Capital Stack Structuring: A Blueprint for Commercial Real Estate and Corporate Finance

In the high-stakes arena of 2026, the difference between a funded transaction and a stalled project rarely lies in the quality of the asset alone. It rests on the integrity of the financing behind it. Capital stack structuring, the strategic arrangement of debt and equity layers used to finance a project, has moved from a routine exercise to a decisive factor in accessing liquidity.

For C-suite executives, family offices and ultra high net worth investors, the era of cheap, monolithic debt is over. Lenders are not declining deals because the real estate property is weak; they are declining because the capital stack structuring in real estate is poorly assembled, unclear in its order of priority, or exposes them to unnecessary risk.

As we approach 2026, markets are tighter, underwriting scrutiny has intensified and the tolerance for sloppy structures has evaporated. In this environment, sophisticated capital stack structuring is about more than leverage. It is about de-risking repayment, optimising the cost of capital and presenting a financial structure that serious lenders are willing to back.

Capital Stack Structuring, Why it Matters in 2026: The New Funding Reality:

The macroeconomic landscape has shifted fundamentally. Higher interest rates have recalibrated the cost of borrowing, while senior debt lenders have retreated to lower loan-to-value (LTV) ratios to insulate themselves from valuation volatility. This retreat has created a “funding gap” in the middle of the stack, a void that must be filled with intelligent capital stack structuring.

In 2026, capital stack structuring is no longer theoretical; it is the operational playbook. Lenders and investors are scrutinising the financial structure with forensic detail. They are looking for stacks that are rational, resilient, and clearly defined in terms of order of priority.

The Shift from Leverage to Resilience

Previously, the goal of many sponsors was to maximise leverage to boost internal rates of return (IRR). Today, the priority has shifted to resilience. A well-structured stack demonstrates to a lender that the borrower has sufficient “skin in the game” and that the project can withstand stress tests regarding cash flow and exit yields.

Whether you are looking at commercial real estate, corporate finance, or a property development scheme, the ability to articulate a clear, robust capital structure is the primary key to unlocking financing sources.

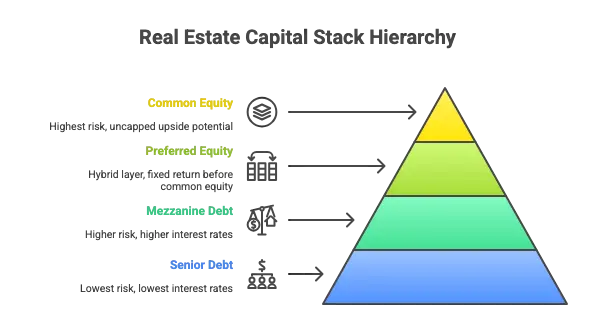

Deconstructing the Real Estate Capital Stack: Order of Priority

To master capital stack structuring, one must understand the distinct layers that fund a transaction. These layers are organised by risk and return, forming a hierarchy that dictates repayment priority and rights in the event of default.

The stack is typically visualised as a vertical block, where the bottom layers represent the safest positions (paid first), and the top layers represent the highest risk (paid last).

1. Senior Debt: The Foundation

At the bottom of the stack lies senior debt. This is the foundation of most financing structures. Senior debt lenders, typically banks, insurance companies, or debt funds, hold the first lien on the real estate property.

- Risk Profile: Lowest. Because they are repaid in full before any other capital provider, their risk is minimised.

- Cost: Consequently, senior debt carries the lowest interest rate.

- Role: It usually covers 50% to 65% of the total cost or value. In 2026, senior lenders are strictly enforcing debt service coverage ratios (DSCR), ensuring the asset’s cash flow can comfortably service the loan amount.

2. Mezzanine Debt: Bridging the Gap

Sitting directly above senior debt is mezzanine debt. This layer is crucial in the current market to bridge the gap between senior debt constraints and the equity requirement.

- Structure: Mezzanine finance is subordinate to senior debt but senior to all equity. It is often secured by a pledge of the ownership interests in the borrowing entity, rather than the property itself.

- Risk & Return: Mezzanine lenders often demand higher interest rates to compensate for the increased risk. If the borrower defaults, the mezzanine lender can foreclose on the equity and take control of the project.

- Repayment: Mezzanine debts are repaid after senior debt but before any distributions to preferred equity investors or common equity holders.

3. Preferred Equity: The Hybrid Layer

Preferred equity sits in a unique position. It is technically equity, but it functions similarly to debt in that it usually mandates a fixed return (or “preference”) that must be paid before common shareholders receive a penny.

- Priority: Preferred equity investors have a higher claim on cash flow than common equity but are subordinate to all debt.

- Usage: In 2026, we are seeing a surge in preferred equity as a flexible alternative to mezzanine debt. It allows sponsors to raise leverage without tripping covenants that restrict the amount of debt placed on an asset.

- Recoup: Investors in this layer expect to recoup their capital and a set return before the common equity sees profit.

4. Common Equity: The Top of the Stack

Common equity sits at the top of the capital stack. This is the riskiest layer, typically held by the sponsor (GP) and their limited partners (LPs).

- Risk: Common equity investors are in the “first loss” position. If the value of the property drops, their capital is eroded first.

- Return: In exchange for this risk, they enjoy uncapped upside potential. Once all debt and preferred equity obligations are met, the remaining profits flow to the common equity.

- Repayment: They are repaid last. In a real estate capital stack, this layer requires the highest conviction in the business plan.

The 2026 Edge: Why Optimal Capital Stack Structuring Wins Deals

In the current vintage of real estate investing, the “optimal capital stack” is not necessarily the one with the cheapest blended rate, but the one with the highest certainty of execution.

Aligning Incentives Through Structure

Sophisticated capital sources, from private credit funds to institutional equity investors, favour structures that align incentives. Capital stack structuring in 2026 is about demonstrating that the sponsor is not merely using financing sources used to fund the deal to strip out fees, but is committed to the asset’s long-term success.

Lenders are increasingly requiring a minimum equity contribution from the sponsor. A stack that relies too heavily on debt financing or synthetic equity is viewed with suspicion. Optimal capital stack structuring balances the cost of capital with the flexibility required to navigate market volatility.

Managing the “Weighted Average Cost of Capital” (WACC)

While interest rates remain elevated compared to the previous decade, intelligent structuring can mitigate the impact on the Weighted Average Cost of Capital (WACC). By blending senior debt, mezzanine finance, and equity investment precisely, a sponsor can achieve a leverage point that maximises return on investment (ROI) without exposing the project to distress risk.

For example, replacing a portion of expensive common equity with preferred equity can lower the overall WACC, enhancing the yield for the common shareholders, provided the asset’s cash flow can support the preferred payments.

Strategic Applications: Real-World Scenarios

To understand how capital stack structuring functions in practice, consider these anonymous but realistic scenarios reflecting the 2026 market environment.

Scenario A: The Refinancing “Gap”

A prominent commercial property owner needs to refinance a prime office asset. The original loan was at 65% LTV. However, due to cap rate expansion, the asset’s value has adjusted downward. The new senior debt lenders are only willing to lend at 55% of the current value.

- The Problem: The sponsor faces a capital shortfall to pay off the maturing loan.

- The Solution: The sponsor utilises capital stack structuring to introduce preferred equity. This layer fills the gap between the new senior loan and the existing equity.

- The Outcome: The deal is refinanced without the sponsor having to inject massive amounts of fresh common equity or face a forced sale. The preferred equity investors receive a compelling fixed return, secured by the cash flow of a stabilised asset.

Scenario B: The Ground-Up Development

A developer plans a large-scale property development scheme. Traditional banks are conservative, capping development finance at 50% of cost.

- The Problem: The developer wants to reserve cash for other projects and cannot fund the remaining 50% as pure equity.

- The Solution: The developer engages a mezzanine lender to provide an additional 15% of the capital stack.

- The Structure: The stack now consists of 50% senior debt, 15% mezzanine debt, and 35% equity financing.

- The Outcome: The mezzanine finance is more expensive than the bank loan, but it is cheaper than equity. This structure boosts the developer’s internal rate of return on their 35% equity stake while ensuring the project is fully funded.

Scenario C: Distressed Acquisition

An opportunistic real estate investor identifies a hospitality asset selling at a discount. The asset has no cash flow currently, making traditional debt and equity mixes difficult.

- The Problem: Senior lenders refuse to lend on non-income-producing assets.

- The Solution: The investor structures the stack with “bridge equity” and high-yield private equity debt that accrues interest rather than requiring current pay.

- The Outcome: The investor secures the asset. Once stabilised, they refinance into a traditional real estate capital stack with lower-cost senior debt, paying out the expensive bridge capital.

Why Sophisticated Capital Stack Structuring is Gaining Popularity Now

The rise of bespoke capital stack structuring is driven by necessity. The “set it and forget it” financing models of the 2010s are obsolete.

1. The Refinancing Cliff

A significant volume of commercial loans originated in 2021 and 2022 are reaching maturity. Many of these face a refinancing gap. Capital stack refers to the solution for this gap, layering in mezzanine debt or preferred equity to facilitate the refinance.

2. Investor Demand for Risk-Adjusted Yield

Investors are becoming more granular in their requirements. Some want to invest for pure safety (senior debt), while others seek yield without the volatility of common ownership (mezzanine/preferred). Structuring allows sponsors to slice the capital stack to appeal to different types of capital providers simultaneously.

3. Flexibility Over Cost

In 2026, flexibility is valued as highly as cost. Borrowing structures that allow for payment-in-kind (PIK) interest, extension options, or flexible covenants are in high demand. Sponsors are willing to pay a slightly higher rate for finance solutions that prevent an event of default during a temporary market dip.

Actionable Considerations for Raising Capital

For decision-makers looking to raise capital in 2026, the following considerations are paramount when approaching the capital stack:

- Avoid Over-Leverage: Lenders favour resilience. A stack that is “stretched” to the absolute limit is a red flag. Leave a buffer in your debt service coverage ratio.

- Clarify the Waterfall: Ensure the order of payment is explicitly defined in the intercreditor agreement. Ambiguity regarding who gets repaid and when can kill a deal during due diligence.

- Understand Dilution: When adding equity or preferred layers, calculate the impact on the common equity returns. Dilution is often preferable to default, but it must be modelled accurately.

- Match Term to Strategy: Do not use short-term, high-cost mezzanine finance for a long-term hold unless there is a clear exit or refinance strategy.

- Scrutinise the Lender: In a layered stack, the relationship between the senior lender and the mezzanine lender is critical. Ensure they have an established relationship or a clear intercreditor agreement to avoid paralysis in a downside scenario.

- Equity Sits at the Top: Remember that equity sits at the top of the risk spectrum. To attract equity investors, you must show that the debt layers below them are stable and that the risk premium is justified.

- Recourse vs. Non-Recourse: Be clear on what is being pledged. Mezzanine lenders often require a pledge of equity interests. Understand the implications of this level of risk for the sponsor.

Conclusion: The Mindset Shift for 2026

Capital stack structuring is no longer just a chapter in a corporate finance textbook; it is the defining characteristic of successful deal-making in 2026. The market has moved away from a reliance on cheap, abundant leverage toward a model that rewards discipline, clarity, and alignment of interest.

For the real estate investor and corporate borrower, the message is clear: the “optimal” stack is one that prioritises certainty of closing and resilience of cash flow. By understanding the nuance of senior debt, mezzanine debt, and the various shades of equity, sponsors can construct a fortress balance sheet capable of weathering volatility and attracting the most sophisticated financing sources.

The winners of 2026 will not be those who take the most risk, but those who structure their risk most intelligently. Whether you are navigating a complex property development scheme or a corporate acquisition, the architecture of your capital stack is your most valuable asset.

Discreet Guidance for Complex Structures

Navigating the complexities of the modern capital stack requires more than just market knowledge; it requires access to the right relationships and strategic foresight.

If you are a sponsor or investor seeking to optimise your capital stack structuring for a significant transaction, we invite you to arrange a private consultation. We specialise in tailoring senior debt, mezzanine, and equity financing solutions that align with your strategic objectives in the 2026 marketplace.

Contact us today to discuss your financing requirements with discretion and precision.