Refinancing Risk 2026: When Timing Turns Manageable Debt into Forced Outcomes

In the upper echelons of corporate finance and private wealth management, the term ‘risk’ is rarely synonymous with a lack of capital. For the sophisticated borrower, the challenge is seldom an absolute inability to find a lender. Instead, the true danger lies in the erosion of optionality. As we approach the significant maturity walls of 2026, a new paradigm is emerging: refinancing risk is no longer a question of creditworthiness, but a question of timing.For CFOs, treasurers, and Ultra-High-Net-Worth Individuals (UHNWIs), the 2026 horizon represents a convergence of post-pandemic debt cycles, shifting central bank policies, and a fundamental tightening of credit committee behaviours. Those who treat a 2026 maturity as a 2026 problem are already ceding their negotiating power to the market.

Redefining Refinancing Risk for the 2026 Credit Market

In a textbook sense, refinancing risk (often conflated with rollover risk) is the possibility that a borrower will be unable to replace an existing debt obligation with new debt at a critical juncture. However, for high-level decision-makers, this definition is too narrow.

In the current climate, refinancing risk should be viewed as the risk of being forced into a sub-optimal transaction due to a compressed timeline. It is the transition from being a ‘price maker’ to a ‘price taker.’ When a corporation or a family office approaches a bank or a commercial lending institution with only six months of runway, the lender no longer views the loan as a partnership; they view it as a rescue.The 2026 landscape is unique. Much of the corporate debt and commercial real estate finance currently on balance sheets was secured during the 2019–2022 window, a period of historic lows in interest rates. As these obligations approach maturity, the gap between the original funding costs and the current market reality is stark. Refinancing risk in 2026 is the risk that the market conditions at the time of issuance will be significantly more adverse than the conditions at the time of the original contract.

Why Timing, Not Leverage, is Now the Real Problem

Historically, a strong rating and low leverage were sufficient to mitigate refinancing risk. If the asset was good and the liquidity was present, the refinance was a formality. In 2026, this assumption is dangerous.

The Pricing of Uncertainty

A bank credit committee in 2026 will not just look at your cash flow; they will look at your execution window. If you are forced to repay or refinance during a period of inflation volatility or geopolitical instability, the financing costs will reflect that urgency.

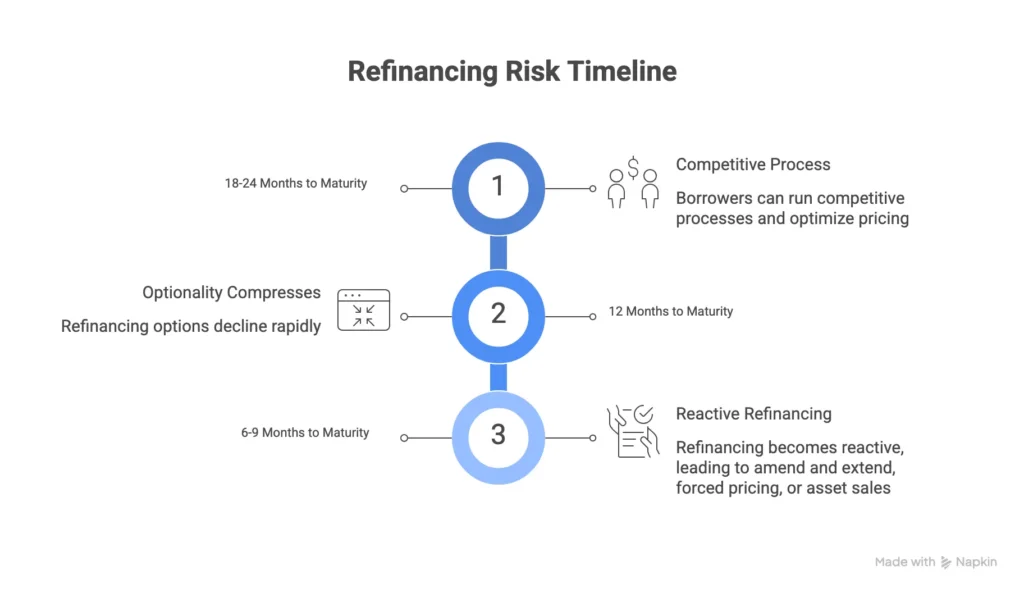

The Compression of Options

Waiting for better markets has historically been a rational strategy, but in 2026 the credit market shows little tolerance for execution risk. When a borrower waits, they allow the creditor to dictate terms. What could have been a competitive multi-bank tender 24 months out becomes a bilateral “amend-and-extend” 6 months out, often with punitive fees and restrictive covenants.

The Shift in Commercial Lending

Commercial lending has moved from a growth-oriented posture to one of downside protection. Even for firms with strong underlying businesses, new debt is now conditional on evidence of proactive liability management.

The Anatomy of a Forced Outcome: Real-World Scenarios

To understand how refinancing risk manifests in 2026, we must look at how timing failures lead to adverse outcomes for otherwise healthy entities.

Scenario A: The Real Estate Balloon Payment

Consider a high-value commercial portfolio with a significant balloon payment due in Q3 2026. The borrower, an asset-rich family office, assumes that their high equity cushion ensures a smooth refinance. However, they delay formal engagement with the bank until early 2026, hoping for an interest rate cut.

By the time they engage, the lender has already filled its sector allocation for the year. The borrower is forced to turn to alternative funding sources at 300 basis points above the market rate, or worse, execute a forced asset sale in a soft market to meet the obligation. The outcome was driven by delay, not by the quality of the asset.

Scenario B: The Corporate Bond Cliff

A mid-cap corporation has a bond issue maturing in 2026. They have maintained a solid credit profile, but they wait for a specific “window” of market stability to launch their new debt issuance. A sudden macro event closes the high-yield market for three months. Because they are now within the 12-month maturity window, their rating is put on negative watch due to liquidity concerns. This self-fulfilling prophecy drives up their borrowing costs when the market finally reopens.

Why Refinancing Risk is Escalating in 2026

Several factors are converging to make 2026 a particularly challenging year for debt maturity management.

- Maturity Concentration: The volume of corporate debt and commercial lending facilities set to expire in 2026 is significantly higher than in previous years, creating a “crowded house” effect where borrowers are competing for the same pool of institutional liquidity.

- Tighter Underwriting Standards: Banks are under increased regulatory pressure to scrutinise refinancing needs. The “pro-forma” projections that were accepted in 2021 are being replaced by stress-tested models that assume higher interest rates and lower asset valuations.

- The End of Extend and Pretend: post-2008 rollover strategies are no longer being tolerated by creditors.

- Reduced Execution Certainty: In a volatile market, the time between a “term sheet” and “drawdown” is fraught with risk. Transaction failures are becoming more common as lenders invoke “material adverse change” clauses or simply pull back during the documentation phase.

Strategic Mitigation: How Sophisticated Borrowers Protect Their Balance Sheets

For the C-suite and HNWIs, managing refinancing risk is an exercise in strategic foresight. It requires a shift in mindset: viewing the refinance as a multi-year project rather than a quarterly task.

1. The 18–24 Month Rule

Engagement with the credit market should begin no later than 18 to 24 months before maturity. This window allows the borrower to:

- Test lender appetite without the pressure of an impending default.

- Explore alternative funding structures, such as private credit or mezzanine finance.

- Address any rating or credit profile issues well in advance.

2. Decoupling Liquidity from Term

Sophisticated borrowers are increasingly separating their need for immediate liquidity from the long-term optimisation of their debt terms. This might involve securing a bridge facility or a revolving credit line early, even if the pricing is not ideal, to ensure that the existing debt can be retired regardless of market conditions. Once the immediate refinancing risk is removed, the borrower can wait for an opportunistic window to secure long-term funding.

3. Diversifying Lender Relationships

Relying on a single bank for a major refinance is a significant point of failure. In 2026, resilience will come from having a diverse panel of creditors, including traditional banks, non-bank lenders, and institutional bond investors. If one commercial lending sector pulls back, others may remain open.

4. Understanding the Internal Bank Perspective

Decision-makers must understand how banks view refinancing risk internally. A loan that is within 12 months of maturity is often classified differently for capital adequacy purposes. By approaching a lender while the debt is still “long-term,” the borrower helps the bank’s own balance sheet metrics, which can lead to more favourable terms.

The Role of Luxury Asset Finance and Securities-Based Lending

For UHNWIs and family offices, refinancing risk often extends to non-corporate assets. Luxury asset finance (for aircraft, yachts, or significant art collections) and securities-based lending (SBL) are sensitive to the same timing risks.

In 2026, an SBL facility that was once a simple “set and forget” tool may face margin call pressures or refinance hurdles if the underlying asset volatility increases. Managing these liabilities requires the same proactive timing as a major corporate debt restructuring. Ensuring that cash reserves or liquid assets are positioned to de-lever a facility quickly is a key component of resilience.

Conclusion: Control the Timing or Accept the Outcome

For UHNWIs and family offices, refinancing risk often extends to non-corporate assets. Luxury asset finance (for aircraft, yachts, or significant art collections) and securities-based lending (SBL) are sensitive to the same timing risks.

In 2026, an SBL facility that was once a simple “set and forget” tool may face margin call pressures or refinance hurdles if the underlying asset volatility increases. Managing these liabilities requires the same proactive timing as a major corporate debt restructuring. Ensuring that cash reserves or liquid assets are positioned to de-lever a facility quickly is a key component of resilience.

Call to Action

For borrowers assessing upcoming maturities, capital structure pressure, or refinancing windows, early structuring conversations often determine whether outcomes remain optional or become forced. In an environment where commercial lending appetite can shift in a matter of weeks, a discreet, high-level review of your refinancing needs is the first step toward securing your financial autonomy.

For a confidential discussion regarding your 2026 maturity profile and capital strategy, we invite you to engage with our senior advisors. Discreet discussions are welcome.