Debt Covenant Monitoring and Trigger Risk After Close

In the high-stakes world of private credit and complex capital structures, debt covenant monitoring is rarely treated as the finish line. The closing dinner is celebrated, legal teams stand down, origination fees are booked, and the deal quietly migrates from the front office to the back office. Yet seasoned investors and risk managers know the uncomfortable truth: most loans do not fail at the underwriting stage. They fail quietly and incrementally, in years two to four of the loan’s life.

This is the “silent failure window,” where the rigorous discipline of the deal team is replaced by routine reporting. It is here that debt covenant monitoring becomes the single most critical determinant of capital preservation.

Effective monitoring is not merely an administrative exercise in checking boxes or populating a spreadsheet. It is a continuous process of credit surveillance. In a market characterised by higher interest rates and thinner liquidity, the difference between a managed exit and a capital impairment often lies in the rigour of the monitoring framework applied after the ink is dry.

What Is Debt Covenant Monitoring (In Practice)?

To the uninitiated, debt covenant monitoring is often reduced to the periodic calculation of ratios, when in reality those metrics are merely lagging indicators of deeper credit stress. However, for the C-suite and investment committees, this view is dangerously simplistic, because the covenant tests themselves are defined much earlier in the process, specifically by how underwriting sets covenant tests.

True debt covenant monitoring is the active surveillance of a borrower’s creditworthiness against the loan agreement. It encompasses three distinct layers:

- Financial Covenants: The quantitative tests (e.g., Debt Service Coverage Ratio, Loan-to-Value) that measure financial performance.

- Non-Financial Covenants: The affirmative and negative covenants that restrict behaviour, such as limits on capex, M&A activity, or dividend recapitalisations.

- Behavioural Indicators: The subtle shifts in how a borrower interacts with the lender, delays in providing management accounts, vague answers to a query, or repeated requests to adjust definitions.

It is a discipline focused on identifying “covenant drift”, the gradual erosion of headroom, long before a hard breach occurs. By the time a borrower formally breaches a financial covenant, the credit has likely been deteriorating for quarters. A robust monitoring framework detects these early warning signs, allowing the lender to intervene while they still possess leverage.

Where Deals Break Down After Close

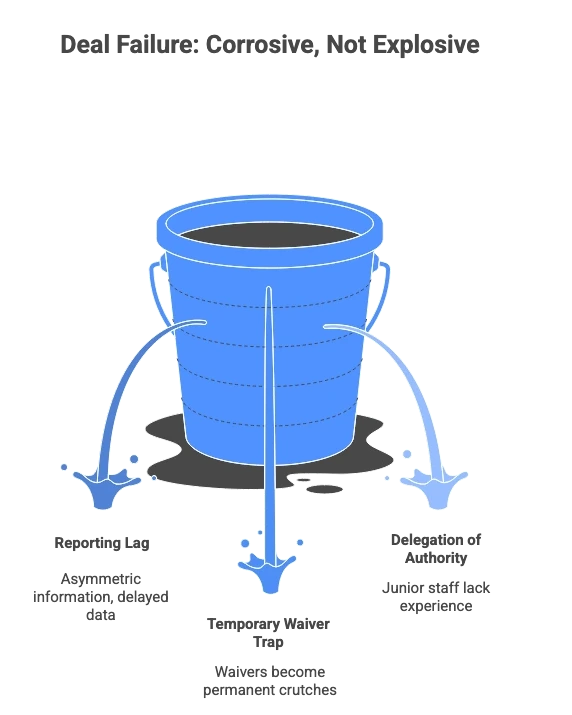

The mechanics of deal failure are rarely explosive; they are corrosive. When debt covenant monitoring is treated as a passive reporting function rather than active risk management, several structural weaknesses emerge in the debt portfolio.

The Reporting Lag and Selective Disclosure

Information asymmetry is the lender’s greatest risk. A common precursor to failure is the “reporting lag.” When financial information arrives weeks late, or when management accounts are presented without the usual granularity, it is rarely an administrative oversight. It is often a delay tactic designed to buy time to massage the numbers. Without real-time access or a culture of proactive communication, lenders are often looking at data that is already obsolete.

The “Temporary Waiver” Trap

When a minor breach occurs, perhaps a slight dip in the coverage ratio, the instinct is often to grant a waiver to preserve the relationship. However, without a strict monitoring framework, temporary waivers can become permanent crutches. If a lender waives a breach without extracting a concession or enhanced visibility, they signal a lack of enforcement appetite. This encourages the borrower to test the boundaries further, eroding the protective power of the loan covenants.

Delegation of Authority

In many organisations, covenant monitoring is pushed too far down the hierarchy. Junior staff may confirm that figures reconcile mechanically, but lack the experience to challenge the assumptions behind them. EBITDA add-backs are accepted at face value, definitions are stretched, and judgement is replaced with box-ticking. The result is a dangerous gap between the original credit logic and the reality of ongoing risk. When monitoring becomes procedural rather than interpretive, value erosion is almost guaranteed.

Structure Sets the Covenants – Debt Monitoring Determines Survival

There is an industry adage: Underwriting defines the risk; monitoring manages the outcome.

You can structure the most robust loan agreement in the market,and as explored in how structure influences the stability of covenants, replete with tight banking covenants, cross-default clauses, and aggressive negative covenants. Yet, these legal protections are dormant assets unless they are actively monitored.

The loan covenants set the rules of engagement, but debt covenant monitoring determines whether those rules are enforced. A tight structure with weak monitoring is functionally equivalent to a “covenant-lite” deal. Conversely, a standard structure with aggressive, intelligent monitoring can often outperform, as it forces the borrower to maintain financial discipline and engage in transparent dialogue.

The goal of the monitoring framework is to preserve optionality. When a breach is identified early, the lender has options: re-price the risk, demand an equity injection, or restructure the borrowing. If the breach is caught late, the only option remaining is often a distressed enforcement or a haircut.

Real-World Scenarios: The Cost of Complacency

To understand the severity of the risk, we must look at how debt covenant monitoring failures play out in reality.

The “EBITDA” Add-Back Illusion

Consider a leveraged buyout where the borrower is struggling with cash flow. To avoid breaching the leverage covenant, the CFO aggressively utilises “pro forma” adjustments and add-backs allowed under the loan agreement. A passive monitoring process accepts the adjusted EBITDA figure. A rigorous process, however, scrutinises the quality of earnings, realising that “one-off restructuring costs” have become a recurring expense. The covenant technically holds, but the financial health of the company has collapsed.

The Asset Disposal Distortion

In a real estate financing scenario, a borrower might sell a high-performing asset to generate cash to repay a portion of the debt or service interest. This improves the immediate liquidity position but degrades the quality of the remaining collateral. If the debt monitoring focuses solely on the debt service ratio without analysing the remaining asset base, the lender may wake up to a portfolio of secondary assets that cannot support the exit valuation.

The Equity Cure Abuse

Many agreements allow for an “equity cure”, an injection of cash to fix a ratio breach. While this protects the lender in the short term, repeated reliance on cures is a sign of a structural deficit in the business model. If covenant monitoring treats an equity cure as a “pass” without investigating the underlying operational failure, the lender is merely kicking the can down the road toward a larger default.

Why Debt Covenant Monitoring Matters More Now

The macroeconomic environment has shifted, and with it, the margin for error has vanished, a reality reinforced by industry research showing renewed focus on covenant discipline as credit conditions tighten.

- Higher Interest Rates: With the cost of borrowing significantly higher, debt service burdens have increased, eroding headroom across the board. Companies that were comfortable at 3% rates are drowning at 8%.

- Refinance Risk: The “extend and pretend” strategy is harder to execute when liquidity is scarce. Lenders cannot assume a takeout by another bank is imminent.

- Thinner Equity Cushions: Valuations in many sectors have corrected, meaning the equity buffer beneath the debt is thinner.

In this environment, financial stability is fragile. A breach today is more likely to lead to a payment default than it was five years ago, a dynamic increasingly highlighted by the European Central Bank in its analysis of loan performance under tighter financial conditions. Consequently, debt covenant monitoring has transitioned from a compliance task to a strategic imperative. It is the only mechanism lenders have to ensure financial management remains prudent during turbulent times.

What Strong Debt Covenant Monitoring Actually Looks Like

Effective debt covenant monitoring moves beyond the spreadsheet and into the realm of governance. It requires a shift in mindset from reactive to proactive.

1. Independent Data Validation

Best practices dictate that lenders should not rely solely on borrower-calculated certificates. The monitoring team must undertake an independent verification of the financial information, cross-referencing management accounts with bank statements and third-party valuations.

2. Clear Trigger Thresholds

A strong framework establishes “soft triggers” set inside the hard covenant levels. If a coverage ratio is set at 1.50x, the monitoring team should be alerted if it drops below 1.65x. This early warning system allows for a “quiet word” with the borrower before a formal breach letter is required.

3. Focus on Cash, Not Just Accruals

Accounting profits can be manipulated; cash cannot. Effective debt monitoring places a heavy emphasis on cash flow statements and liquidity analysis, looking for divergence between reported EBITDA and actual cash generation.

4. Escalation Discipline

There must be a clear protocol for the severity of the breach. Who is notified? When does the Investment Committee get involved? When do we engage legal counsel? Removing ambiguity from the decision-making process ensures that lender reaction times are fast and decisive.

Key Takeaways for Lenders and Borrowers

For the stakeholder navigating this landscape, the following principles are paramount:

- Covenants are only as strong as their enforcement. A lender who ignores minor deviations loses the moral and legal high ground when a major crisis hits.

- Transparency builds optionality. For the borrower, greater transparency and proactive communication regarding potential issues can often secure a waiver or amendment. Hiding the problem until the management accounts reveal it destroys trust.

- Delay destroys leverage. The longer a breach or covenant drift is left unaddressed, the fewer options remain to fix it. Immediate repayment demands are rarely successful if the cash is already gone.

- Look beyond the ratio. Financial ratios are lagging indicators. Behavioural changes, market shifts, and employer covenant strength (in defined benefit pension scenarios) are leading indicators.

Conclusion: The Mindset Shift

Deals do not fail because covenants exist; they fail because no one acts when those covenants start to matter.

Debt covenant monitoring is the immune system of a credit portfolio. When it is functioning correctly, it detects pathogens, bad behaviour, deteriorating performance, market shifts, and neutralises them before they threaten the life of the deal. When it is suppressed or ignored, the infection spreads until it is fatal.

For decision-makers, the shift is simple: stop viewing monitoring as a back-office cost and start viewing it as a front-office defence. In a volatile market, the ability to monitor, interpret, and act on financial reporting is the ultimate competitive advantage.

Are you confident in the resilience of your current loan book?

For lenders and borrowers navigating complex capital structures, post-close discipline is where value is protected or destroyed. When trigger risk, covenant headroom, or reporting integrity begin to drift, an early, structured conversation preserves options that disappear quickly once stress becomes visible.