Credit Market 2026: The Reset – What Serious Borrowers Need to Know

As we look toward the horizon of the credit market 2026, a distinct narrative is emerging, one that defies the simplistic binary of “boom” or “bust.” For high-level decision-makers, the prevailing sentiment isn’t panic; it is a profound sense of recalibration.

We are entering a period that will not be defined merely as another “tight market.” Instead, we are witnessing a fundamental reset. The era of free money is long dead, but the era of “easy” credit, where a decent story and a handshake could secure leverage, has also evaporated.

The 2026 Global credit outlook presents a landscape shaped by sticky inflation, uncertain rate cuts, a labour market that is softening but not breaking, and, crucially, tight credit spreads. As indicated by recent market analysis, tight credit spreads offer limited cushion, and lenders have moved into a more selective, research-driven posture.

Understanding this distinction is vital. The 2026 global financial environment will not necessarily lack capital; there is ample dry powder in private credit and fixed income allocations. However, accessing that capital will require a level of discipline, transparency, and strategic foresight that many borrowers have not had to exercise in the past.

This article explores the market outlook for the coming years, dissecting the credit markets not just from a macroeconomic perspective, but through the lens of the borrower who needs to navigate this new reality.

What the Credit Market 2026 Reset Actually Means

To navigate the markets in 2026, one must first strip away the jargon. When we speak of a “reset,” we are not predicting a recession or a crash. A reset is more insidious for the unprepared because it looks like business as usual on the surface, but the mechanics underneath have changed.

The credit market 2026 is characterised by a recalibration where lenders price risk with surgical precision. In previous cycles, a rising tide lifted all boats; in 2026, lenders are scrutinising the seaworthiness of every individual vessel.

The Mechanics of the Reset

- Approvals Slow Down: The velocity of capital deployment is decelerating. Investment committees are demanding deeper dives into fundamental data. What used to take four weeks may now take twelve.

- Leverage Reduces: The days of pushing LTV ratios to the brink are over. Lenders are building larger equity buffers to protect against valuation volatility.

- Pricing Widens for Non-Prime: While investment grade issuers might see stability, the credit spreads for anything slightly complex or non-prime are widening. The market is bifurcating between the “pristine” and the “rest.”

- Documentation Standards Tighten: Covenants are returning with force. Lenders are less willing to accept “covenant-lite” structures, demanding enforceability and rigorous reporting.

For the borrower, this means that narrative consistency is critical. You cannot present a bullish growth story to an equity investor and a conservative stability story to a debt provider. In the 2026 credit landscape, these discrepancies are flagged immediately during diligence.

Why This Reset Matters More for Borrowers Than Investors

There is a distinct asymmetry in the outlook 2026. Investors, whether they are allocating to fixed income, private credit, or equity, have optionality. They can choose to sit on cash, buy government bonds, or simply wait for the “fat pitch.” They are currently being compensated reasonably well for patience.

Borrowers do not have this luxury. For a borrower, liquidity is often time-bound. Whether it is a refinancing wall, a strategic acquisition, or a capital expenditure need, the requirement for funds is driven by the calendar. In the credit market 2026, liquidity is gated by scrutiny.

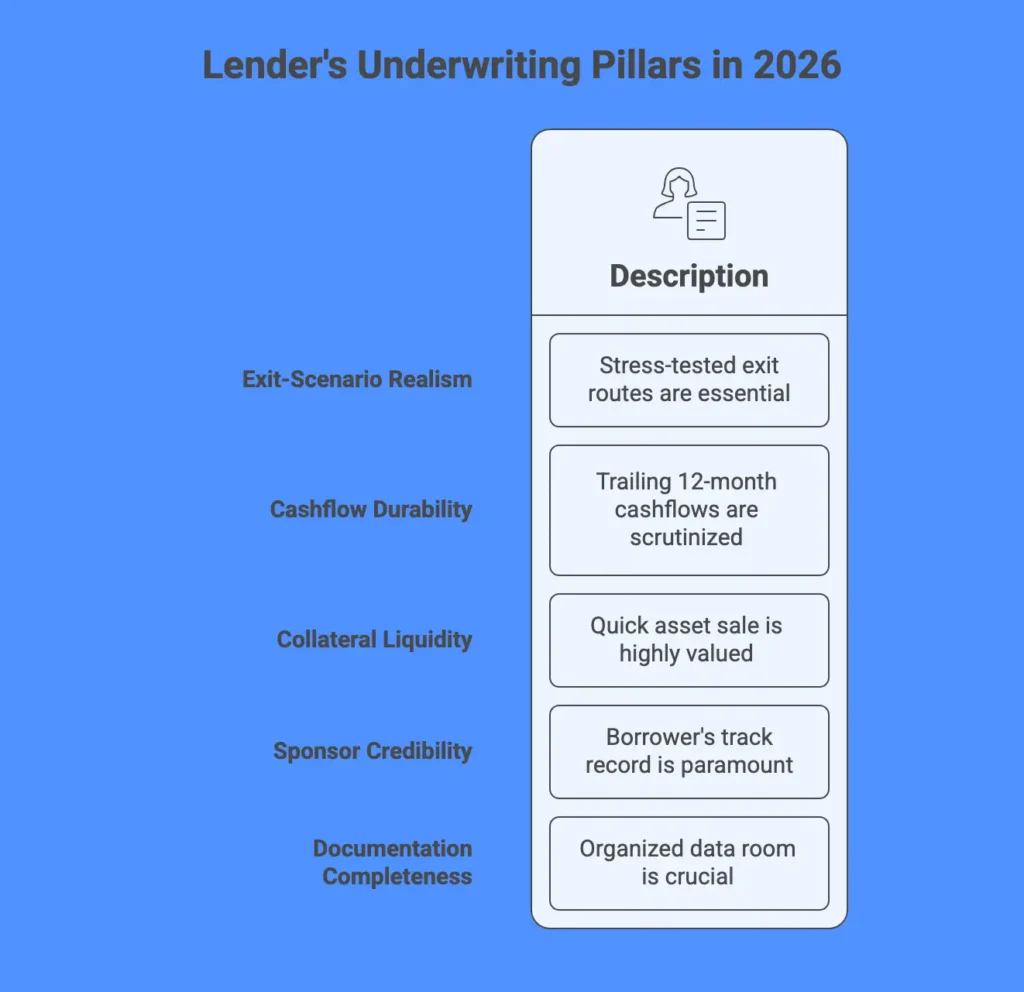

Lender’s Checklist for 2026

Lenders in 2026 are prioritising safety over yield chasing. Their focus has shifted from “How much can we deploy?” to “How do we get out?” Consequently, five key pillars now dominate the underwriting process:

- Exit-Scenario Realism: Vague plans to “refinance in three years” are no longer sufficient. Lenders want to see stress-tested exit routes that work even if interest rates remain elevated.

- Cashflow Durability: Pro-forma adjustments and “future synergies” are being discounted heavily. Lenders are looking at trailing 12-month (TTM) cashflows with a sceptical eye.

- Collateral Liquidity: It is not just about the value of the asset; it is about how quickly it can be sold. Illiquid assets are being hair-cut aggressively.

- Sponsor Credibility: The track record of the borrower is paramount. Lenders are conducting forensic diligence on the behaviour of sponsors during the 2024-2025 period. Did they support the asset? Did they communicate transparently?

- Documentation Completeness: A disorganised data room is now a deal-killer. It signals operational risk. (For more on this, see our guide on Data Room for Lending).

Credit Market 2026 – Real-World Borrower Scenarios

To understand the market outlook fully, we must move beyond theory. The following scenarios illustrate how the credit market 2026 dynamics play out for different types of borrowers.

Scenario 1: The Developer Capital Stack Gap

A seasoned property developer approaches the market to refinance a stabilised commercial asset. Based on 2024 metrics, they assume a refinance at 65–70% LTV is achievable.

- The 2026 Reality: The lender, concerned about cap rate expansion and macro volatility, is only comfortable at 50–55% LTV.

- The Consequence: The developer faces a significant capital gap. They must either inject fresh equity (which may be scarce) or seek expensive mezzanine debt/preferred equity to plug the hole. The deal stalls not because the asset is bad, but because the leverage expectations were misaligned with the credit outlook.

Scenario 2: The Outdated Valuation

A corporate borrower seeks expansion capital, presenting a valuation report from late 2024. They argue that the business has grown since then, so the value should be higher.

- The 2026 Reality: The credit committee dismisses the application immediately. In a market defined by valuation sensitivity, relying on data that is 18 months old signals a lack of risk awareness.

- The Consequence: The borrower loses credibility. To re-engage, they must commission a fresh, third-party valuation, delaying the process by months and losing the strategic initiative.

Scenario 3: The Family Office and Illiquid Assets

A Family Office holding a significant position in listed but thinly traded equity assumes that a securities based loan will be straightforward and quick.

- The 2026 Reality:The lender, wary of market liquidity and potential volatility in emerging market or niche sectors, demands enhanced reporting covenants and a revised exit timing structure. They refuse to lend against the full portfolio, cherry-picking only the most liquid names.

- The Consequence: The Family Office receives significantly less liquidity than anticipated and is forced to pledge additional assets to secure the facility.

Why the Credit Market 2026 is Becoming More Selective

Why is the credit market 2026 so fastidious? It is not arbitrary; it is a rational response to a confluence of global factors.

1. Tight Spreads and Risk Compensation

As noted in the introduction, tight credit spreads mean that lenders are not being paid a premium to take on excessive risk. When the spread between risk-free rates and corporate credit is narrow, the margin for error disappears. Lenders naturally migrate toward the highest quality borrowers, investment grade or top-tier private market sponsors, leaving the middle market to fight for attention.

2. Rate-Cut Uncertainty and Duration Risk

While the market forecasts regarding central bank policy have oscillated, the reality of 2026 is that we are likely in a “higher-for-longer” or at least “volatile-for-longer” regime. Interest rates may settle, but the path there is rocky. This creates duration risk. Lenders are hesitant to lock in long-term rates for borrowers with shaky fundamentals, preferring shorter tenors or floating rate structures that protect their own balance sheets.

3. Economic Headwinds and the Labour Market

The labour market is a lagging indicator, and by 2026, we may see the full effect of the previous years’ tightening. A softening labour market impacts consumer spending, which flows upstream to corporate earnings. Lenders are modelling downside scenarios where earnings growth stalls. If a borrower’s ability to service debt relies on aggressive growth assumptions, they will fail the stress test.

4. The Maturation of Private Credit

Private credit has grown from a niche asset class to a dominant force in the capital market. However, with size comes scrutiny. Allocators (pension funds, insurers) are demanding more rigour from private credit funds. This pressure flows down to the borrower. While there is more money available, the “wild west” days of unregulated private lending are fading. Funds are acting more like banks regarding due diligence.

5. Structural Forces: AI and Geopolitics

The 2026 global landscape is also shaped by structural shifts. AI and data centers are consuming vast amounts of capital, creating a new sector of “infrastructure credit” that competes for allocation. Simultaneously, geopolitical fragmentation means that global credit is less fungible. A lender may be comfortable with UK or US risk but entirely closed off to specific emerging markets due to sanctions or instability.

What Borrowers Must Consider: Practical, Actionable Takeaways

If you are a borrower approaching the credit market 2026, hope is not a strategy. You must operationalise your preparation. The market is currently pricing in a premium for organisation and transparency.

Here is your checklist for navigating the year ahead:

1. Prepare a Lender-Grade Data Room

Before you send a single email to a lender, your data room must be immaculate. It should contain structured folders with historical financials, legal entity charts, and tax returns. A sloppy data room suggests a sloppy management team.

- Internal Resource: Review our guide on Data Room for Lending to ensure you meet the 2026 standard.

2. Update Valuations and Financials

Do not rely on 2025 data. Lenders need to see the current picture. If your assets have not been valued in the last 6 months, commission a refresh. Outdated data kills deals faster than bad data because it implies you are hiding the current reality.

3. Reduce Leverage Expectations

Go into negotiations with a conservative ask. If you ask for 75% LTV, you may be dismissed as unrealistic. If you ask for 55% with a clear path to debt service, you invite a conversation. Acknowledging the credit risk environment upfront builds trust.

4. Strengthen Your Exit Narrative

“We will sell the asset” is not an exit strategy. Lenders want to know: Who is the buyer? Is there market depth for this asset? What if the sale takes 12 months longer than planned? Your financial model must demonstrate resilience under these delayed scenarios.

- Internal Resource: Ensure your projections are robust by utilising proper Structured Finance Modelling.

5. Prioritise Liquidity Buffers

Lenders in 2026 love liquidity. Show them that you have cash on the balance sheet to weather a storm. If you are running “lean,” you are viewed as fragile. A borrower with a healthy liquidity buffer is often granted better terms than one who is maxed out, even if the underlying asset is identical.

6. Expect Deeper Diligence on Sponsors

Your reputation is an asset. Be prepared for background checks that go beyond credit scores. Lenders are looking at litigation history, past performance in downturns, and general market reputation. If there are skeletons, disclose them early and control the narrative.

7. Assume Slower Approvals

Time is the enemy of all deals. Start your refinancing or acquisition financing processes 3 to 6 months earlier than you think is necessary. The investment research and committee approval stages are taking longer as institutional investors demand more granular data.

Credit Market 2026 And The Role of AI and Technology

It is impossible to discuss the outlook 2026 without touching on AI. For borrowers, AI is a double-edged sword.

On one hand, lenders are using AI to process data faster. They can ingest your bank statements and audit reports in minutes, identifying discrepancies that a human analyst might miss. This means your numbers must be flawless.

On the other hand, AI and data centers represent a massive investment opportunity. Borrowers operating in the digital infrastructure space, providing the physical shell, power, and cooling for the AI revolution, are finding a very receptive audience in the credit markets. This sector is enjoying strong tailwinds, and lenders are eager to deploy capital here, provided the credit quality of the off take contracts (the tech giants leasing the space) is solid.

For the general borrower, the lesson is clear: Lenders are using advanced tech to assess you (see AI in Finance). You should use similar rigour to assess yourself.

Conclusion – Strategic Mindset Shift

The credit market 2026 is not closed, but it is gated. The key to unlocking it lies in a strategic mindset shift.

The next two years will favour borrowers who operate like institutional sponsors, not opportunists. The “cowboy” era of borrowing, characterised by loose structures, high leverage, and minimal reporting, is incompatible with the current landscape.

Borrowers who adapt to the reset with discipline, preparation, and realistic structures, will find funding. In fact, they may find that because the “tourists” have been washed out of the market, the relationship with lenders becomes deeper and more strategic.

The market participants who succeed in 2026 will be those who understand that credit is no longer a commodity; it is a partnership based on transparency and rigorous risk management.

Call to Action

The landscape has shifted, and the old playbooks will not suffice. If you have upcoming maturities, disposals, or significant liquidity needs in the next 12 to 24 months, waiting until the last minute is a risk you cannot afford.

Forbes Le Brock can review your documentation discreetly and outline structured financing pathways suitable for the 2026 landscape. Whether you are dealing with complex cross-border assets or simply need to optimise your capital stack, a well-prepared borrower gets a very different outcome in this market.

Contact us today to discuss your credit strategy.