Private Credit Underwriting 2026: A Lender’s Perspective

In 2026, credit isn’t scarce, confidence is…

We have entered a market cycle defined by the “maturity wall.” A significant volume of debt originated during the low-interest era of 2020–2021 is coming due, facing a refinancing reality where base rates remain structurally higher than the previous decade. For finance decision-makers, the landscape of capital has shifted.

Banks, constrained by regulatory capital requirements and legacy portfolio issues, have retreated further from the middle market. Into this void steps private credit. However, the “growth-at-all-costs” mentality of the past has evaporated. Today, private credit underwriting is the filter through which all capital flows. It is no longer a box-ticking exercise; it is a forensic, bespoke discipline focused on durability and downside protection.

For a broader view of the macro forces shaping lender behaviour this year, see the credit market 2026 outlook

For borrowers and investors alike, understanding the mechanics of private credit underwriting is no longer optional, it is a strategic necessity.

What Is Private Credit Underwriting?

At its core, private credit underwriting is the process of assessing a borrower’s creditworthiness to determine the risk and viability of a private debt investment. Unlike the standardised, algorithmic underwriting often seen in public markets or traditional bank lending, private credit takes a fundamental, bottom-up approach.

The goal of private credit underwriting is not merely to approve a loan but to construct a highly specialised financial solution. It involves a deep dive into the borrower’s operations, market position, and asset base. The objective is to build a bespoke loan structure that delivers an acceptable risk-adjusted return for the investor while meeting the borrower’s specific needs for liquidity or growth capital.

For a deeper look at how deal assumptions are built before underwriting begins, see our guide on structured finance modelling.

In 2026, underwriting is a key determinant of success in private credit. It is the bridge between a borrower’s narrative and the lender’s balance sheet. It requires validating assumptions, stress-testing cash flow under various scenarios, and ensuring that the capital structure is resilient enough to withstand economic volatility.

Why Private Credit Underwriting is Vital to Success: The Unique Advantage

For sophisticated borrowers and intermediaries, understanding the underwriting process provides a distinct competitive edge. Deals rarely fall apart due to pricing disagreements; they fail because of underwriting mismatches, where the borrower’s presentation of risk does not align with the lender’s mandate for preservation of capital.

Strong underwriting is a key differentiator in direct lending. Lenders in 2026 are prioritising predictability over perfection. They are looking for borrowers who understand their own risks and have mitigated them.

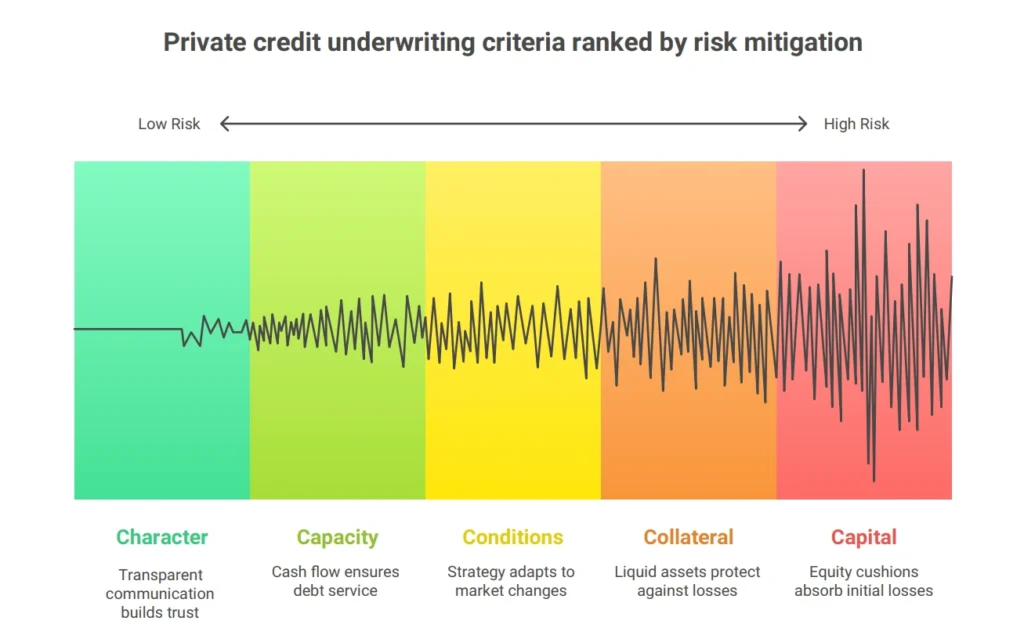

The 5 Cs of Credit in a 2026 Context

While the traditional “5 Cs of Credit” remain relevant, their application in private credit underwriting has evolved:

- Character: In the current economic environment, lenders scrutinise the track record of the sponsor or management team during the 2023–2025 volatility. Did they support the asset? Did they communicate transparently?

- Capacity: This is strictly about cash flow coverage. Can the business service higher debt costs without eroding working capital?

- Capital:Lenders demand significant “skin in the game.” Junior capital or equity cushions must be substantial to absorb first losses.

- Collateral: In a world of fluctuating valuations, the quality and liquidity of the underlying assets are paramount.

- Conditions: How does the investment strategy hold up against macroeconomic headwinds like inflation or geopolitical instability?

Real-World Scenarios: Underwriting Across the Asset Class

To understand how private credit underwriting functions practically, we must look at specific use cases. The approach varies significantly depending on the borrower profile and the investment product.

1. The Mid-Market Corporate Borrower

Consider a manufacturing firm seeking financing sources for an acquisition. A bank might reject the deal due to a temporary dip in EBITDA. A private credit lender, however, will underwrite the deal based on future order books and operational synergies.

- Underwriting Focus: The analysis centres on operating models, covenant headroom, and the sustainability of margins. The lender may structure a senior secured facility with a tighter definition of EBITDA but offer greater flexibility on amortisation.

2. The Real Estate Sponsor

A developer requires a bridge loan to refinance a prime commercial asset where the existing bank facility is maturing.

- Underwriting Focus: Here, due diligence targets valuation credibility and exit certainty. The underwriter assesses the loan terms against the asset’s ability to be sold or refinanced in 12–24 months. Risk management dictates that the lender focuses on the “as-is” value rather than speculative future value.

3. Private Equity and NAV Lending

A private equity firm seeks a Net Asset Value (NAV) loan to generate liquidity for a specific fund without selling assets in a down market.

- Underwriting Focus:This is a portfolio analysis. The lender evaluates the cross-collateralisation of the underlying companies. Diversification is key; the underwriter ensures that a failure in one portfolio company does not trigger a systemic default.

Why Rigorous Underwriting is Gaining Popularity

The surge in private credit is not accidental. As a traditional asset class, fixed income has faced challenges with yield and duration risk. Institutional investors and family offices are increasingly allocating to private debt, attracted by the floating-rate nature of the asset and the structural protections offered by robust underwriting.

However, credit losses in some corners of the market have highlighted that not all private credit is created equal. Investors now realise that underwriting is vital to private credit success. They are demanding transparency regarding how managers mitigate risk and how they value illiquid assets.

Furthermore, the secondary market for private credit is growing. For loans to be tradable, the initial credit underwriting must be impeccable. A loan with weak documentation or loose covenants will trade at a steep discount, damaging the lender’s reputation and the investor’s return.

Strategic Considerations for Borrowers and Investors

Whether you are seeking financing or investing in private credit strategies, the following considerations are essential for navigating the 2026 landscape.

For the Borrower:

- Pre-empt the Questions: Understand the lender’s risk lens: “What can go wrong, and who pays for it?” Present your financial obligations and cash flows conservatively.

- Structure Matters: Be open to creative structures. A first lien loan with a PIK (Payment in Kind) toggle might be more sustainable than a lower-rate loan with strict cash interest requirements.

- Transparency is Currency: In relationship-based origination, hiding bad news is fatal. Early disclosure allows the underwriter to structure around the problem. A complete, consistent, lender-ready data room is essential, and you can review the full checklist in our article on data room for lending.

For the Investor:

- Scrutinise the Manager: When selecting a private credit fund, look beyond the yield. Ask about their default and recovery rates. How large is their workout team?

- Diversify: Ensure your portfolio management strategy includes exposure to different sectors (e.g., corporate, real estate, asset-backed) to diversify risk.

- Covenant Discipline: Ensure the manager maintains strong underwriting standards and does not succumb to “covenant-lite” structures in a bid to deploy capital.

Conclusion: The Mindset Shift

The era of easy money is over. In 2026, private credit underwriting acts as the gatekeeper of capital allocation. For the lender, the underwriting is to ensure that the principal is protected and the return is commensurate with the risk. For the borrower, understanding this process is the key to unlocking liquidity in a constrained market.

Strong underwriting is a key determinant of success in private credit. It separates the tourists from the true practitioners. Those who respect the discipline of the process, providing clear data, realistic valuations, and coherent business plans, will find that private credit offers a flexibility and partnership that traditional banking cannot match.

As we navigate this cycle, the determinant of success in private credit will be the ability to look beyond the spreadsheet and understand the fundamental drivers of value and risk.

Ready to Discuss Your Capital Requirements?

Navigating the complexities of private credit underwriting requires expertise and discretion. If you require a confidential review of your capital plan or guidance on presenting a lender-ready underwriting case, we invite you to request a consultation.

Disclaimer: This content is for informational purposes only and does not constitute investment advice or an offer to sell any security or investment product. Investing in private credit involves risks, including the potential loss of principal. Always seek independent investment advice from a qualified professional regarding your specific financial situation.