Private Credit Trends 2026 – Why Discipline Matters Again

As we enter 2026, the global financial landscape has reached a definitive inflection point. For the past decade, private credit was often discussed as the “bright young thing” of alternative investments, a high-yielding alternative to anaemic fixed-income markets. However, the private credit trends 2026 reveals a market that has shed its adolescent volatility to become a core, institutionalised pillar of the global financial system, building on many of the private credit assumptions that underpinned the last decade of growth

For the C-suite, institutional investors, and ultra-high-net-worth individuals (UHNWIs), the narrative has shifted. The era of breakneck expansion and “growth at any cost” has been replaced by a more sober, sophisticated reality. In 2026, the defining characteristic of the private credit market is no longer just the volume of capital deployed, but the discipline with which it is managed.With a significant “maturity wall” looming from loans originated in the low-rate environment of 2021-2022, and the continued retreat of traditional banks and private credit entities forming new alliances, the private credit outlook for the year ahead demands a more nuanced understanding of risk, structure, and manager selection.

The Private Credit Outlook for 2026: From Expansion to Maturation

The private credit trends in 2026 have matured into an asset class exceeding $1.5 trillion globally. Yet, the headline growth figures mask a deeper structural change: the Great Bifurcation. In 2026, this bifurcation is no longer theoretical: experienced managers are actively restructuring capital stacks and controlling outcomes, while weaker platforms are discovering, often too late, that yield alone does not compensate for poor underwriting or structural fragility.

A Core Component of Private Capital

Private capital is no longer a peripheral consideration for a balanced portfolio. Institutional investors now view private credit as a permanent fixture of the capital structure, often replacing traditional high-yield bonds or syndicated loans. As we head into 2026, the debt market has become more fragmented but also more specialised.The 2026 outlook suggests that while the growth of private credit remains positive, the pace has stabilised. The focus has moved from simply gaining access to private credit to ensuring that the credit quality of the underlying private companies remains resilient against a backdrop of persistent inflationary pressures and geopolitical shifts.

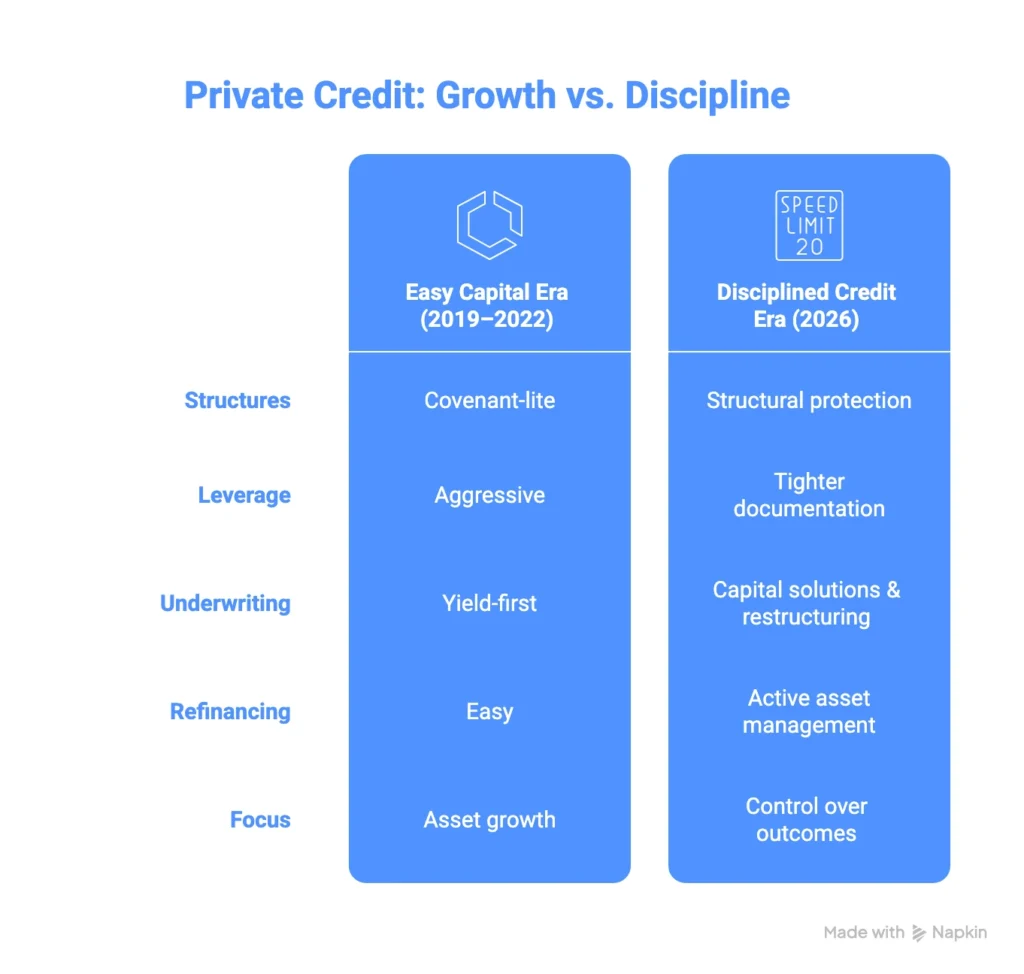

Why Discipline Matters Again in Credit Markets

For several years, the private credit industry was characterised by “borrower-friendly” terms. Covenant-lite structures and aggressive leverage multiples were common as lenders competed to deploy record levels of “dry powder.”

In 2026, the pendulum has swung back. Discipline is the watchword for the following reasons

- The End of Easy Refinancing: The private credit trends market is currently navigating a massive wave of refinancings. Loans issued during the 2021 peak are reaching maturity. Private credit lenders are no longer willing to “extend and pretend” without significant equity injections or structural enhancements.

- Underwriting Integrity: The ability to underwrite complex risks has become a competitive advantage. In 2026, private credit firms that relied on broad market beta are struggling, while those with deep sector expertise and rigorous underwriting standards are thriving.

- The Return of Covenants: We are seeing a resurgence of “maintenance covenants” which provide private lenders with early warning signs of borrower distress, allowing for proactive capital solutions rather than reactive liquidations.

Key Private Credit Trends 2026: What is Driving the Market?

To understand the private credit trends 2026, one must look beyond simple direct lending. The market has diversified into a sophisticated ecosystem of credit strategies.

1. The Rise of Opportunistic Credit and Capital Solutions

As traditional banks continue to retrench due to regulatory capital constraints, a gap has emerged for opportunistic credit. This isn’t just “distressed” debt; it is the provision of bespoke capital solutions for high-quality companies facing temporary liquidity hurdles or complex transition periods. Private credit trends 2026 provide the flexibility that the syndicate market cannot match.

2. Credit Secondaries: Providing Liquidity

One of the most significant private credit trends 2026 is the explosion of the credit secondaries market. As institutional investors seek to rebalance their private market exposure or manage liquidity, the ability to trade LP (Limited Partner) interests in private credit funds has become essential. This has added a layer of maturity and liquidity to the asset class that was previously absent.

3. Asset-Based Finance (ABF)

The private credit outlook is increasingly focused on asset-based lending. Moving away from pure cash-flow lending, private credit asset managers are looking at the balance sheet, financing everything from equipment and inventory to intellectual property and receivables. This provides an additional layer of downside protection for the investor.

The Shift Toward Bespoke Capital Solutions and Restructuring

As we enter 2026, the “maturity wall” is the most significant tactical challenge facing the corporate credit sector. A substantial volume of debt is due for renewal, often at rates 400-500 basis points higher than when the debt was originally struck.

Refinancing and Rescue Capital

Private credit has become the primary source of rescue capital. When a middle market company cannot access the capital markets or their existing lender is unwilling to increase exposure, private credit managers step in with preferred equity or junior debt structures. These credit opportunities allow companies to bridge the gap to a more stable economic environment without undergoing a formal insolvency process.

Partnering with Private Lenders

We are seeing a trend of “partnership lending.” Rather than a purely adversarial relationship, borrowers are partnering with private credit platforms that offer more than just cash. They offer strategic advice, industry connections, and a long-term view of the investment cycle. This is particularly prevalent in European private credit, where the relationship-driven model remains dominant.

Private Wealth and the Institutionalisation of the Asset Class

A major driver of the growth of private credit in 2026 is the influx of capital from private wealth investors. High-net-worth individuals and family offices are increasingly moving away from volatile public equities into semi-liquid private credit vehicles.

The Rise of Semi-Liquid Funds

New structures, such as the European Long-Term Investment Fund (ELTIF 2.0) and the Long-Term Asset Fund (LTAF) in the UK, have democratised access to private credit. These credit vehicles offer monthly or quarterly liquidity windows, making them attractive to private wealth portfolios that require a balance between yield and accessibility.

However, this trend brings its own set of risks. Private credit managers must be disciplined in how they manage the liquidity mismatch between the underlying long-term loans and the redemption requests of private wealth investors. In 2026, the regulatory reality check is focused heavily on the transparency and valuation practices of these retail-facing private funds.

Real-World Scenario: Navigating the 2026 Maturity Wall

Consider a mid-sized European technology firm that took out a €200 million direct lending facility in 2021 at Euribor + 5.5%. In 2021, their interest expense was manageable. By 2026, with Euribor significantly higher, their debt service coverage ratio (DSCR) has tightened.

In the previous cycle, this company might have struggled to find a lender. In the 2026 private credit outlook, a disciplined private credit platform would approach this through a capital solution:

- Structure: Converting a portion of the cash interest to PIK (Payment-in-Kind) to preserve cash flow.

- Protection: Taking a preferred equity stake to capture upside while maintaining seniority in the capital structure.

- Discipline: Requiring the founders to inject fresh equity, ensuring alignment of interests.

This scenario illustrates how private credit provides a safety valve for the economy, preventing a wave of bankruptcies through intelligent, disciplined restructuring.

Banks and Private Credit: Competition or Collaboration

One of the most misunderstood private credit trends 2026 is the relationship between traditional banks and private credit. While the media often portrays them as rivals, the reality is one of increasing collaboration.

The “Synthetic” Partnership

Banks are increasingly using private credit to manage their own balance sheet constraints. Through “Significant Risk Transfer” (SRT) transactions, banks can move the risk of their loan books to private credit investors without losing the client relationship.

Furthermore, many banks have established their own private credit arms or entered into joint ventures with established private credit firms. This allows the bank to originate the deal (using its vast branch network) while the private credit fund provides the capital. This hybrid model is a key feature of the direct lending market in 2026.

Risk Management: Addressing the Lagging Default Signals

While the private credit industry has proven remarkably resilient, 2026 is the year where “underlying stress” can no longer be ignored. Reported default rates in private credit portfolios often appear lower than in the public high-yield market.

Sophisticated investors understand that contained default statistics often reflect active liability management, extensions, PIK toggles, and quiet restructurings, rather than the absence of underlying stress.. A “default” in private credit often results in a quiet restructuring or a “work-out” rather than a public bankruptcy filing.

Valuation Discipline

In 2026, there is intense scrutiny on how asset managers value their private assets. The private credit trends 2026 show a move toward third-party, independent valuations to ensure that the Net Asset Value (NAV) of credit funds accurately reflects the market conditions. For the investor, understanding the manager’s valuation methodology is as important as understanding their investment strategy.

What Investors and Borrowers Should Consider in 2026

For those navigating the private credit market in 2026, several strategic considerations are paramount:

For Investors (HNWIs and Family Offices)

- Vintage Risk: Be mindful of the “2021-2022 vintage.” These loans were struck at the top of the market. Focus on managers who are deploying fresh capital into the 2026 outlook environment, where terms are more favourable to the lender.

- Manager Experience: In a bull market, everyone looks like a genius. In 2026, prioritise private credit managers who have lived through multiple credit cycles (2008, 2012, 2020).

- Diversification: Move beyond simple direct lending. Look at opportunistic credit, credit secondaries, and asset-backed strategies to build a resilient portfolio.

For Borrowers and C-Suite Executives

- Proactive Engagement: Do not wait for the maturity wall to hit. Engage with private credit lenders early to discuss capital solutions.

- Flexibility over Price: In 2026, the “cheapest” capital is often the most restrictive. The flexibility offered by private credit, such as PIK options or delayed-draw credit facilities, can be more valuable than a lower interest rate in the long run.

- Transparency: Private credit firms are more intrusive than banks. Be prepared to share detailed operational data and maintain a high level of transparency regarding the balance sheet.

Conclusion: A More Disciplined Phase of Private Credit

As we look at the private credit trends 2026, it is clear that the asset class has entered its “adult” phase. The frantic dash for assets has been replaced by a calculated, structural approach to lending.

Discipline matters again because the margin for error has narrowed. Higher interest rates, geopolitical uncertainty, and the sheer scale of the private credit market mean that only the most diligent lenders and the most resilient borrowers will thrive.

For the sophisticated investor, 2026 offers a compelling opportunity. The private credit outlook is one where the “complexity premium”, the extra return earned for structuring difficult deals, is at its highest in a decade. In 2026, returns will be driven less by asset growth and more by control, structure, documentation, and the ability to intervene early when capital structures come under pressure.

The next phase of the credit cycle will not be defined by who can lend the most, but by who can lend the smartest. In 2026, discipline is not just a virtue; it is the ultimate competitive advantage.

Engaging in the Next Phase of Credit

The landscape of private credit in 2026 requires more than just capital; it requires a strategic partner who understands the nuances of the current debt market. Whether you are an institutional investor seeking to rebalance your private capital allocation or a corporate leader navigating a complex capital structure, the importance of expert guidance cannot be overstated.

For those navigating the complexities of the 2026 private credit outlook, the path forward is defined by bespoke solutions and discreet, off-market opportunities.

Contact us today to discuss how a disciplined approach to private credit and capital solutions can support your strategic objectives in 2026 and beyond.