Classic Car Financing: Retain Ownership, Unlock Equity in 2025

Classic Car Financing Secrets: What Lenders Don’t Tell Vintage Collectors

The gleam of polished chrome, the evocative scent of aged leather, the resonant growl of a finely-tuned engine – for high-net-worth individuals (HNWIs), investors, and C-suite executives, a classic car is often far more than a mere vehicle. It’s a passion, a piece of history, an appreciating asset. But what if that 1960s Ferrari, that pre-war Bugatti, or that iconic Porsche could do more than adorn a collection? What if it could unlock significant liquidity, fund your next strategic acquisition, or enhance portfolio flexibility—all without ever leaving your climate-controlled garage? Welcome to the discreet world of classic car financing, a sophisticated financial tool that many collectors, and indeed many traditional lenders, know little about.

The market for classic cars has seen remarkable appreciation over the past two decades, transforming these automotive masterpieces into a recognised alternative asset class. As their values have soared, so too has the interest from specialized finance providers and private banking desks. In a financial landscape where liquidity is paramount and traditional credit lines can be restrictive based on credit score, understanding how to leverage these high-value passion assets is no longer a niche curiosity but a strategic imperative. This isn’t about a standard car loan; this is about bespoke, asset based financing options designed for the discerning collector car owner.

Unveiling Classic Car Financing: Beyond the Standard Auto Loan

At its core, classic car financing (often referred to as classic car finance) involves securing a loan using one or more classic cars or vintage cars as collateral. However, to equate this with a typical auto loan sourced from a high-street bank or credit union for a daily driver would be a fundamental misunderstanding. The world of financing classic cars operates on a different plane, tailored to the unique nature of these assets and the sophisticated needs of their owners.

Key Characteristics of Bespoke Classic Car Financing:

- Asset-Backed, Not Just Credit-Score Dependent: While a strong credit history is always beneficial, the primary security for these facilities is the classic car itself. Lenders in this space are experts in valuation and the nuances of the collector car market.

- Higher Loan-to-Value (LTV) Ratios: Compared to art or other passion assets, classic cars can sometimes command more favorable LTV ratios, often ranging from 50% to 70% of the appraised value, depending on the vehicle’s rarity, provenance, condition, and market desirability.

- Specialized Appraisal Process: Determining the true vehicle value of a collectible vehicle is an art and a science. Lenders specializing in classic car finance work with renowned appraisers who understand auction trends, private sale data, and the specific factors that influence a top classic car‘s worth. This goes far beyond a standard blue book valuation used for a new car or regular used car.

- Bespoke Loan Structures and Flexible Terms: These are not off-the-shelf products. Loan terms, repayment schedules (monthly payment structures, interest-only options), and even currency options can often be tailored. The goal is to provide liquidity that aligns with the borrower’s broader financial strategy, not just a simple loan for your dream car.

- Provider Landscape: You won’t typically find these classic car financing options advertised alongside mortgages or standard business loans. They are usually offered by:

- Specialty Finance Companies: Firms dedicated to luxury asset lending.

- Private Banks: Many private banking arms catering to UHNWIs have desks that can structure such deals.

- Private Lenders & Family Offices: Smaller, more agile players who understand niche assets.

- Specialist Brokers: Intermediaries who connect collectors with the right len

The loan process for classic car financing is more involved than a standard auto loan application process. It requires detailed documentation of the vehicle (provenance, restoration records, insurance policy), a thorough valuation, and a clear understanding of the borrower’s financial standing and objectives. However, for the right client and the right asset, it unlocks financial power previously dormant.

Classic Car Financing: The Hidden Advantage for Asset-Rich Clients

The realm of high-value classic car financing remains relatively opaque for several compelling reasons, creating an “insider” advantage for those in the know.

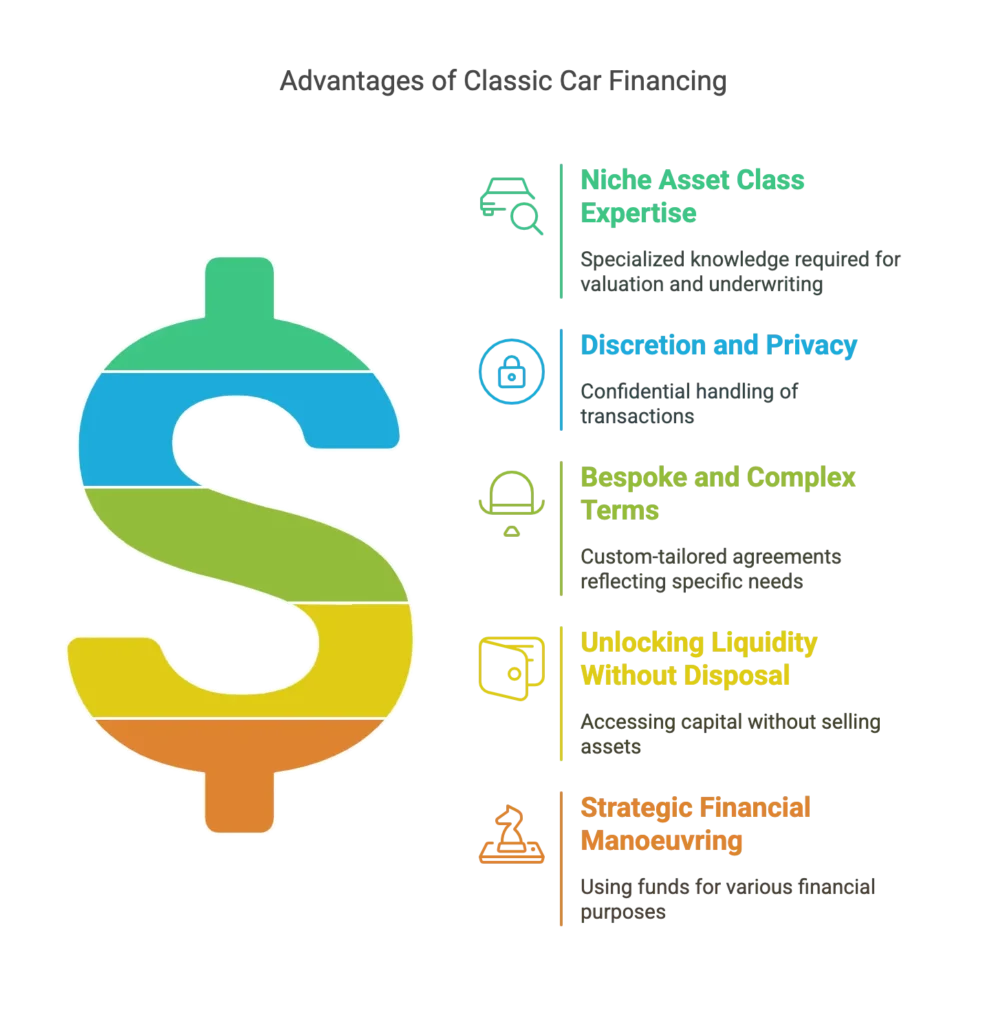

- Niche Asset Class Expertise: Traditional lenders often lack the specialized knowledge to accurately value and underwrite loans against classic cars. The volatility, subjectivity, and unique risk factors (storage, maintenance, authenticity) of collectible vehicles require a depth of understanding that mainstream institutions rarely possess. This is why a standard auto loan provider might shy away from a multi-million-dollar vintage Ferrari, whereas a specialist lender sees a prime collateral opportunity.

- Discretion and Privacy: HNWIs and family offices value discretion above all. The providers of bespoke classic car finance understand this implicitly. Transactions are handled with confidentiality, far from the public disclosures sometimes associated with other forms of financing. This isn’t about flashing a new purchase financed via a dealership; it’s about strategic capital management.

- Bespoke and Complex Terms: Each classic car loan of this nature is essentially a custom-tailored agreement. There’s no standardised calculator or one-size-fits-all application process. The terms reflect the specific vehicle(s), the borrower’s needs, and the lender’s risk appetite. This complexity naturally limits widespread understanding and access.

- Unlocking Liquidity Without Disposal: Perhaps the most significant advantage is the ability to access substantial capital without selling cherished assets. Selling a prized classic car can trigger significant capital gains taxes, involve hefty auction fees, and mean parting with an irreplaceable piece of a collection. Classic car financing allows owners to retain ownership and enjoyment of their dream classic car while putting its inherent value to work.

- Strategic Financial Manoeuvring: The funds unlocked can be used for a multitude of purposes:

- New Investments: Seizing opportunities in real estate, private equity, or other ventures.

- Business Capital: Injecting liquidity into operating businesses.

- Portfolio Diversification: Rebalancing assets without forced sales.

- Estate Planning: Providing liquidity for estate management purposes.

- Acquiring More Collector Cars: Expanding the collection strategically.

- Short-Term Bridging: Covering financial gaps until other assets mature or are

Understanding these nuances is key to leveraging classic car finance effectively. It’s about recognising that the capital tied up in your garage isn’t “idle”—it’s a potent financial resource waiting to be strategically deployed.

Real-World Scenarios: Strategic Liquidity in Action

To illustrate the power of classic car financing, consider these sophisticated, albeit anonymised, applications:

- Scenario 1: The Property Developer’s Aston Martin

An established property developer, a keen car enthusiast, identified a time-sensitive opportunity to acquire a prime parcel of land for a luxury residential project. Traditional bank finance was proving too slow, with cumbersome due diligence threatening the deal. By leveraging his pristine 1963 Aston Martin DB5 (a highly desirable collectible), he secured a £2 million bridging loan from a specialty lender within three weeks. The loan terms were structured as interest-only for 12 months, allowing him to secure the land and commence initial planning. The classic car financing provided the crucial speed and flexibility that conventional lending could not. - Scenario 2: The Family Office’s Multi-Car Collateral for a PE Co-Investment

A multi-generational family office sought to co-invest in a promising private equity fund focused on sustainable technology. Rather than liquidating existing equity holdings and incurring capital gains, they opted to collateralise a portion of their significant classic car collection, which included several post-war European sports cars, each a collectible vehicle in its own right and collectively valued at over $15 million. A private bank, familiar with their overall wealth profile, structured a revolving line of credit against the collection. This provided the necessary capital for the PE investment while allowing the family to maintain their strategic market positions and enjoy their dream classic cars. The LTV was negotiated based on the diversity and quality of the collection, and the interest rates tend to be competitive for such bespoke facilities. - Scenario 3: The Art Collector’s Blended Asset Loan

An internationally recognised art collector wished to acquire a significant contemporary sculpture but preferred not to sell existing artworks. She also owned a rare, concours-condition 1955 Mercedes-Benz 300SL Gullwing, a vintage car with impeccable provenance. A boutique finance firm, specializing in luxury asset lending, structured a “blended asset” loan, collateralising both the Gullwing and a selection of her blue-chip art. This innovative approach to financing classic cars and other passion assets allowed for a larger loan amount and more favorable terms than if only one asset class had been used. The valuation process was meticulous for both asset types, ensuring the lender was comfortable with the combined collateral.

These scenarios underscore that classic car financing is not merely about borrowing money; it’s a sophisticated tool for strategic financial management, enabling HNWIs to achieve diverse objectives without disrupting their core investment portfolios or parting with prized possessions.

The Rising Tide of Classic Car Financing: Why It’s Gaining Momentum

The increasing prominence of classic car financing as a strategic tool for HNWIs isn’t accidental. Several converging factors are driving its popularity:

- Sustained Appreciation of Classic Car Values: The classic car market has demonstrated robust growth over the past two decades, with many models significantly outperforming traditional investments. This sustained appreciation has solidified their status as a legitimate alternative asset class, making lenders more comfortable with their valuation and long-term value retention. Vehicles that are 25 years or older and well-maintained often see significant value increases.

- HNWI Appetite for Liquidity Without Asset Disposal: In an economic climate that prizes liquidity and flexibility, HNWIs are increasingly seeking ways to unlock capital from their existing assets without resorting to outright sales. The desire to avoid capital gains taxes, maintain ownership of passion assets, and respond nimbly to investment opportunities fuels demand for solutions like classic car finance.

- Innovation Among Private Lenders: The private credit market has become increasingly sophisticated. Specialty lenders and private banks are actively developing creative financing options for luxury assets. They possess the expertise to assess the unique risks and rewards associated with collectible vehicles and are willing to structure bespoke deals that traditional banks might avoid. They understand that owning a classic can be a significant store of value.

- Shift Towards Alternative Credit Strategies: Post-2008 financial crisis, and more recently post-COVID, traditional bank lending has, in some areas, become more constrained by regulation and risk aversion. This has opened the door for alternative credit providers who can offer more flexible and tailored loan solutions, including those backed by non-traditional collateral like classic cars.

- Increased Transparency and Professionalism in the Classic Car Market: The classic car market itself has matured. Major auction houses like RM Sotheby’s and Gooding & Company, along with resources like Hagerty‘s valuation tools, provide greater transparency in pricing and trends. This increased market professionalism gives lenders more confidence in the underlying collateral.

This confluence of factors suggests that the strategic use of classic car financing will continue to grow, offering sophisticated collectors a powerful, yet discreet, financial lever.

Classic Car Financing: Nuances Every Collector Should Know

Classic car loans offer attractive benefits, but they come with specific conditions collectors must understand.

- Valuation & Risk: Lenders take a conservative view. Expect cautious valuations and rates that reflect the car’s market volatility and bespoke loan terms.

- Eligibility: Not all classic cars qualify. Lenders favor rare, well-documented, high-condition vehicles—especially those with strong provenance like a concours-level Ferrari.

- Storage & Insurance: Lenders may require approved secure storage and proof of insurance, sometimes naming themselves as loss payee. In high-value deals, they may even take custody.

- Loan Structure: Typical LTVs are 50–70%. Look closely at interest rates, fees, and repayment flexibility. Align the terms with your broader financial strategy.

- Specialist Lenders Only: Work with experts who understand both finance and collectible cars. A generic lender won’t cut it.

- Credit Review: Even if the loan is asset-backed, lenders still assess your financial health. Be ready with documentation.

- Fine Print Matters: Understand the terms, especially clauses on default, vehicle value fluctuations, and prepayment penalties.

- Insurance Fit: Use an agreed-value policy that meets lender requirements.

- Refinancing Options: As your car appreciates or needs shift, refinancing can unlock more capital or improve terms.

With expert guidance and the right lender, collectors can unlock liquidity from their garage without selling their prized assets.

Conclusion: Your Garage is More Than a Showcase — It’s a Balance Sheet

For serious collectors, classic cars aren’t just passion pieces — they’re appreciating assets. When approached strategically, classic car financing allows you to unlock capital without selling, disrupting your collection, or triggering tax consequences.

This isn’t about dealership loans or online lenders. It’s about bespoke credit facilities, structured discreetly and intelligently, to fit within a broader wealth strategy. Your classic car can power your next investment or provide liquidity exactly when it’s needed — without parting ways with the vehicle.

As lenders become more sophisticated and markets continue to evolve, the opportunity to monetize your collection while retaining ownership is now both practical and strategic.

Call to Action: Unlock Capital, Keep the Keys

Ready to unlock the value of your classic car collection? Contact us today for tailored classic car financing solutions across the UK, Europe & Asia-Pacific.

🎙️ Prefer an audio summary? Listen to the podcast discussion for a deeper dive into classic car finance. 🎧