Luxury Yacht Financing: Loan Options & Market Trends 2025

For high-net-worth individuals (HNWIs) and C-suite executives, financing a yacht represents a significant investment, often symbolising both a personal achievement and a strategic asset. However, the substantial capital outlay required for such a purchase necessitates careful financial planning. This comprehensive guide explores the intricacies of luxury yacht financing, providing insights and strategies tailored to a sophisticated financial audience, helping them navigate the complexities and optimize their investment. We’ll cover everything from traditional boat loans to more specialized financing structures, empowering you to make informed decisions that align with your overall financial strategy.

Understanding the Landscape of Luxury Yacht Financing

The luxury yacht financing market is a specialised niche within the broader luxury asset lending space. Unlike conventional auto loans or residential mortgages, yacht loans involve significantly larger sums, more complex due diligence, and deeper expertise in valuing non-standard assets.

According to The Business Research Company, the global yacht market, including both sailing and motor yachts under 24 meters — was valued at approximately USD 9.06 billion in 2024 and is projected to reach USD 9.48 billion by 2025, growing at a compound annual growth rate (CAGR) of 4.7%. While these vessels are often financed through traditional marine lenders, loans at the luxury end still require bespoke structuring.

Lenders in the luxury yacht segment assess far more than just creditworthiness. They consider depreciation, operating costs, resale liquidity, and even flagging or registration issues. A high-value vessel may hold prestige, but from a lender’s perspective, it must retain collateral value and remain viable throughout the loan term.

Why Finance Instead of Paying Cash?

Luxury yacht financing allows buyers to preserve liquidity for other investments or unforeseen expenses. Choosing to fund a superyacht instead of paying cash can be a strategic move, especially given current market trends. In 2025, the new luxury vessel market is expected to see continued price increases, while the used boat market may experience slight price reductions due to increased inventory availability. These fluctuations highlight the importance of securing favorable loan terms to mitigate potential pricing volatility.

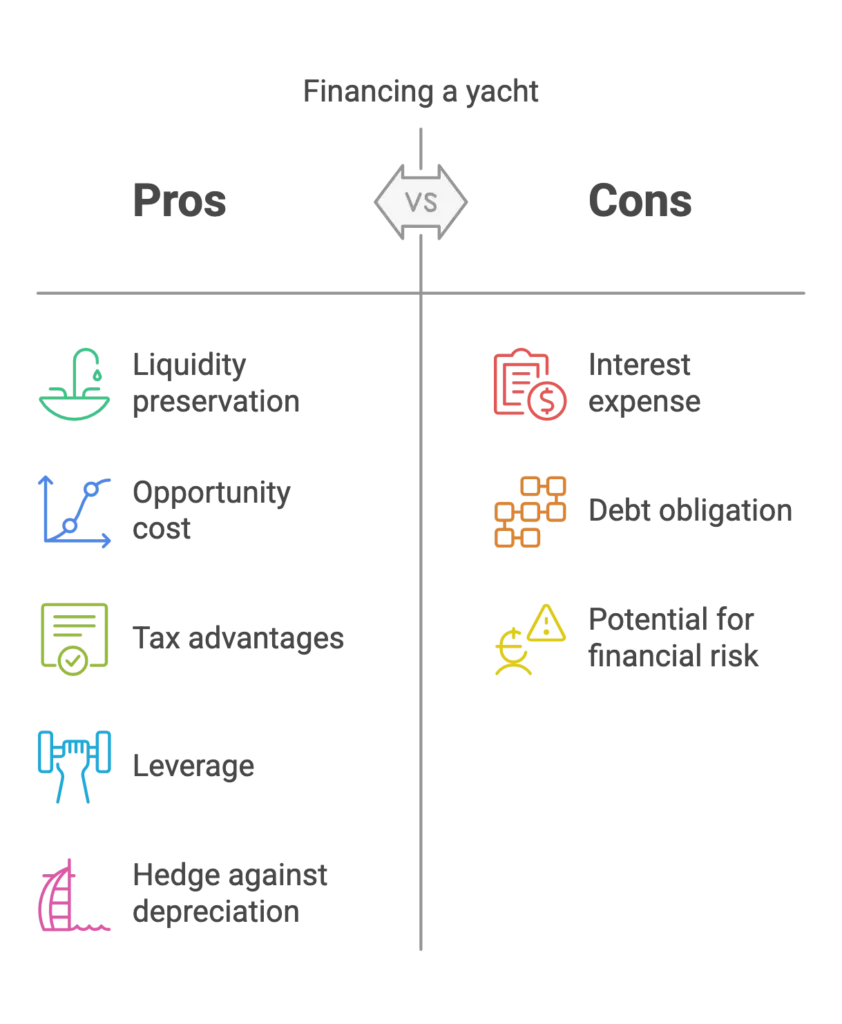

While HNWIs may have the liquid assets to purchase a vessel outright, financing a luxury yacht often presents a more strategically advantageous approach. Several key reasons support this:

- Liquidity Preservation: Tying up a significant portion of capital in a single asset can limit investment opportunities and reduce financial flexibility. Borrowing allows you to retain liquidity for other ventures, potentially generating higher returns than the cost of the loan.

- Opportunity Cost: The capital preserved by lending can be deployed in other investments, such as securities, real estate, or business ventures, potentially yielding higher returns than the interest expense on the loan.

- Tax Advantages: In certain jurisdictions, and under specific conditions, the interest paid on luxury yacht financing may be tax-deductible. If the vessel qualifies as a “second home” (possessing a berth, head, and galley), the interest on the loan can potentially be deducted, similar to a traditional home mortgage. In the US, the IRS currently allows deductions on interest for up to $750,000 of mortgage debt for combined first and second homes. If it is used for business purposes, further deductions may be available, such as depreciation.

- Leverage: Borrowing allows you to leverage your existing assets to acquire a larger or more luxurious model than might be possible with a cash purchase.

- Hedging against depreciation: Luxury vessels, like many illiquid luxury assets, can depreciate. Borrowing a portion of the purchase allows to preserve capital in other appreciating assets.

Exploring Luxury Yacht Financing Options

Luxury yacht financing isn’t one-size-fits-all. Several funding structures exist, each tailored to different ownership goals, vessel types, and borrower profiles. Understanding how these structures work is key to selecting the right fit, whether you’re acquiring a new luxury yacht, refinancing an existing one, or unlocking equity from a high-value vessel.

While the broader yacht market is growing steadily, the superyacht segment, typically vessels over 24 meters, is seeing even more aggressive expansion. According to Coherent Market Insights, the global superyacht market is projected to reach USD 21.60 billion by 2025 and USD 45.16 billion by 2032. This rising demand is driving innovation in financing structures, making flexible and asset-sensitive lending options more critical than ever.

1. Traditional Yacht Loans (Marine Mortgages)

A traditional yacht loan, often referred to as a marine mortgage, is a secured loan where the vessel serves as collateral, similar in structure to a home mortgage. These loans are widely used for new and pre-owned luxury yachts and are typically offered by banks, marine lenders, and some specialist finance providers.

- Interest Rates: Fixed and variable options are available. As of 2025, competitive rates start around 6.49%, depending on credit profile, vessel age, and loan term. Fixed-rate structures offer predictable repayments, while variable rates may carry initial savings with the risk of future increases.

- Loan Terms: Standard terms range from 10 to 20 years, with some lenders extending up to 25 years for larger yachts.

- Down Payment: Expect to put down 10% to 20% of the purchase price. Larger down payments can improve the annual percentage rate (APR) and reduce financing risk.

- Credit Profile Requirements: Most lenders will require a strong credit history, with prime rates typically reserved for applicants with excellent credit. While some lenders may consider applicants with lower scores or less conventional profiles, weaker credit may result in higher interest rates or stricter terms.

- Debt-to-Income Ratio (DTI): Many lenders require a DTI ratio of 35% or less to qualify, ensuring repayment capacity alongside existing liabilities.

Advantages:

- Predictable repayment schedules with fixed-rate options

- Generally lower interest rates than unsecured lending

- Long repayment horizons ease monthly cash flow impact

Considerations:

- The yacht secures the loan, meaning repossession is possible in case of default

- Down payments are typically required upfront

- The underwriting process can be detailed, especially for high-value vessels

2. Specialist Marine Lenders

These lenders operate exclusively within the marine sector and are well-versed in the nuances of luxury yacht financing. Their deep understanding of the luxury yacht market allows them to tailor lending terms to the vessel type, usage, and borrower profile, often beyond the risk appetite or capacity of mainstream banks.

Benefits:

- Extensive expertise in valuing high-end and custom vessels

- Potentially more flexible lending structures and covenants

- Faster underwriting and approval processes

- Willingness to finance older, refurbished, or one-off craft

- Access to specialist guidance and aftercare, including insurance and maintenance finance solutions

Drawbacks:

- May charge a premium in interest due to niche focus

- Some lenders may require higher deposits, particularly on specialised or non-standard yachts

3. Secured Loans Against Other Assets

HNWIs often possess substantial assets, such as investment portfolios, real estate holdings, or even art collections. These assets can be used as collateral for a secured loan, providing the funds to purchase the yacht.

Benefits:

- Potentially lower rates than unsecured loans.

- May allow for larger loan amounts.

- Avoids using the yacht as direct collateral.

Drawbacks:

- Requires pledging valuable assets as collateral.

- The financier can seize the pledged assets if you default on the loan.

4. Unsecured Loans

While less common for large purchases, unsecured loans are an option, particularly for smaller vessels or for borrowers with exceptionally strong credit profiles.

Benefits:

- No collateral required.

- Faster approval process.

Drawbacks:

- Significantly higher rates.

- Smaller loan amounts.

- Requires an excellent credit history.

5. Maritime Leasing and Charter Management Programs

- Leasing: Maritime leasing provides an alternative to outright ownership, offering lower upfront costs and fixed monthly payments over a set period.

- Charter Management Programs: These programs allow you to offset some of the ownership costs by chartering the vessel when you’re not using it. The charter income can help cover loan payments, maintenance, and other expenses.

Benefits:

- Lower initial investment.

- Potential to generate income through chartering.

- Reduced maintenance responsibilities (in some charter programs).

Drawbacks:

- You don’t own the asset outright (in leasing).

- Limited personal use (in charter programs).

- May not be the most cost-effective option in the long run.

6. Balloon Payment Structures

Some yacht loans are structured with a balloon payment, a large final repayment due at the end of the term. This arrangement reduces monthly obligations during the term, freeing up liquidity, but demands disciplined financial planning to cover the lump sum at maturity.

Benefits:

- Lower monthly payments throughout the loan term

- Frees up cash flow for other investments or expenses

- May facilitate the purchase of a larger or more desirable yacht

Drawbacks:

- Large final payment requires advance planning or refinancing

- Risk of needing to sell the yacht or refinance under pressure if liquidity is unavailable

- May incur higher total interest costs depending on the structure

7. Refinancing a Luxury Yacht

Refinancing allows yacht owners to restructure their existing loan, typically to secure a lower rate, change the term, or release equity. This can be a strategic move if market conditions improve or personal financial circumstances shift.

Benefits:

- Potential to reduce monthly repayments through lower interest rates

- Opportunity to shorten loan duration and pay off the yacht faster

- May allow equity release for other financial priorities

- Can improve overall financing efficiency if original loan terms were unfavourable

Drawbacks:

- May involve fees, valuation costs, or early repayment penalties on the existing loan

- Approval depends on current yacht value, condition, and marketability

- Interest rate savings can be eroded if refinancing is not well-timed

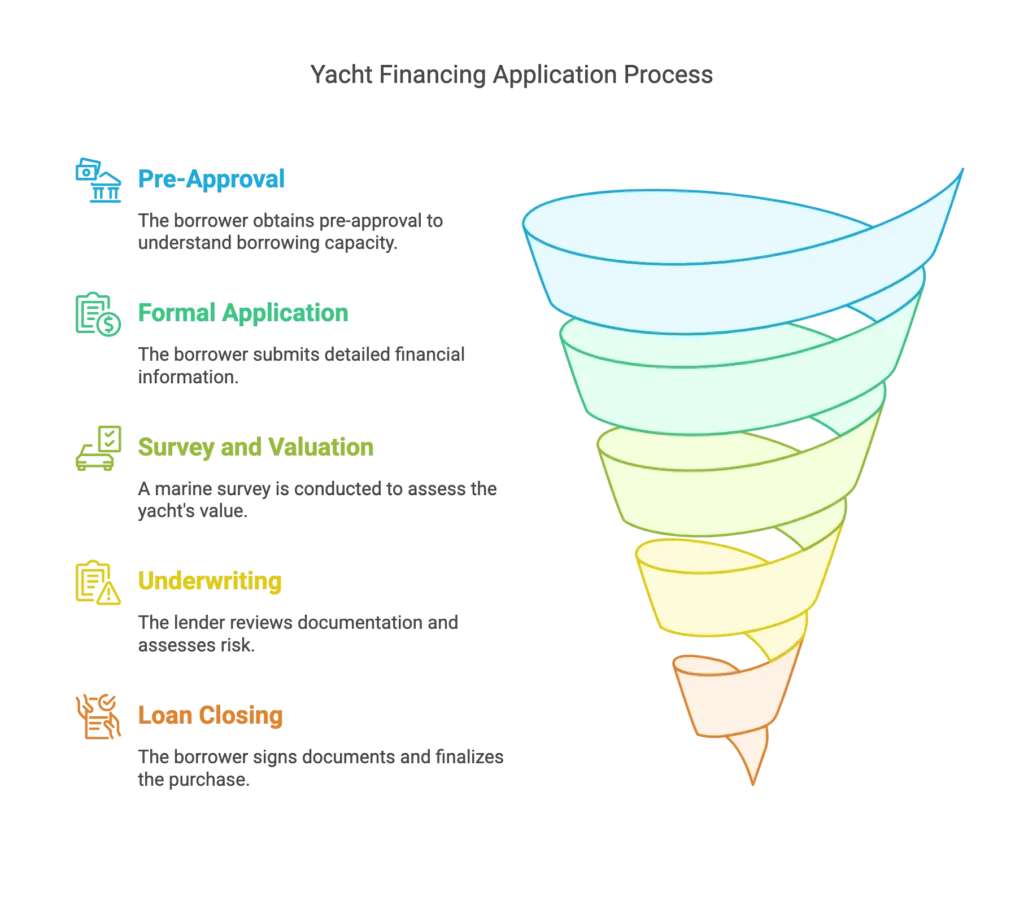

What to Expect During the Luxury Yacht Financing Application Process

The luxury yacht financing application process is generally more rigorous than for smaller loans. An internal appraiser will conduct thorough due diligence, assessing both the borrower’s financial profile and the yacht itself.

Key Steps:

- Pre-Approval: It’s highly recommended to get pre-approved for a loan before seriously shopping. Pre-approval gives you a clear understanding of your borrowing capacity and strengthens your negotiating position with sellers.

- Application: The formal application will require detailed financial information, including:

- Personal financial statements.

- Tax returns (typically for the past two to three years).

- Proof of income and assets.

- Credit history.

- Details about the model (brand, year, purchase price).

- Survey and Valuation: For used boats, and often for new builds, financiers will require a marine survey by accredited surveyors to assess the vessel’s condition and value. This is a crucial step to ensure the craft is worth the loan amount.

- Underwriting: The underwriting team will review all the submitted documentation and assess the risk of the loan.

- Loan Closing: Once approved, the loan closing process involves signing the loan documents and finalizing the purchase.

Key Lending Benchmarks for Luxury Yacht Financing

- Loan-to-Value (LTV) Ratio: This is the ratio of the loan amount to the yacht’s appraised value. Finance companies typically prefer LTV ratios of 80% or less, meaning you’ll need a down payment of at least 20%.

- Debt-to-Income (DTI) Ratio: Your DTI will be assessed to ensure you can comfortably afford the loan payments along with your other financial obligations.

- Liquidity Requirements: Funders want to see that you have sufficient liquid assets to cover the down payment, closing costs, and ongoing operating expenses of the yacht.

- Insurance: Comprehensive marine insurance is mandatory for yachts loans.

- Running costs: The costs of operating the yacht which include hiring a crew, are likely to cost around 10% of the yacht’s value annually. These aren’t covered, so one needs to comfortably cover them in addition to the loan repayments.

- Tax Implications: Consult with your tax advisor to understand the potential tax deductions and implications.

- Legal Advice: Seek counsel from a maritime lawyer on the best option for ownership, funding options and registration.

Inside the Deal: Leveraging Luxury Asset Lending for Yacht Acquisition

A high net worth individual (HNWI) is interested in purchasing a 150-foot super yacht valued at $30 million. After consulting with their financial advisor, they decide to pursue their funding options, and preserve liquidity for other investment opportunities.

- Option 1: Traditional Marine Mortgage: The HNWI secures a marine mortgage with a 20% down payment ($6 million) and a 15-year term at a fixed interest rate of 7.5%. This results in monthly payments of approximately $222,457.

- Option 2: Secured Loan Against Investment Portfolio: The HNWI pledges a portion of their investment portfolio as collateral for a secured loan. They obtain a loan for $24 million at a lower interest rate of 6% due to the strong collateral. This results in lower monthly payments compared to the marine mortgage.

- Option 3: Combination Approach: The HNWI decides to combine a smaller marine mortgage with a secured loan against their investment portfolio. This allows them to minimise the down payment on the marine mortgage while still benefiting from a lower overall interest rate.

The HNWI, in consultation with their financial and legal advisors, carefully evaluates each option, considering the interest rates, terms, tax implications, and the impact on their overall financial strategy. They ultimately choose the combination approach, optimising their liquidity and leveraging their existing assets.

Conclusion: Charting a Course to Yacht Ownership

Luxury yacht financing can provide a powerful tool for HNWIs and decision-makers to acquire their dream vessel while maintaining financial flexibility and optimizing their investment strategy. By understanding the various lending options, the application process, and the key considerations involved, you can navigate the complexities of customized yacht financing with confidence.

Actionable Insights for Decision-Makers:

- Consult with Financial Professionals: Engage your financial advisor, tax advisor, and a maritime lawyer to discuss your specific needs and develop a tailored financing strategy.

- Get Pre-Approved: Obtain pre-approval for a loan to understand your borrowing capacity and strengthen your negotiating position.

- Compare Multiple Offers: Don’t settle for the first offer you receive. Compare rates, terms, and fees from multiple lenders.

- Factor in All Costs: Consider not only the purchase price but also the ongoing operating expenses, including insurance, maintenance, crew, and dockage.

- Negotiate: Don’t be afraid to negotiate the loan terms and the purchase price.

- Understand Loan To Value: A LTV of 80% or lower is achievable.

By taking a proactive and informed approach to funding, you can transform your dream into a reality while making sound financial decisions that align with your long-term goals

Next Steps

Ready to navigate the complexities of owning a luxury yacht? Contact our team today to explore tailored funding solutions that align with your financial goals and make your dream of ownership a reality. Currently serving clients across UK, Europe & Asia-Pacific

🧠 Want to hear others’ take on luxury yacht financing? Listen to this deep dive for the highlights. 🎙️ Listen here