Subscription Finance 2026: Private Credit’s Liquidity Engine

The landscape of private capital has shifted significantly over the last half-decade. As we navigate the financial terrain of 2026, the era of easy exits and rapid capital recycling has given way to a more complex environment. For the C-suite, fund principals, and sophisticated investors, the focus has moved from pure asset selection to the strategic management of liquidity. In this context, subscription finance has graduated from a back-office treasury convenience to a cornerstone of competitive fund management.

We are currently witnessing a “liquidity pinch” where delayed exits and slower fundraising cycles are creating operational drag. Managers facing tighter underwriting conditions should also review the expectations outlined in our Structured Finance Modelling guide. Funds cannot afford to let capital sit idle, nor can they burden Limited Partners (LPs) with fragmented capital calls. This is where subscription finance, specifically credit facilities secured by investors’ uncalled capital commitments, has become the liquidity engine of choice.

This article explores how these facilities are reshaping private credit, the nuances of their structure in the current market, and why they are essential for maintaining agility in a constrained economic cycle.

For a detailed look at how lender expectations have evolved, see our Data Room for Lending analysis.

Subscription Finance and the Evolution of Credit Facilities

To understand the strategic importance of this tool in 2026, one must first strip away the jargon. At its core, subscription finance (often referred to as capital call facilities or sub lines) is a revolving credit facility. However, unlike traditional leverage which is secured by the underlying assets of the fund, these facilities are secured by the uncalled capital commitments of the investor base.

Historically, banks dominated this market, viewing it as a low-risk entry point to build relationships with top-tier sponsors. Broader liquidity and credit cycle trends are regularly analysed by the Bank for International Settlements. Today, the ecosystem has expanded. We now see a diverse range of lenders, including non-bank financial institutions and institutional investors, entering the space.

The Mechanics of the Subscription Finance Facility

The structure is elegant in its simplicity but powerful in its application. Accurate modelling of these liquidity movements is essential, as outlined in our Structured Finance Modelling framework. When a fund manager identifies an investment opportunity or incurs an expense, they draw down on the subscription finance facility rather than issuing an immediate capital call to investors. The lender advances the funds, secured by the pledge of the investors’ obligation to contribute capital when called.

The facility is typically short-term, often with a tenor of 12 to 36 months, and is repaid once the capital is eventually called from the LPs. This mechanism allows the fund to:

- Streamline cash flows.

- Reduce the frequency of capital calls (smoothing the administrative burden).

- Execute transactions with speed and certainty.

For the borrower, usually the General Partner (GP) acting on behalf of the fund, the creditworthiness of the facility relies heavily on the quality of the investor base. A fund backed by institutional giants and sovereign wealth funds will command better terms than one with a high concentration of smaller, less rated investors.

The Strategic Edge: Why Managers Are Adopting Subscription Finance

In 2026, the utility of subscription finance extends far beyond administrative ease. It has become a strategic imperative for financial management within private markets.

1. Speed of Execution of Subscription Finance in Competitive Markets

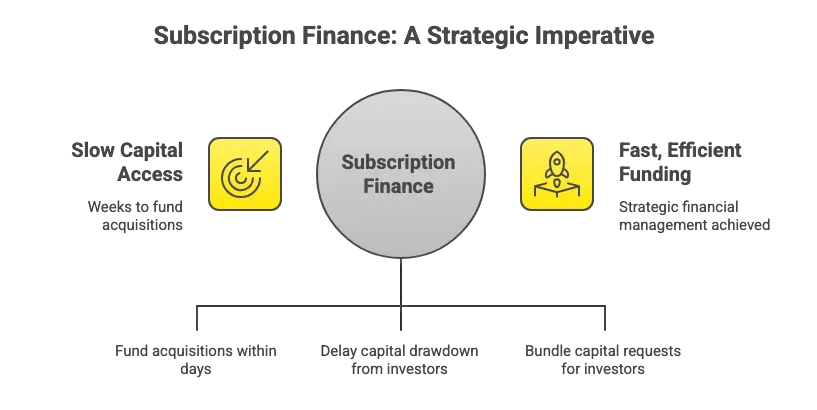

In private equity and private credit, the ability to close a deal quickly is often the difference between winning and losing an asset. Subscription finance provides immediate access to capital. A manager can fund an acquisition within days using a credit line, whereas calling capital from a diverse pool of LPs can take weeks. This flexibility allows funds to act like cash buyers, securing assets before competitors can mobilise their capital.

2. Optimising Internal Rate of Return (IRR)

While controversial in the past, the impact of these facilities on IRR is now a standard consideration. By delaying the drawdown of capital from investors, the clock on the preferred return starts later. This can optimize the IRR for the LPs, although sophisticated investors now look closely at Multiple on Invested Capital (MOIC) to ensure the performance is genuine and not purely a result of financial engineering.

3. Operational Efficiency for Investors

For the investor, particularly large institutions and Family Offices, frequent and irregular capital calls are an administrative headache. Subscription finance allows the manager to bundle these requests. Instead of five small calls of £2 million each, the manager can issue a single capital call for £10 million. This predictability is highly valued by the subscriber.

Real-World Scenarios: Subscription Finance in Action

To illustrate the versatility of these credit facilities, consider the following scenarios typical of the 2026 market environment.

Scenario A: The Private Credit Fund

A private credit fund identifies a time-sensitive opportunity to provide a bridge loan to a distressed company. The borrower needs the funds within 48 hours. The fund manager utilises their subscription finance line to deploy the capital immediately. Three months later, once the loan is syndicated or the fund decides to retain the position long-term, they issue a capital call to repay the line. This speed is unlike traditional financing routes and secures the deal.

Scenario B: The Real Estate Sponsor

A real estate fund is in the due diligence phase for a commercial property portfolio. They need to place a significant deposit and cover legal fees. Rather than calling capital for these “soft costs” which might be returned if the deal falls through, they draw on their sub lines. If the deal proceeds, the cost is rolled into the final capital call. If not, the line is repaid from other sources or a smaller call, keeping the financial statements clean and the LPs undisturbed.

Scenario C: Bridging the Fundraising Gap

A manager is launching a successor fund but has not yet reached the final close. They have secured a “first close” with a cornerstone investor. A subscription finance facility allows them to start investing immediately based on the commitments of that first close, ensuring they don’t miss the current vintage’s opportunities while waiting for the final investor base to settle.

Subscription Finance: Navigating Risks and Considerations

Despite the clear advantages, subscription finance is not without risk. Stakeholders must approach these facilities with a clear understanding of the potential downsides.

1. The Risk of Default and Cross-Default

If an LP defaults on a capital call, the lender typically has the right to step in. In severe cases, this can trigger cross-default provisions. The LPA (Limited Partnership Agreement) is the critical document here. It must contain specific provisions regarding the pledge of uncalled capital and the rights of the lender. Investors must be aware that their commitment is the collateral.

2. Interest Rate Sensitivity

In a higher interest rate environment, the cost of the facility can drag on the fund’s net performance. Managers must forecast the cost of borrowing against the expected return on the asset. If the cost of the sub line exceeds the hurdle rate, it destroys value. Financial services providers are now offering more bespoke hedging products to mitigate this, but the risk remains.

3. Over-Leverage and the “Downstream” Effect

There is a concern regarding the layering of leverage. If a fund uses subscription finance at the top level, and the portfolio companies use downstream leverage (asset-level debt), the total system leverage increases. In a market downturn, this can amplify losses. Credit ratings agencies are increasingly scrutinising this “leverage on leverage.”

4. Investor Concentration

Lenders will apply strict concentration limits. If a single investor holds 40% of the fund’s commitments, the borrowing base (the amount the fund can draw) will be capped or adjusted based on that investor’s credit rating. Managers must curate their investor base carefully to maximise their borrowing capacity.

Structuring the Facility: Subscription Finance Best Practices for 2026

For decision-makers looking to implement or amend a facility, the following structural elements are paramount.

The Borrowing Base

This is the calculation that determines how much can be drawn. It is usually a percentage of the uncalled capital of “included investors” (those with high credit ratings). Uncalled capital commitments from investors with lower credit quality may be excluded or given a lower advance rate.

LPA Provisions

The Limited Partnership Agreement must be bespoke to allow for the facility. It needs to explicitly permit the pledge of capital calls and waive the right of investors to claim set-off defenses against the lender. Without these “no-setoff” clauses, banks and non-bank lenders will struggle to get credit committee approval.

Clean Down Periods

To ensure the facility remains a bridge and not permanent leverage, lenders often require a “clean down”, a period where the facility must be repaid to zero. This enforces discipline and ensures the facility is used for short-term liquidity rather than long-term leverage.

Beyond 2026: The Future of Call Facilities

As we look toward the latter half of the decade, the market is evolving. We are seeing the rise of hybrid facilities, structures that combine subscription finance (secured by uncalled capital) with NAV facilities (secured by the net asset value of the portfolio).

This evolution is driven by the need for liquidity later in the fund’s life. As capital is called and the uncalled capital commitments dwindle, the borrowing base for a traditional sub line shrinks. A hybrid facility allows the security package to transition from uncalled capital to asset value, providing a seamless liquidity solution throughout the fund’s lifecycle.

Furthermore, advancements in technology are streamlining the administration of these loans. Real-time reporting on investor creditworthiness and automated capital contributions tracking are reducing the administrative friction, making these facilities accessible even to smaller, emerging managers.

Conclusion: The New Operating Reality

In 2026, subscription finance is no longer a niche product; it is a fundamental component of the private capital infrastructure. For the investor, it offers a smoother cash flow experience. For the manager, it provides the flexibility and speed required to compete in a crowded market.

However, it is not a tool to be used passively. It requires active financial management, a deep understanding of credit ratings, and a strategic approach to investor relations. As the market grows toward the multi-trillion dollar mark, the funds that master the nuances of these credit facilities will be the ones that secure the best assets and deliver the most consistent returns.

The ability to generate recurring revenue and manage liquidity events with precision is what separates top-tier firms from the rest. Whether you are structuring a new fund or looking to optimise an existing vehicle, the integration of a robust subscription facility is a critical step in future-proofing your investment strategy.

Take the Next Step

Navigating the complexities of fund finance requires discreet, expert guidance. Whether you are exploring subscription finance for a new vintage, considering NAV lines, or seeking to amend existing credit facilities to better suit the 2026 market, professional advice is paramount.

Contact our specialist advisory team today to request a private consultation. We can help you outline suitable lenders, structure bespoke facilities, and ensure your liquidity strategy is aligned with your long-term goals.

FAQ: Subscription Finance Essentials

What is the difference between Subscription Finance and NAV Finance?

Subscription finance is secured by the uncalled capital commitments of the investors. It is typically used early in the fund’s life. NAV (Net Asset Value) finance is secured by the underlying assets of the fund and is typically used later in the lifecycle when the assets have accrued value and uncalled capital is low.

How does Subscription Finance affect the “J-Curve”?

By using a credit facility to delay capital calls, the fund can mitigate the initial negative returns often seen in the early stages of a fund (the J-Curve). This helps optimize the IRR in the early years.

Are these facilities risky for LPs?

Generally, they are considered low risk because they are secured by the LPs’ own commitments. However, LPs should be aware that in a default scenario, they are still obligated to pay their capital contributions to the lender.

Can Subscription Finance be used for funds investing in the Subscription Economy?

Yes. While the facility is secured by investor commitments, the fund can use the liquidity to invest in any asset class, including businesses with recurring revenue models. The stability of those revenues may influence lender comfort, but the primary collateral remains the LP commitments.