without ceding control, but its value depends entirely on documentation that holds up if a deal underperforms. The interest rate and equity kicker are negotiated in an afternoon. The intercreditor agreement, and the standstill, cure and enforcement provisions inside it, is what actually determines whether that structure protects the sponsor or the mezzanine lender when it is tested.

This post sits within our broader review of capital structuring in commercial real estate. For the full sequence from acquisition through to close, see our Commercial Real Estate Financing: 9 Steps to Close guide, the starting point for our Commercial Real Estate Finance Playbook.

If you are structuring a mezzanine facility and want the intercreditor terms to protect your position rather than someone else’s, we welcome a discreet conversation. Speak to us today