Private Credit Assumptions Explained: Why Recovery Models Are Breaking in 2026

For the better part of a decade, the private credit market has been the darling of the alternative investment world. Promising “equity-like returns with debt-like risk,” it has attracted a wall of capital from family offices, UHNWIs, and institutional allocators. However, as the credit cycle turns and the era of “cheap money” fades into the rearview mirror, the foundational hypotheses of the asset class are being tested.

To navigate this landscape, sophisticated investors must look beyond the glossy pitch decks. Understanding private credit assumptions explained through the lens of a seasoned practitioner is no longer optional, it is a requirement for capital preservation. The reality is that private credit isn’t broken, but the lazy underwriting assumptions that have governed the last five years certainly are.

What Are Private Credit Assumptions?

Private credit assumptions explained: In the context of direct lending and private debt, assumptions are the implicit beliefs that lenders and investors hold regarding how risk, return, and recovery will behave over the life of a loan. These are not guarantees; they are underwriting hypotheses.

When a private credit fund evaluates a borrower, they make projections about the company’s future cash flows, the stability of the capital structure, and the likely recovery assumptions in the event of a default. For the investor, these assumptions form the basis of the expected Internal Rate of Return (IRR). However, in a benign economic environment, these assumptions are rarely challenged. It is only when interest rates rise and credit risk intensifies that we see which private credit managers were underwriting based on reality and which were relying on marketing myths.

Key Private Credit Assumptions Investors Rely On in 2026

When investors allocate to private credit, they are typically relying on a small set of core assumptions, whether consciously or not. These assumptions form the foundation of expected returns, portfolio stability, and capital preservation.

The most common private credit assumptions include:

- The illiquidity premium will consistently compensate for capital being locked up for multiple years

- Default rates will remain structurally lower than public credit due to active management and tighter documentation

- Covenant protection will allow lenders to intervene early and preserve value

- Floating rate structures will protect returns without materially increasing borrower distress

- Senior secured positioning will translate into predictable recovery outcomes in a downside scenario

- Private credit performance will remain less volatile and less correlated than public markets

- Private equity sponsors will continue to support portfolio companies through periods of stress

Each of these assumptions has historically held true at different points in the credit cycle. The risk for investors today is not that these assumptions are inherently wrong, but that many are being relied upon simultaneously, at a point in the cycle when refinancing risk, higher interest rates, and slowing growth are converging.

The sections below examine where these assumptions remain valid, where they are weakening, and where they can fail entirely if left unchallenged.

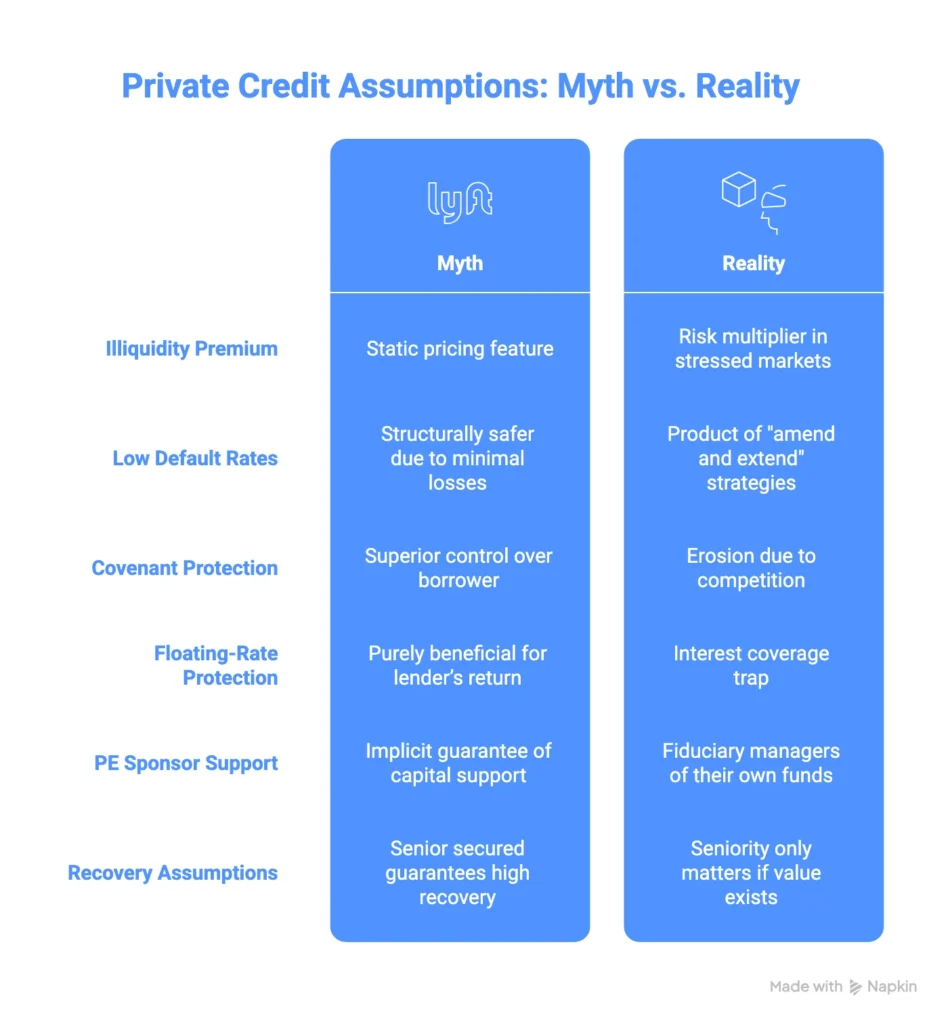

1. The Illiquidity Premium: A Feature or a Risk Multiplier?

One of the primary private credit assumptions explained in every investor presentation is the “illiquidity premium.” The theory suggests that by locking up capital for 5–7 years, investors should earn an additional 300–500 basis points over liquid high-yield markets.

The Myth

The assumption is that illiquidity is a static pricing feature, a “bonus” for patience.

The Reality

In a stressed market, illiquidity becomes a risk multiplier. In public markets, if a borrower’s fundamentals deteriorate, a lender can exit the position at a discount to preserve the remaining principal. In private credit loans, there is often no secondary market. You are “married” to the asset.

If the private credit market faces a systemic liquidity crunch, that 300bps premium can quickly be swallowed by the inability to rebalance a portfolio or exit a deteriorating credit before it hits a hard default. Sophisticated private debt investors must ask: is the premium compensating for the time-lock, or is it merely masking the volatility that would be apparent if the loan were marked-to-market daily?

2. The Mirage of Low Historical Default Rates

When reviewing private credit returns, investors are often comforted by historically low default rate figures, frequently cited as being lower than those in the broadly syndicated loan (BSL) market.

The Myth

Private credit is structurally safer because historical losses have been minimal.

The Reality

The “low default rate” narrative is often a product of “amend and extend” strategies. Because private loans are bilateral or held by a small club of lenders, it is much easier to restructure a deal behind closed doors.

We are currently seeing a surge in:

- PIK (Payment-in-Kind) Toggles: Allowing the borrower to add interest to the principal rather than paying in cash.

- Covenant Waivers: Ignoring technical breaches to avoid triggering a formal default.

- Equity Cures: Sponsors injecting just enough cash to meet a quarterly test.

These actions do not eliminate credit risk; they defer it. Private credit assumptions explained in this context reveal that many “performing” loans are actually “zombie” credits. The true test of recovery assumptions in private credit will occur when these deferred obligations finally hit a refinancing wall that they cannot climb.

3. The Erosion of Covenant Protection

Historically, the “private” in private credit stood for “protection.” Direct lending deals were famous for having “bespoke” covenant protection, including tight financial maintenance covenants that allowed lenders to intervene at the first sign of trouble.

The Myth

Private credit managers have superior control over the borrower compared to public bondholders.

The Reality

As the asset class grew, competition among private debt funds intensified. To win deals, many managers moved toward “covenant-lite” structures or “covenant-loose” definitions of EBITDA.

When we look at private lending structures today, we often find “EBITDA add-backs” that are purely aspirational. If a lender assumes they have a seat at the table because of a covenant, but that covenant only triggers when the company is already insolvent, the protection is illusory. For the C-suite and HNWIs, the focus should be on enforceability, not just the presence of a covenant in the legal docs.

4. Floating-Rate Protection: The Double-Edged Sword

Floating rate loans have been the primary selling point for private credit during the recent hiking cycle. As base rates rose, so did the yields for private debt investors.

The Myth

Rising interest rates are purely beneficial for the lender’s return profile.

The Reality

There is a ceiling to how much interest a borrower can pay before their cash flows are exhausted. This is the “interest coverage” trap. While the lender enjoys a higher theoretical yield, the credit risk assessment changes fundamentally when debt service consumes 80% of operating cash flow.At a certain point, the floating rate ceases to be a hedge against inflation and starts becoming the primary driver of default risk. If the borrower cannot pass on costs or grow revenue, the very feature designed to protect the investor’s yield becomes the catalyst for the destruction of their principal.

5. The Fallacy of PE Sponsor Support

A significant portion of the private credit market involves lending to companies owned by Private Equity (PE) firms. The assumption is that a deep-pocketed sponsor will always support their portfolio company to protect their equity.

The Myth

The “Sponsor Relationship” provides an implicit guarantee of capital support during distress.

The Reality

PE sponsors are fiduciary managers of their own funds. They perform a cold-blooded “NPV (Net Present Value) calculation” on every asset. If the capital structure is underwater and the enterprise value has dropped below the debt level, the sponsor will walk away.We are increasingly seeing “Sponsor-led restructurings” where the PE firm prioritises their latest fund’s reputation over a single asset’s survival. In some cases, they may even use “priming” transactions to move valuable assets out of the reach of existing private credit lenders. Relying on sponsor “goodwill” is a dangerous loan assumption.

6. Recovery Assumptions: Seniority vs. Enterprise Value

In the hierarchy of the capital structure, private credit usually sits at the “Senior Secured” level.

The Myth

Being senior secured guarantees a high recovery rate (historically 60–80%).

The Reality

Seniority only matters if there is value to recover. In private companies, especially those in the service or technology sectors, the “assets” are often intangible. If the company fails, the “security” (the IP, the brand, the customer list) can evaporate.Furthermore, the rise of unitranche loans, which blend senior and junior debt into a single facility, has complicated recovery assumptions. In a liquidation, the lack of a junior debt cushion means the “senior” lender takes the first pound of loss. Sophisticated investors must evaluate default risk modelling based on the liquidation value of the assets, not the entry multiple paid by the PE sponsor three years ago.

Real-World Scenarios: When Assumptions Meet Reality

To truly understand private credit assumptions explained, we must look at how these deals behave under pressure.

Case Study: The Unitranche “Roll-Forward”

A mid-market healthcare company took a £100m unitranche loan at 6x EBITDA. As interest rates rose, their interest coverage ratio dropped to 1.1x. Instead of declaring a default, the private credit manager agreed to a “PIK toggle” for 50% of the interest.

- The Assumption: The company will grow out of the problem.

- The Reality: The debt load is increasing while the business stagnates. The manager is avoiding a “mark-down” on their books, but the eventual recovery will be significantly lower because the principal is now £115m on a business still only worth £120m.

Case Study: The “Bespoke” Covenant Trap

A manufacturing firm had a “Net Debt/EBITDA” covenant. However, the definition of EBITDA allowed for “pro-forma synergies” from an acquisition that never materialised.

- The Assumption: The lender has a 5x leverage cap.

The Reality: On a cash basis, the leverage was 8x. By the time the “technical” covenant was breached, the company’s liquidity was so depleted that a turnaround was impossible.

Why This Matters Now for HNWIs and Decision-Makers

The private credit market is transitioning from a “yield harvesting” phase to a “loss management” phase. For a decade, anyone could look like a genius in private debt because the rising tide of liquidity lifted all boats.

Now, the divergence between top-tier private credit managers and “asset gatherers” will become stark. Sophisticated investors should focus on:

- True Cash Interest vs. PIK Dependency: What percentage of the fund’s yield is actually being paid in cash by borrowers?

- Covenant Enforceability: Are the covenants “maintenance-based” (tested quarterly) or “incurrence-based” (only tested if the company takes on more debt)?

- LTV Based on Downside: Is the Loan-to-Value ratio based on an optimistic “exit multiple” or a conservative “liquidation value”?

- Sponsor Behaviour: How has the PE sponsor treated lenders in other distressed situations? Do they have a history of “creditor-on-creditor violence”?

Strategic Insights: How to Vet Private Credit Portfolios

If you are an asset manager or a family office principal, your due diligence process must evolve. The standard “track record” of the last ten years is largely irrelevant because it was achieved in a zero-interest-rate environment.

Focus on “Workout” Capabilities

In the coming years, the most valuable part of a private credit fund will not be the origination team, but the “workout” or “special situations” team. You want to know exactly what happens when a loan goes sideways. Does the manager have the legal and operational expertise to take over a company if necessary?

Scrutinise the Valuation Policy

Since private loans are not traded on exchanges, valuations are often “mark-to-model.” Ask for the sensitivity analysis. If the discount rate increased by 200bps, what would happen to the NAV? If the valuation hasn’t moved despite a massive spike in market yields, you are likely looking at “volatility suppression,” not actual stability.

Diversification Beyond Direct Lending

Consider different types of private credit. While direct lending to PE-backed software companies is crowded, other areas like Luxury Asset Finance, Securities-Based Lending, or Commercial Real Estate Finance may offer different risk-reward profiles and more tangible collateral.

The Role of AI in Modern Credit Risk Assessment

As we look toward the future, AI in Finance is beginning to play a role in refining private credit assumptions. Advanced algorithms can now scan thousands of data points, from shipping manifests to real-time consumer sentiment, to provide a more accurate picture of a borrower’s health than traditional quarterly management accounts.

For the high-level decision-maker, leveraging these technological gains can provide a competitive advantage. However, AI is only as good as the data it receives. In the opaque world of private debt, the “human” element of auditing the lender-borrower relationship remains paramount.

Conclusion: Reframing Private Credit Reality

Private credit remains one of the most effective tools for income generation and portfolio diversification. However, the “marketing version” of the asset class is currently at odds with the “economic version.”

The private credit assumptions explained in this post highlight a simple truth: seniority in the capital structure is not a substitute for rigorous underwriting. As defaults rise and the “amend and extend” cycle reaches its limit, the winners will be those who priced illiquidity as a risk, not a comfort, and who understood that recovery assumptions are only as strong as the underlying enterprise value.

For UHNWIs, C-suite executives, property developers, the message is clear: stop believing the recovery myths. Demand transparency on PIK levels, scrutinise EBITDA definitions, and ensure your managers are prepared for a “workout” environment. Structured properly, private credit works. Structured blindly, it is a ticking clock.

Call to Action (CTA)

If you are currently allocating to private credit or reviewing an existing portfolio of private debt funds, now is the time for a candid, assumption-level assessment.

At the highest levels of wealth management and corporate finance, the best decisions are made when we strip away the marketing fluff and look at the raw mechanics of the deal. If you require a discreet, impartial review of your credit exposures or wish to discuss private credit solutions that prioritises principal protection over “headline yields, let us start a conversation.

The next phase of the credit cycle will not be kind to the complacent. Ensure your capital is positioned for resilience, not just returns. Speak with Forbes Le Brock today